内部バーと移動平均線に基づく自動定量取引戦略

概要

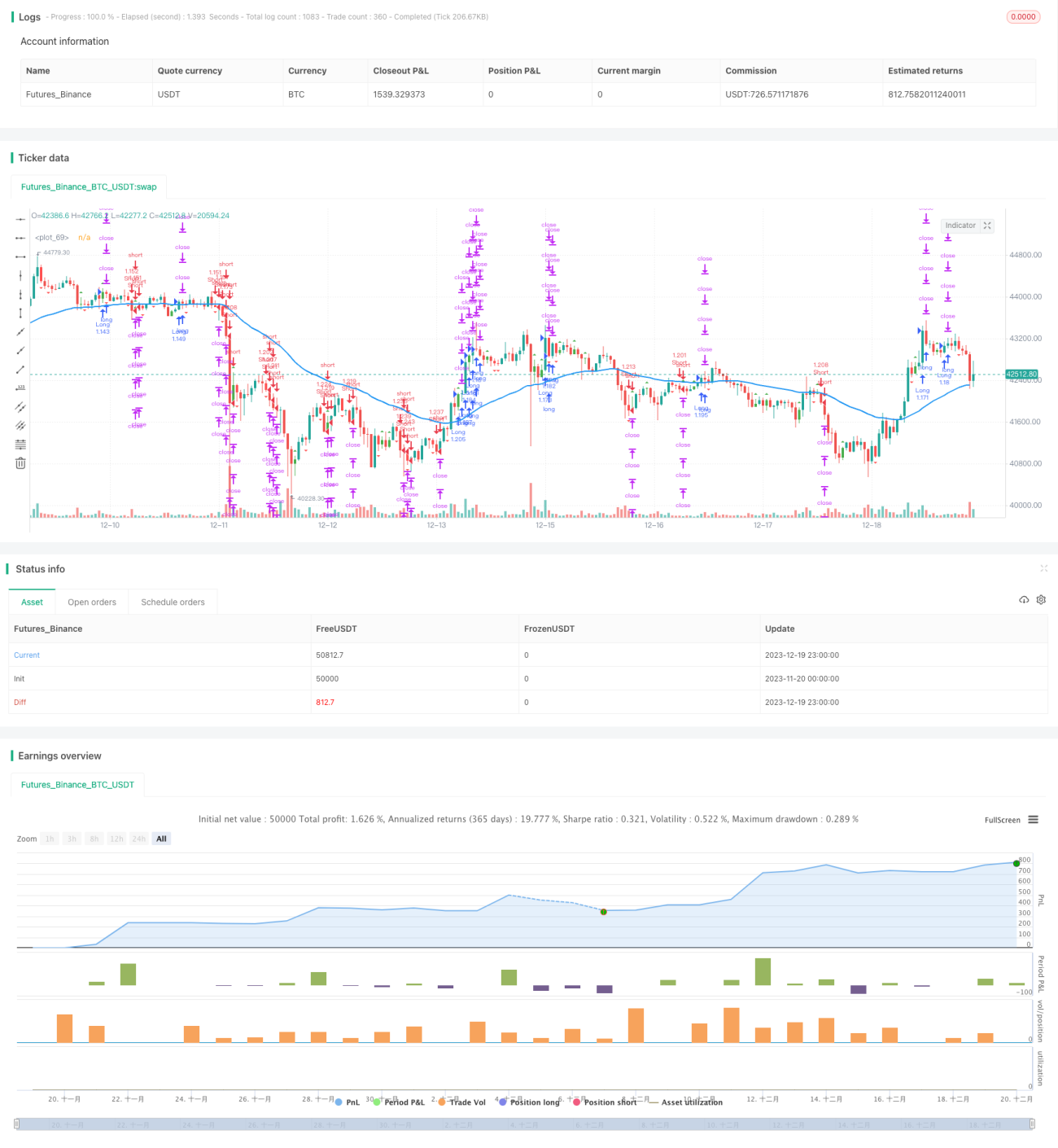

本戦略の核心は、内部バー形状と移動平均線インジケーターを組み合わせて自動売買を実現することです。内部バー形状が発生した場合、現在のトレンドが転換する可能性があることを示すため、その時点で移動平均線の位置を利用して最終的な売買方向を判断します。

戦略の原理

-

内部バー形状を探します。内部バー形状とは、あるローソク足の高値と安値が前のローソク足の実体部分の間にある状態を指します。実体の色に基づいて、内部バーが買い内部バーか売り内部バーかを判断します。

-

移動平均線の位置を判断します。内部バー形状が見つかったとき、価格が移動平均線より上にある場合は買いシグナル、下にある場合は売りシグナルとします。

-

内部バー形状と移動平均線の買い・売りシグナルを組み合わせて、最終的な売買方向を決定します。すなわち、弱気内部バーが平均線を下抜けたら売り、強気内部バーが平均線を上抜けたら買いとします。

戦略のメリット

-

テクニカル指標と価格形状を組み合わせることで、取引判断の精度を向上させます。

-

内部バー形状自体が強い価格転換シグナルを含んでおり、トレンドの転換点を早期に特定できます。

-

移動平均線によりノイズの一部が除去され、レンジ相場での迷いを防ぎます。

-

完全自動売買を実現し、手動取引の時間と労力を大幅に削減します。

戦略のリスクとその解決方法

-

価格が平均線付近で揉み合う場合、誤ったシグナルが多発し、過剰取引につながる可能性があります。移動平均線のパラメータを最適化するか、フィルター条件を追加することで誤シグナルを減らせます。

-

本戦略は比較的明確なトレンドがある市場に適しており、レンジ相場では効果が低下する可能性があります。ADXのようなトレンド判断指標を組み合わせて、アルゴリズムの起動タイミングを制御できます。

-

一定のタイムラグが存在します。適切にパラメータを短縮するか、移動平均線の計算方法を最適化することでラグを低減できます。

-

ドローダウンリスクが大きい場合があります。ストップロスを設定して損失リスクを抑え、またポジション管理を適切に調整することでドローダウン低減にも役立ちます。

戦略の最適化方向

-

内部バー判定の周期パラメータを最適化し、最適なパラメータ組み合わせを探します。

-

EMAやSMAなど異なる種類の移動平均線を試し、最も適した移動平均線指標を決定します。

-

MACDやKDJなどの補助指標を追加し、売買判断の根拠を充実させ、シグナルの精度を高めます。

-

ADXやATRなどのフィルター指標を導入し、アルゴリズム起動の環境を制御して、不適切な市場での稼働を回避します。

-

リスクポジション管理や損失補填ポジションなど、ポジション管理戦略を最適化し、リスクを抑えつつ高リターンを目指します。

まとめ

本戦略は、内部バーシグナルと移動平均線指標を動的に追跡することで、完全自動の定量売買ソリューションを実現しています。シグナルの生成はシンプルで明確であり、理解と追跡が容易です。トレンドが明確な市場で優れたパフォーマンスを発揮します。パラメータとルールをさらに最適化することで、戦略の安定性と収益性をさらに高めることができます。

- 1