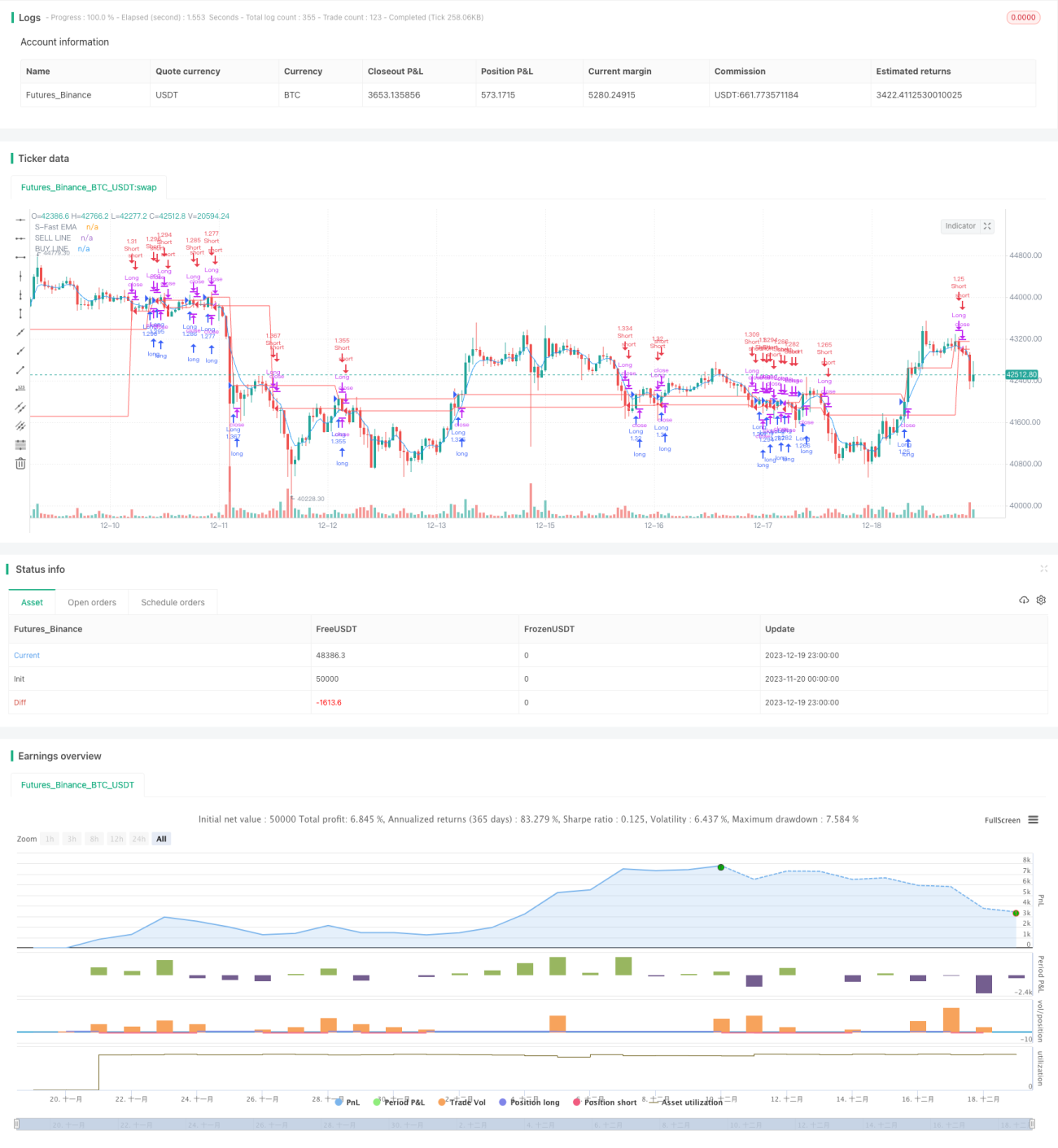

三龍複合テクニカル取引戦略

概要

三龍システムは、拡張価格出来高トレンド指標、ドンチャンチャンネル指標、パラボリックSAR指標を組み合わせた複合テクニカル取引戦略です。この戦略は、3つの指標の補完的な利点を活用して、市場トレンドの方向性と潜在的な売買シグナルを特定します。

戦略の原理

この戦略はまず、拡張価格出来高トレンド指標とドンチャンチャンネルを使用して市場トレンドの方向性を判断します。拡張価格出来高トレンド指標がベースラインより上にあり、価格がドンチャンチャンネルの上限より高い場合、上昇トレンドを示します。逆に、拡張価格出来高トレンド指標がベースラインより下にあり、価格がドンチャンチャンネルの下限より低い場合、下降トレンドを示します。

市場トレンドの方向性を特定した後、この戦略はパラボリックSAR指標を導入して具体的な買いと売りのタイミングを特定します。パラボリックSAR指標が価格を下回ったときに買いシグナルが発生し、パラボリックSAR指標が価格を上回ったときに売りシグナルが発生します。

シグナルをさらに検証するために、この戦略は複数の時間枠でトレンド方向を確認し、市場の激しい変動期間中のエントリーを回避します。さらに、複数の利食いレベルを設定して利益を確定し、リスクを管理します。

優位性の分析

三龍システムの最大の利点は、異なるタイプの指標を組み合わせて使用することで、市場の動きをより包括的かつ正確に判断できることです。具体的には、主な利点は次のとおりです。

- 拡張価格出来高トレンド指標は、トレンドの変化点とトレンドの強さを正確に特定でき、基本面が良好です。

- ドンチャンチャンネル指標はトレンド方向を明確に判断でき、トレンドをうまく捉えることができます。

- パラボリックSARをトレンド指標と組み合わせることで、売買ポイントをより正確に見つけることができます。

指標を有機的に組み合わせることで、各指標の利点を最大限に活かし、三龍システムは中長期の値動きを正確に判断し、売買ポイントをより正確に特定できるため、優れたリスクリターン比を得ることができます。

リスク分析

三龍システムは指標の組み合わせ戦略であり、全体的なリスクは管理可能ですが、注意すべきリスクがいくつかあります。

- 拡張価格出来高トレンド指標は、偽のブレイクアウトや大幅な反転の場合に誤判断するリスクがあります。

- レンジ相場では、ドンチャンチャンネルが狭くなり、誤ったシグナルが発生する可能性が高くなります。

- パラボリックSARのパラメータ設定が適切でない場合、売買ポイントの特定に影響を与える可能性があります。

上記のリスクに対して、指標パラメータの設定を適宜調整し、他の指標を補助的に参照することで、単一指標の失敗確率を低減することをお勧めします。また、適切なストップロスとポジション管理も戦略全体のリスクコントロールに不可欠です。

戦略の最適化

三龍システムにはさらなる最適化の余地があります。

- 機械学習アルゴリズムを導入して、指標パラメータを自動最適化できます。

- ボラティリティ指標を導入して補助判断を行い、戦略の安定性を向上させることができます。

- センチメント指標を組み合わせて、一般投資家の感情変動が戦略に与える影響を判断できます。

アルゴリズムによるパラメータ最適化、複数指標の組み合わせ判断、行動の定量分析を通じて、三龍システムの収益性と安定性をさらに向上させることが期待されます。業界の最先端技術に継続的に注目し、戦略システムを最適化・改善していきます。

まとめ

三龍システムはテクニカル指標の組み合わせ戦略であり、拡張価格出来高トレンド指標、ドンチャンチャンネル指標、パラボリックSAR指標の3つの補完的な利点を活用して市場の動きを判断し、売買ポイントを見つけます。この戦略は判断が正確でリスクが管理可能であり、複数の検証を経て、中長期投資家に適した効果的な戦略システムです。三龍システムを継続的に最適化し、より優れたリスクリターン比を目指します。

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="TRIPLE DRAGON SYSTEM", overlay=true,default_qty_type = strategy.percent_of_equity,default_qty_value=100,initial_capital=1000,pyramiding=0,commission_value=0.01)

/////////////// DRAG-ON ///// EMA'S ///////////////

emar = ta.ema(close,5)- 1