三移動平均線低遅延高速取引戦略

ストラテジーの原理

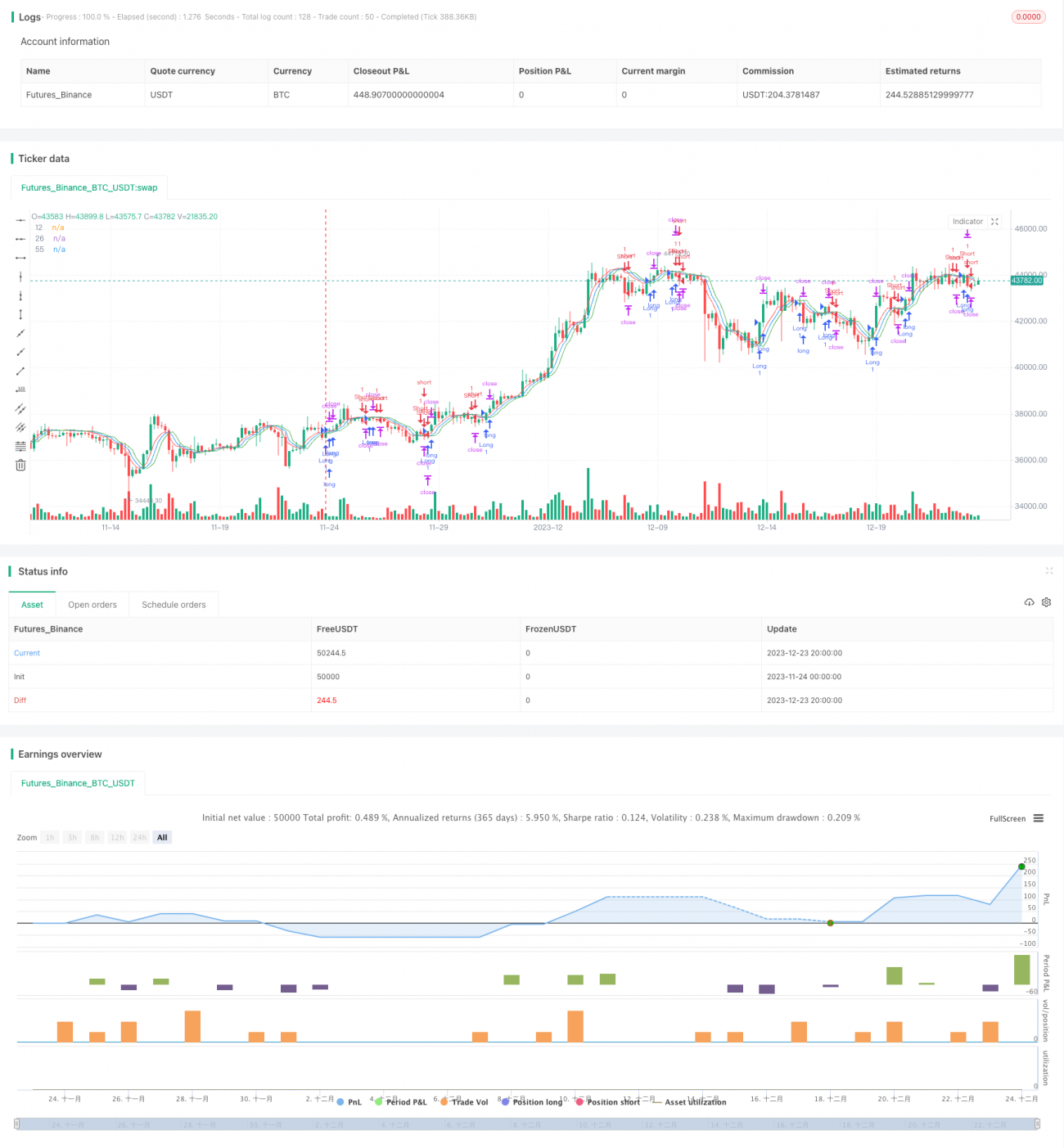

本ストラテジーは、12期間、26期間、55期間の低ラグTEMA(トリプル指数移動平均)の3本の移動平均線を使用します。これら3本の移動平均線はそれぞれ高速線、中速線、低速線を表します。高速線が中速線を上抜けた時に買いシグナル、高速線が中速線を下抜けた時に売りシグナルが発生します。このように3本の移動平均線のクロスを利用して市場の売買点を判断し、高頻度取引を実現します。

コード内では、低ラグTEMAを計算するためのテンプレート関数tema()が定義されています。その計算式はTEMA = 2*EMA - EMA(EMA)であり、2重指数移動平均(EWMA)を使用して計算します。本質的には2重平滑化移動平均であり、主な利点はラグを大幅に低減できることです。これにより、価格変化により迅速に反応し、取引シグナル判断のリアルタイム性が向上します。

具体的には、本ストラテジーのエントリー判断は以下の通りです。高速線が中速線を上抜け、かつ高速線が低速線よりも上にある場合に買いシグナルが発生します。高速線が中速線を下抜け、かつ高速線が低速線よりも下にある場合に売りシグナルが発生します。

優位性分析

本ストラテジーの最大の優位性は、エントリーとエグジットの判断が迅速かつ正確である点です。3本の移動平均線の低ラグ設計によりラグが大幅に低減され、価格変化に素早く対応できます。また、3本の移動平均線のクロスで判定するため、誤判定を回避できます。

さらに、本ストラテジーは高頻度取引に適しており、短期的な価格変動から利益を得ることができます。素早いエントリーとエグジットの運用スタイルにより、ボラティリティの高い市場で利益を上げることが可能です。

リスク分析

本ストラテジーの最大のリスクは、超短期的なダマシ(ホワイプソー)が発生する可能性がある点です。低ラグ設計により価格変化に非常に敏感であるため、市場によっては高頻度の振動が発生し、容易にダマシに巻き込まれる可能性があります。

また、高頻度取引では手数料やスリッページのコストが多く発生します。収益力が不十分な場合、取引コストによって逆に損失を被るリスクがあります。

さらに、本ストラテジーはトレーダーにリアルタイムな監視能力が求められ、損切りラインや利確ラインを随時更新する必要があります。

最適化の方向性

本ストラテジーは以下の点から最適化が可能です。

- 3本の移動平均線の期間パラメータを最適化し、異なる市場の特性により適応させる。

- ボラティリティ指標や出来高指標を追加してシグナルを確認し、レンジ相場でのダマシを回避する。

- より多くのファクターを組み合わせて損切り・利確メカニズムを設定し、動的なトレーリングストップを実現する。

- ポジション管理を最適化し、資金管理手法を通じて1回の取引リスクをコントロールする。

- 機械学習アルゴリズムを組み合わせてストラテジーパラメータを動的に最適化する。

まとめ

本ストラテジーは、3本の移動平均線を用いた低ラグ高速取引ストラテジーです。低ラグ設計により素早いエントリーとエグジットを実現し、短期的なチャンスを捉える高頻度取引に適しています。本ストラテジーの最大の利点はシグナル判断が迅速かつ正確であること、最大の欠点はレンジ相場でダマシに巻き込まれやすいことです。本稿では、詳細な原理の解説、優位性分析、リスク分析、最適化の検討を通じて、本取引ストラテジーを包括的に概説しました。

結論

これは低遅延トリプル移動平均高速取引戦略です。その低遅延設計により、迅速なエントリーとエグジットが可能となり、短期的な機会を捉える高頻度取引に適しています。この戦略の最大の利点は、シグナルの判定が迅速かつ正確であることです。最大の欠点は、レンジ相場においてダマシに遭いやすいことです。本稿では、その理論的背景、利点、リスク、および最適化の方向性について詳細に分析することで、この取引戦略を総合的にまとめています。

[/trans]

/*backtest

start: 2023-11-24 00:00:00

end: 2023-12-24 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("scalping low lag tema etal", shorttitle="Scalping tema",initial_capital=10000, overlay=true)

mav = input(title="Moving Average Type", defval="temadelay", options=["nkclose", "ema", "emadelay", "fastema", "tema", "temadelay"])

lenb = 3- 1