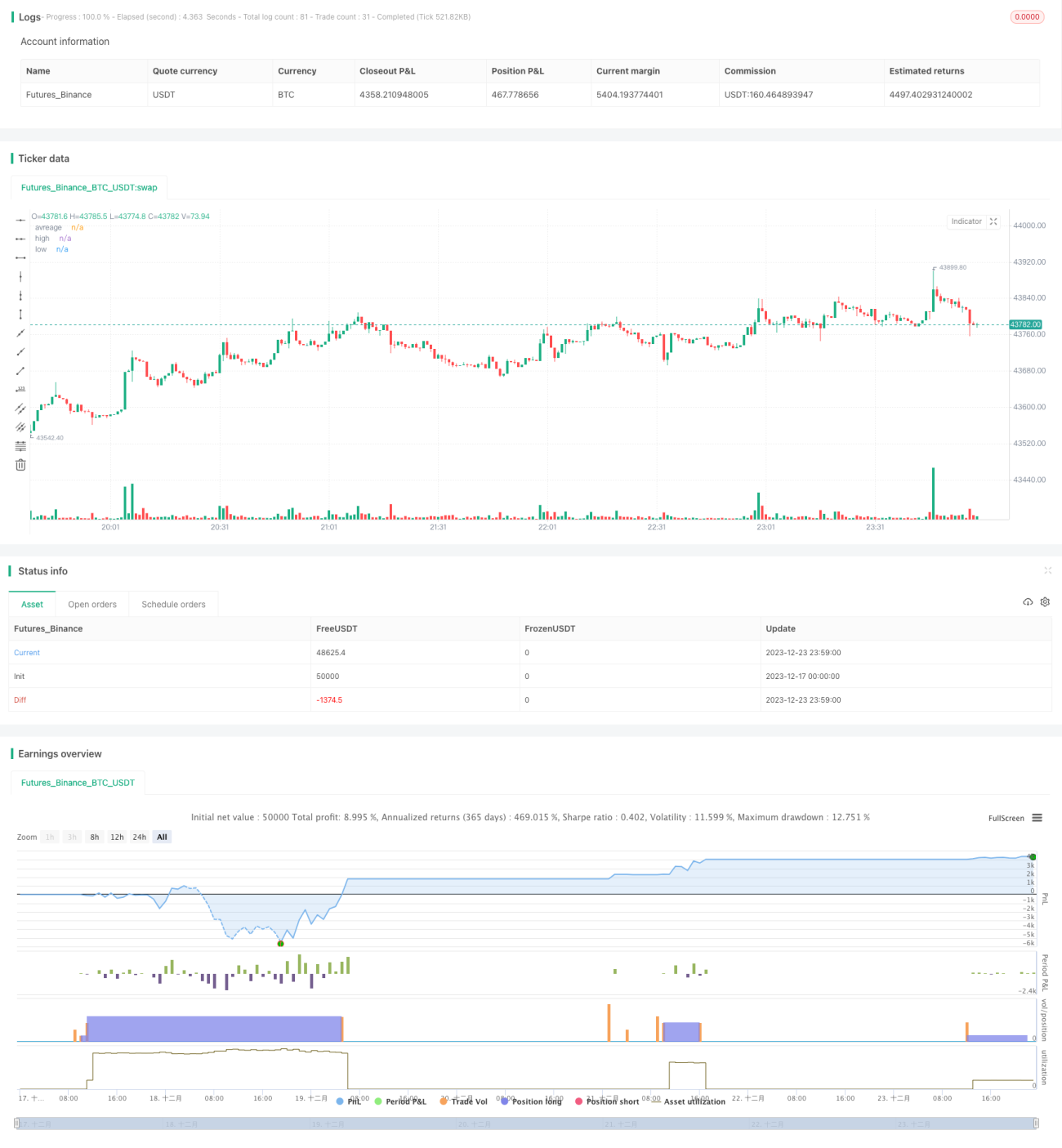

RSI指標に基づくロングトレンドフォロー戦略

概要

この戦略は、相対力指数(RSI)インジケーターに基づいて設計された、RSIの安値で買い、高値でストップロス・利確を行う多頭トレンド追従取引戦略です。RSIが買われ過ぎラインを下回ると買いシグナルを生成し、RSIが売られ過ぎラインを上回ると売りシグナルを生成します。戦略はトレンド追従のパフォーマンスを最適化し、取引リスクを効果的に管理します。

戦略の原理

この戦略はRSIインジケーターを使用して、株式の価格が過大評価されているか過小評価されているかを判断します。RSIインジケーターに買われ過ぎ・売られ過ぎのラインを組み合わせることで、買いと売りのシグナルを形成します。具体的には、RSIが20の売られ過ぎラインを上抜けると買いシグナルが発生し、RSIが80の買われ過ぎラインを下抜けると売りシグナルが発生します。

多頭ポジションを建てた後、戦略は初期ストップロスラインを設定して下値リスクを抑制します。同時に、異なる比率の利確ラインを2つ設定し、分割して利確することで利益を確定します。具体的には、最初に保有ポジションの50%を利確し、利確価格は買値の3%とします。次に、残りの50%のポジションを利確し、利確価格は買値の5%とします。

この戦略は、RSIインジケーターを簡潔かつ効果的に利用してエントリーのタイミングを判断します。ストップロスと利確の設定は合理的であり、リスクを効果的に抑制できます。

戦略の利点

- RSIインジケーターを使用して多空を判断し、盲目的な買いを回避

- RSIパラメーターが最適化されており、指標の効果が向上

- ダブル利確設計が合理的で、分割利確により多くの利益を確定可能

- 初期ストップロスと継続的ストップロスにより巨額損失を防止

リスク分析

- 多頭戦略のため、持続的に上昇しない相場では効果が低い

- RSIが誤ったシグナルを発する確率があり、シグナルの誤判断により損失が拡大する可能性がある

- ストップロス値が深すぎるとストップロスできなくなるリスクがある

- 追加ポジションの回数と比率に制限がないため、損失が拡大する可能性がある

最適化の方向性

- 他のインジケーターと組み合わせてRSIシグナルをフィルタリングし、シグナルの精度を向上

- 追加ポジションの回数と比率に制限を追加

- 異なるRSIパラメーターの効果をテスト

- ストップロス・利確ポイントを最適化し、リスクを低減

まとめ

この戦略はRSIインジケーターを使用して相場を判断し、ストップロス・利確の設定が合理的です。相場のトレンドを効果的に判断し、取引リスクを制御できるため、多頭トレンド追従戦略として適しています。シグナルのフィルタリング、パラメーターテスト、ストップロスの最適化などを通じて、さらに戦略の安定性を高めることができます。

- 1