動的売買量変動ブレイクアウト戦略

1

Follow

1802

Followers

概要

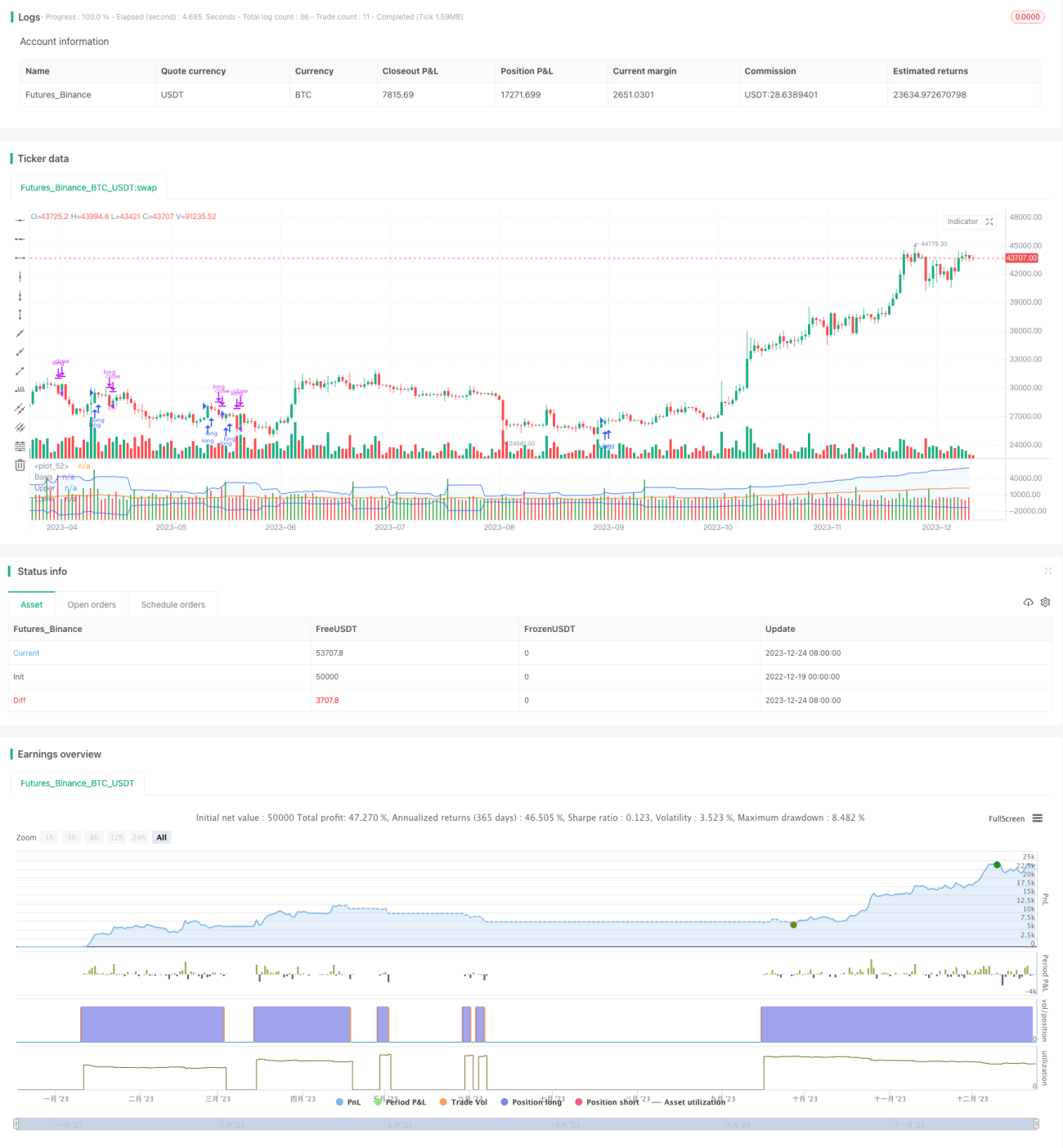

本戦略は、カスタム期間の売買量を用いたマルチ(買い)・ベア(売り)判断に、週足VWAPやボリンジャーバンドを組み合わせてフィルタリングし、高確率のトレンドフォローを実現します。同時に動的な利確・損切りメカニズムを導入することで、一方向のリスクを効果的にコントロールします。

戦略の原理

- カスタム期間内の売買量指標を計算

- BV(買い量):安値での買いによって生じた出来高

- SV(売り量):高値での売りによって生じた出来高

- 売買量の処理

- 20期間のEMAで平滑化

- 処理後の売買量を正負に分離

- 指標の方向性を判断

- 指標が0より大きければ強気、0より小さければ弱気

- 週足VWAPとボリンジャーバンドでダイバージェンスを判定

- 価格がVWAPより上で指標が強気 → 買いシグナル

- 価格がVWAPより下で指標が弱気 → 売りシグナル

- 動的な利確・損切り

- 日足ATRに基づいて利確・損切りのパーセンテージを設定

戦略の優位性

- 売買量は市場の実際の勢いを反映し、トレンドの潜在的なエネルギーを捉える

- 週足VWAPで大きな時間軸のトレンド方向を判断し、ボリンジャーバンドでブレイクシグナルを判定

- 動的ATRによる利確・損切りで、利益を最大限確保し、オーバーシュートを回避

戦略のリスク

- 売買量データには一定の誤差が存在し、判断ミスを引き起こす可能性がある

- 単一指標の組み合わせによる判断では、誤シグナルが発生しやすい

- ボリンジャーバンドのパラメータ設定が不適切だと、有効なブレイクが狭められる

戦略の最適化方向

- 複数時間枠の売買量指標による最適化

- 出来高などの補助指標を追加してフィルタリング

- ボリンジャーバンドのパラメータを動的に調整し、ブレイク効率を向上

まとめ

本戦略は、売買量の予測性を十分に活用し、VWAPとボリンジャーバンドを補完することで高確率のシグナルを生成し、動的な利確・損切りでリスクを効果的に制御する、効率的で安定した定量取引戦略です。パラメータとルールの継続的な最適化により、さらなる効果が期待できます。

Source

Pine

/*backtest

start: 2022-12-19 00:00:00

end: 2023-12-25 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © original author ceyhun

//@ exlux99 update

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1