RSI指標に基づくクロスタイムフレーム戦略

1

Follow

1789

Followers

概要

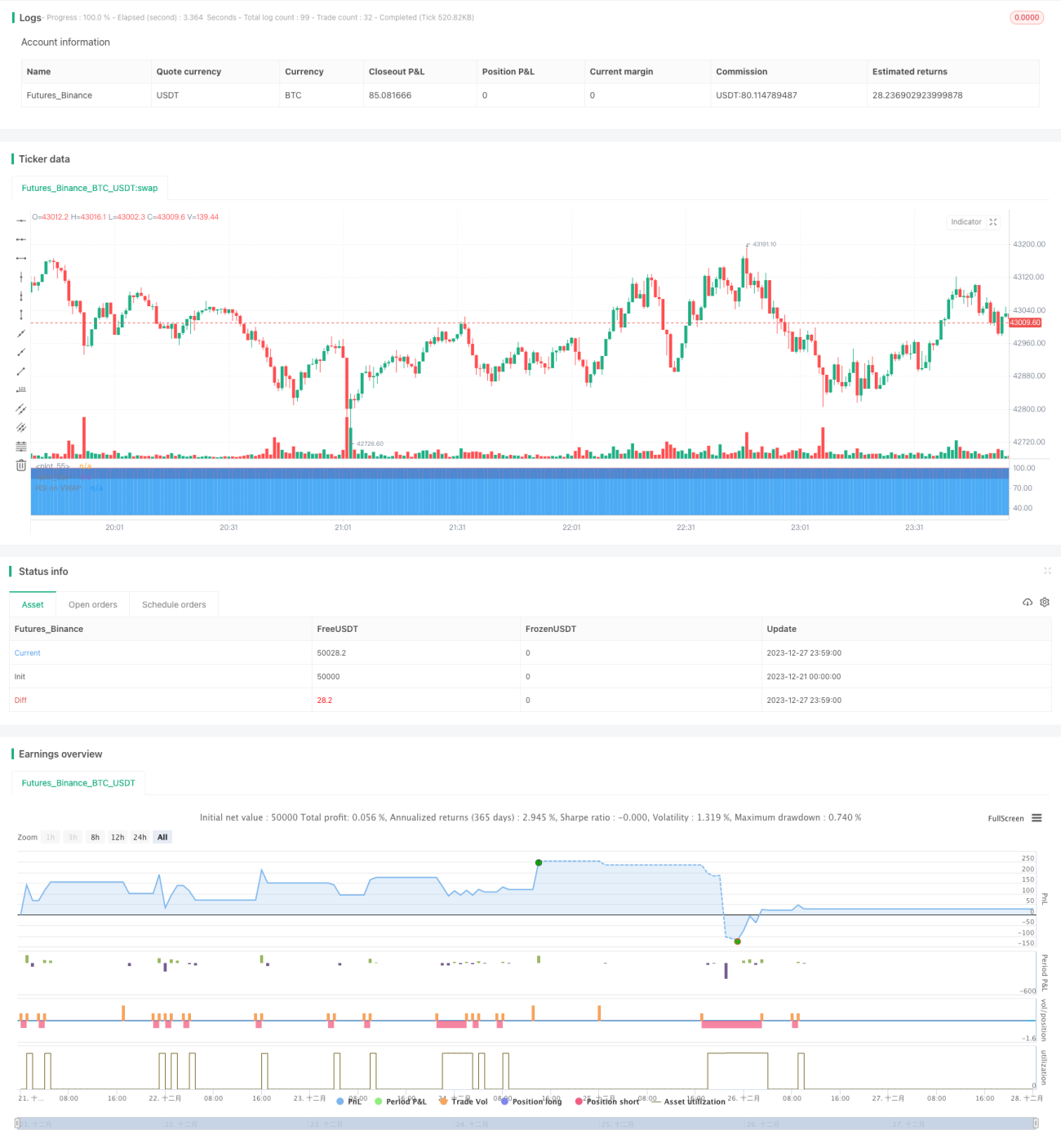

この策略は,RSI指標に基づくクロスタイムフレームのBTC空白策である.この策略は,各K線の交割量加重平均価格 ((VWAP) を計算することでVWAP曲線を得て,その曲線にRSI指標を適用する.RSI指標が超買区から下方へ横断するデッドフォーク信号を表示するときにBTC空白する.

戦略原則

- 取引量加重平均値 ((VWAP) を計算して,VWAP曲線が得られる.

- VWAP曲線にRSI指標を適用し,パラメータは20日,超買線は85日,超売り線は30日

- RSIが超買区 (85),超売区 (30) から下方へ突破すると,空白を入れます.

- 28K線を保持した後,RSIが再び超売り線を突破した場合,平仓

優位分析

- VWAPを使用すると,単なる閉店価格ではなく,実際の取引価格が反映されます.

- RSI指数で超買いと超売りを認識し,高値と低値を追うのを避ける

- タイムフレームを横断して操作する

- リスクは管理可能で,28K線は停止

リスクと解決策

- 緊急事態により,価格が急激に上昇し,損失は抑えられませんでした.

- タイム・フレームを活用し,被曝のリスクを低減する

- パラメータが正しく設定されず,機会が逃れやすい

- RSIパラメータと超買超売ラインのテストと最適化

- K線が超市街に突入できない

- 他の指標の判断傾向と組み合わせたパラメータの柔軟な調整

最適化の方向

- 複数のパラメータをテストし,最適なパラメータを見つけます.

- MACD,KDなどの他の指標と組み合わせて,超買超売領域に入っているかどうかを判断します.

- 種別テストパラメータの設定

- ストップ・メカニズムの最適化,変動率によるストップ・幅度設定

要約する

この戦略はVWAPとRSIを組み合わせてBTCの超買超売状態を識別し,タイムフレームを越えた方法で操作し,リスクを効果的に制御することができる.戦略の考え方は明確で分かりやすいであり,さらなるテストと最適化の価値があり,实体取引に適用される.

Source

Pine

/*backtest

start: 2023-12-21 00:00:00

end: 2023-12-28 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Soran Strategy 2 - SHORT SIGNALS", pyramiding=1, initial_capital=1000, default_qty_type=strategy.percent_of_equity, default_qty_value=50, overlay=false)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1