1

Follow

1802

Followers

概要

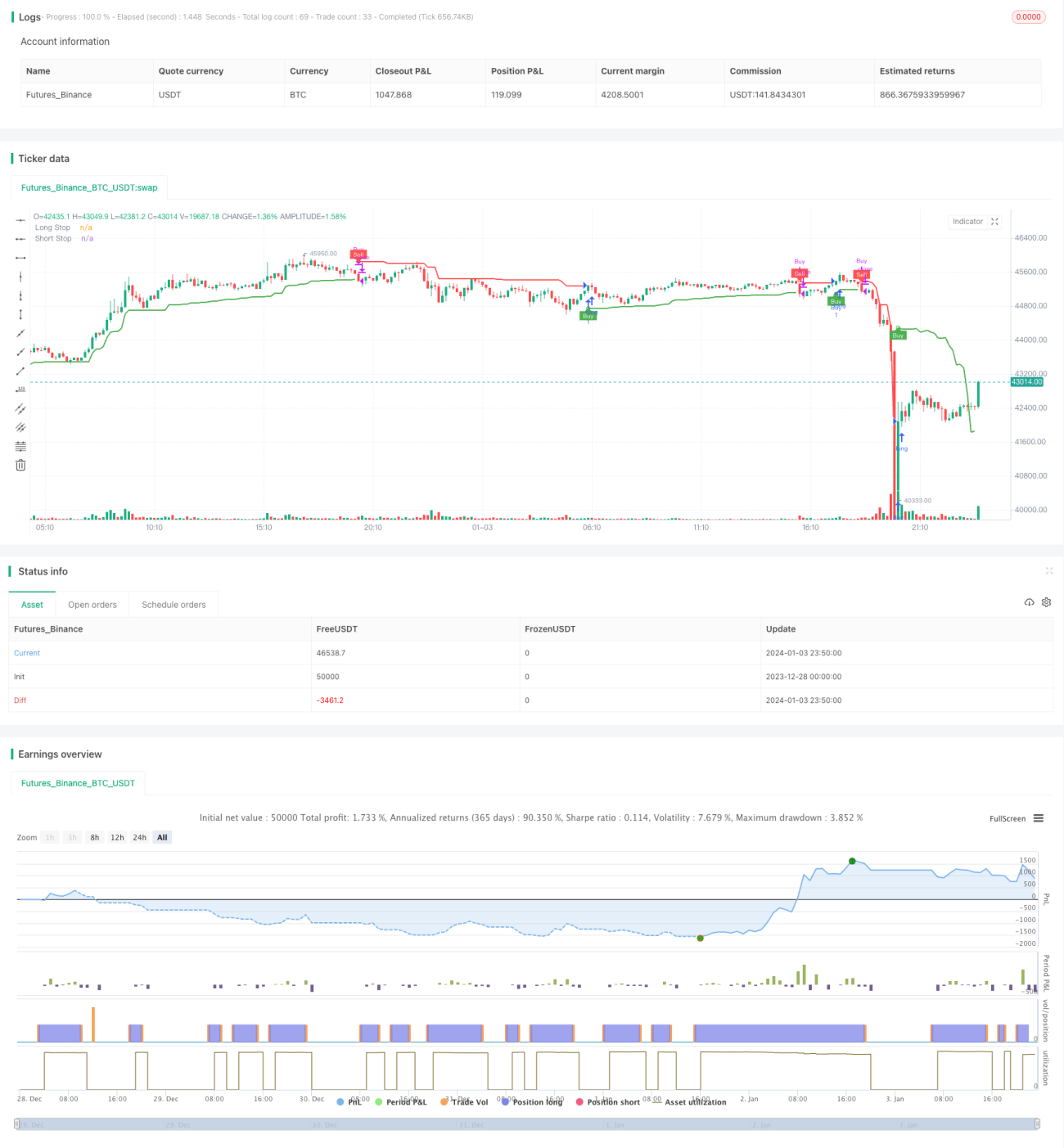

この戦略は、シャンデリア指標を使用して価格ブレイクの方向と強さを判断し、買いシグナルと売りシグナルを生成します。買い注文のみを実行します。

戦略の原理

この戦略はシャンデリア指標に基づいています。シャンデリア指標は、価格の高値、安値、および平均真のレンジ(ATR)を使用してストップロスラインを設定します。具体的には、22期間のATRを計算し、それに係数(デフォルトは3)を乗算します。この値に基づいて、長期ストップロスラインと短期ストップロスラインを設定します。ロングポジションを保有している場合、価格が長期ストップロスラインを下回ると売りシグナルが生成されます。ショートポジションを保有している場合、価格が短期ストップロスラインを上回ると買いシグナルが生成されます。

この戦略は買い注文のみを実行します。具体的には、価格が前回の長期ストップロスラインを上回ったときに買いシグナルを生成します。その後、価格が短期ストップロスラインを下回ったときに売りシグナルを生成してポジションをクローズします。

優位性分析

- シャンデリア指標を使用した動的なストップロスラインにより、リスクを効果的に管理できます。

- 価格ブレイクに連動して取引シグナルを生成することで、価格のトレンド性を捉えることができます。

- 買い注文のみを実行することで、相場の両端での反転を回避する戦略を実現しています。

- 複数の条件でトリガーされるアラートが設定されており、戦略の状態を即座に監視できます。

リスク分析

- シャンデリア指標はボラティリティに敏感であり、異常な価格変動が発生した場合に誤ったシグナルを発する可能性があります。

- 買い後にストップロスが設定されていないため、損失リスクを効果的に制御できません。

- トレーリングストップ(利益確定)が考慮されていないため、利益を固定できません。

リスク解決方法:

- 他の指標と組み合わせてシグナルをフィルタリングし、誤報を回避する。

- ストップロスラインを設定し、最大損失率を制限する。

- トレーリングストップ(利益確定)メカニズムを追加し、売りラインを動的に調整するか、部分的に利確することを検討する。

最適化の方向性

- 異なるパラメータ設定をテストし、買いと売りのタイミングを最適化できます。

- 他の指標による確認を追加し、誤ったシグナルを回避できます。

- 買いと売りの両方の操作を同時に行うことも検討できます。

- ストップロスと利益確定のメカニズムを設定できます。

まとめ

この戦略は、シャンデリア指標の動的なストップロスラインを使用して価格の反転の機会を識別します。価格が長期ストップロスラインを上抜けたときにのみ買い、価格が短期ストップロスラインを下回ったときに売ることで、片方向の取引を行い、相場の両端での反転を回避するシンプルな戦略です。この戦略はリスクを効果的に管理していますが、ストップロスや利益確定の設定はありません。他の指標によるフィルタリングやストップロス・利益確定の設定を追加することで、この戦略をより堅牢に最適化できます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1