トレンドフォロー・モメンタム・ブレイクアウト戦略の改善

概要

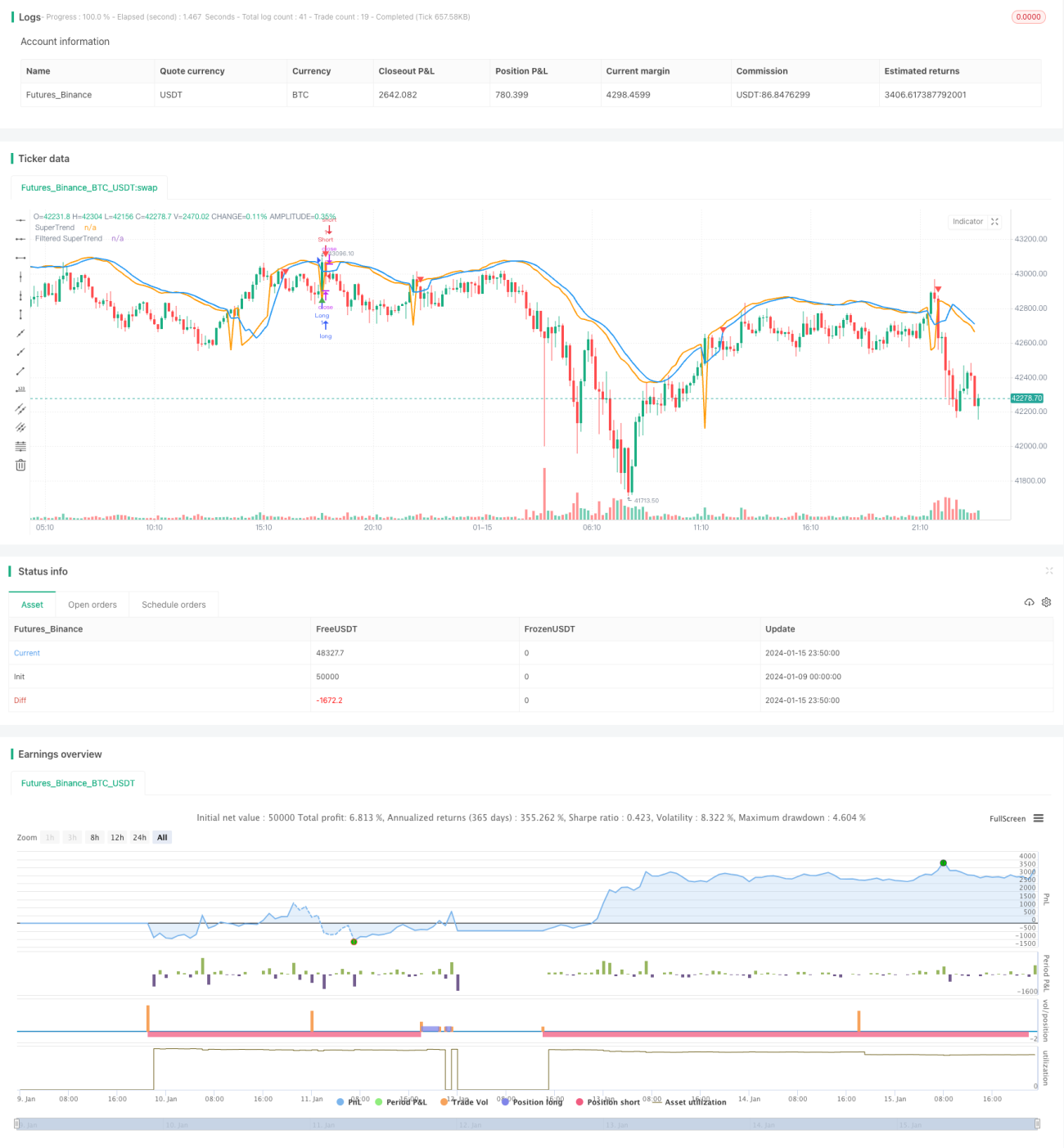

本稿では、SuperTrend指標とStochastic RSIフィルターを組み合わせた改良型トレンドフォロー戦略を詳細に分析します。この戦略は、市場トレンドを考慮しつつ、偽シグナルを低減するための買い・売りシグナルを生成することを目的としています。Stochastic RSIは、買われ過ぎ・売られ過ぎの状況における偽シグナルを回避するために使用されます。

戦略の原理

SuperTrendの計算

まず、真の変動幅(TR)と平均真の変動幅(ATR)を計算します。次にATRを用いて、上限バンドと下限バンドを計算します。

上限バンド = SMA(終値, ATR期間)+ ATR乗数 × ATR

下限バンド = SMA(終値, ATR期間)- ATR乗数 × ATR

終値が下限バンドを上回っている場合は上昇トレンド、終値が上限バンドを下回っている場合は下降トレンドとします。上昇トレンドではSuperTrendは下限バンド、下降トレンドではSuperTrendは上限バンドとなります。

フィルター機構

偽シグナルを低減するため、SuperTrendに移動平均を適用してフィルター処理後のSuperTrendを取得します。

Stochastic RSI

RSIの値を計算し、それにストキャスティクス指標を適用してStochastic RSIを生成します。これは、RSIが買われ過ぎまたは売られ過ぎの領域にあるかどうかを示します。

エントリー・エグジット条件

買い条件:終値がフィルター処理後のSuperTrendを上抜き、かつ上昇トレンドであり、かつStochastic RSI < 80

売り条件:終値がフィルター処理後のSuperTrendを下抜き、かつ下降トレンドであり、かつStochastic RSI > 20

買いのエグジット:終値がフィルター処理後のSuperTrendを下抜き、かつ上昇トレンドである場合

売りのエグジット:終値がフィルター処理後のSuperTrendを上抜き、かつ下降トレンドである場合

戦略の優位性

これは改良型トレンドフォロー戦略であり、単純な移動平均などの指標と比較して以下のような利点があります。

- SuperTrend自体が強力なトレンド識別能力とフィルターによる偽シグナル低減能力を持っています。

- フィルター機構を適用することで、さらに偽シグナルが減少し、より信頼性の高いシグナルが得られます。

- Stochastic RSIは、買われ過ぎ・売られ過ぎの状況で発生する偽シグナルを回避し、重要なサポート・レジスタンス領域付近で戦略にシグナルを発出させます。

- 戦略はトレンド方向とStochastic RSIの買われ過ぎ・売られ過ぎ状況を同時に考慮しており、トレンド追跡と偽シグナル回避のバランスが良好に取れています。

- 戦略のパラメータは柔軟に調整可能であり、様々な市場環境に適応できます。

戦略のリスクと最適化

潜在的なリスク

- 激しく変動する市場では、ストップロスが突破される可能性があります。

- SuperTrendおよびフィルター機構には遅延が生じるため、直近の価格変動を見逃す可能性があります。

- Stochastic RSIのパラメータ設定が不適切だと、戦略のパフォーマンスに影響を与える可能性があります。

リスクへの対応

- ストップロスを適切に調整するか、デフォルトのストップロスを使用します。

- ATR期間やフィルター期間のパラメータを調整して、遅延性とのバランスを図ります。

- Stochastic RSIのパラメータをテストし、最適化します。

最適化の方向性

- 異なるパラメータの組み合わせをテストし、最適なパラメータを探します。

- EMA平滑化など、異なるフィルター機構を試してみます。

- 機械学習アルゴリズムを適用して、パラメータを自動最適化します。

- 他の指標を組み合わせてエントリーの根拠を補完します。

まとめ

本戦略は、SuperTrendとStochastic RSIの2つの指標の利点を統合し、トレンドを効果的に識別して質の高い取引シグナルを発出します。また、フィルター機構により市場ノイズに対する頑健性も向上しています。この戦略はパラメータ最適化によってさらなる効果を得られるほか、他の指標やモデルとの組み合わせも検討可能です。総じて、優れたトレンド追跡能力と一定のリスク管理機構を備えており、安定した収益を求める投資家に適しています。

- 1