時空を超える莫非指標戦略

概要

これは莫非指標を用いて市場の「大物」を識別するシンプルな定量戦略です。5分足を対象とし、主に暗号通貨取引に使用します。

戦略原理

当戦略は長さ3の莫非指標を使用し、買われすぎラインを100、売られすぎラインを0に設定します。莫非指標が買われすぎレベルに達したとき、市場に「大物」が存在することを示します。当日の最初の2本の莫非指標が買われすぎ点を示した後も価格が上昇トレンドを維持している場合、それはロングエントリーシグナルとなります。

莫非指標が100になり、次のローソク足が大陽線になったときにロングエントリーします。ストップロスはその取引日の最安値に設定し、利確はエントリー後60分以内に行います。

ショートに関しては、ミラーリングロジックを使用できます。すなわち、莫非指標が売られすぎに達した後、次のローソク足が大陰線になったときにショートエントリーします。

戦略の利点

-

莫非指標を使用することで、市場における「大物」の潜在的な株の買い集め行動を効果的に識別でき、そのような銘柄は上昇を続ける可能性があります。

-

ローソク足の実体を利用して強度の高いブレイクポイントを識別することで、多くのフェイクブレイクをフィルタリングできます。

-

SMAフィルターを組み合わせることで、下落トレンドにある銘柄の買いを回避し、取引リスクを効果的に低減します。

-

日内超短期取引手法を用い、60分での利確により迅速に利益を確定し、ドローダウンの確率を低減します。

戦略のリスク

-

莫非指標が誤ったシグナルを生成し、不必要な損失を招く可能性があります。パラメータを適宜調整するか、他の指標を追加してフィルタリングすることで対応できます。

-

60分での超短期取引手法は積極的すぎる可能性があり、ボラティリティの高い銘柄には適さない場合があります。利確時間を調整するか、トレーリングストップを使用して最適化できます。

-

重要なマクロ経済イベントが発生した際の市場への影響リスクを考慮していません。そのような場合、戦略を一時停止し、市場が安定してから取引を再開すべきです。

戦略の最適化方向性

-

異なるパラメータの組み合わせ(例えば、莫非指標の長さの調整やSMA周期パラメータの最適化)をテストできます。

-

ボリンジャーバンドやKD指標など他の指標を追加し、シグナルの精度が向上するかどうかを試すことができます。

-

ストップロス幅を適度に緩和することで、1回あたりの利益が拡大するかをテストできます。

-

本戦略フレームワークに基づき、15分足や30分足など他の時間軸に対応したバージョンを開発してみることも可能です。

まとめ

本戦略は全体的に非常にシンプルで理解しやすく、基本的な考え方は古典的な「大物」追跡手法と一致しています。莫非指標の買われすぎ・売られすぎの重要なポイントを識別し、ローソク足の実体でフィルタリングすることで、多くのノイズを排除できます。SMAフィルターの追加により、戦略の安定性がさらに向上しています。

60分での超短期取引手法により迅速に利益を得られますが、同時に高い取引リスクも伴います。全体として、この戦略は実戦価値の高い定量戦略テンプレートであり、さらなる研究と最適化に値します。また、戦略開発の貴重なアイデアを提供してくれます。

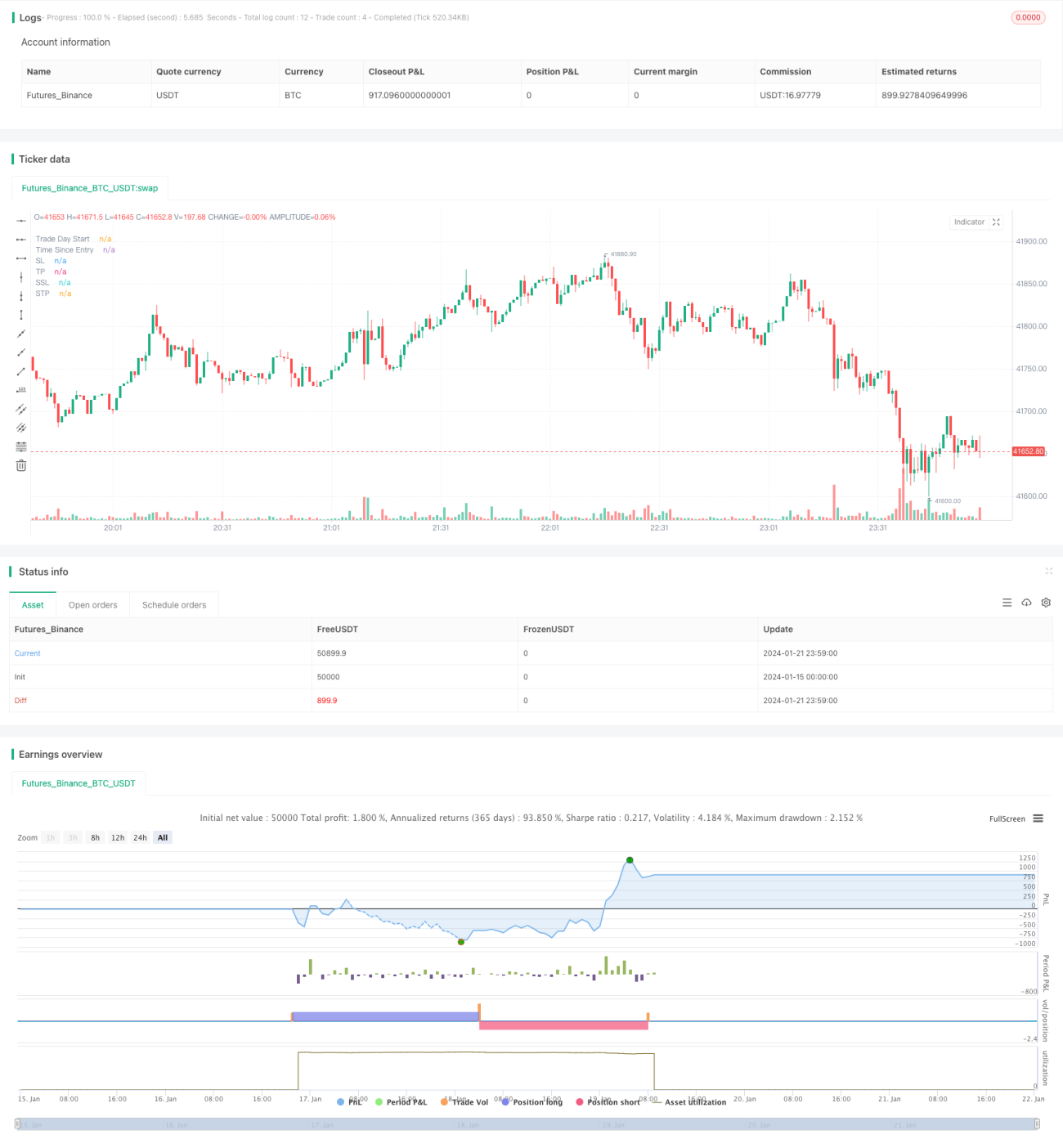

/*backtest

start: 2024-01-15 00:00:00

end: 2024-01-22 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// From "Crypto Day Trading Strategy" PDF file.

- 1