ダブル移動平均線価格チャネルトレンド追跡戦略

概要

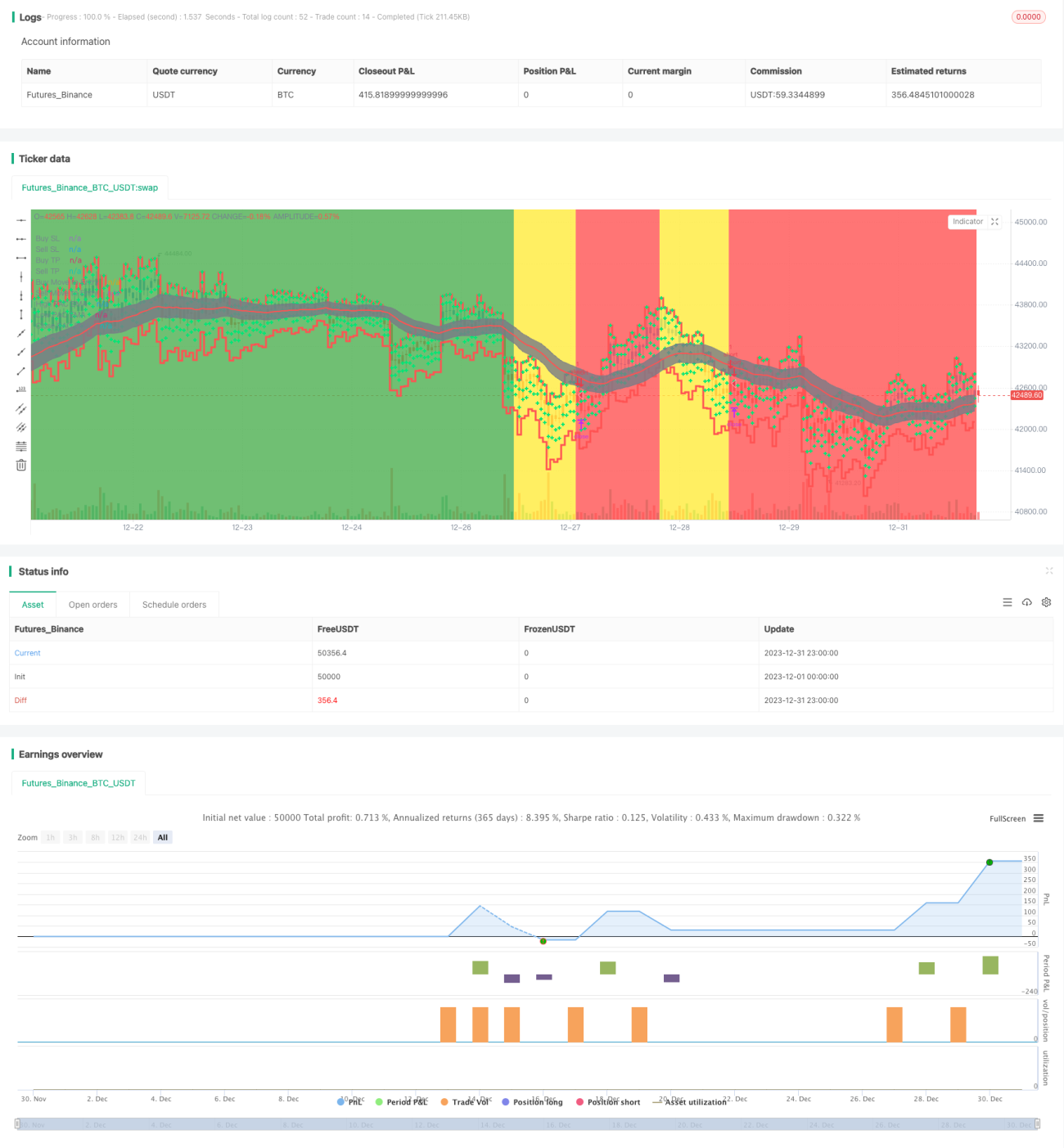

この戦略は、二重移動平均線に基づいて価格チャネルを構築し、チャネル範囲を使用して価格トレンドの方向を判断し、ストップロストレーリングを設定して利益を確定するトレンド追跡戦略です。

戦略の原理

二重移動平均線価格チャネル戦略は、短期EMAと長期EMAを使用して価格チャネルを構築します。短期EMAの期間は89、長期EMAの期間は200です。同時に、高値、安値、終値に基づく3本の移動平均線を使用して価格チャネル範囲を構築します。チャネルの上限線と下限線は、それぞれ34期間の高値EMAと安値EMAです。

短期EMAが長期EMAよりも上にあり、かつ価格が下限線を下回っている場合、上昇トレンドと判断します。短期EMAが長期EMAよりも下にあり、かつ価格が上限線を上回っている場合、下降トレンドと判断します。

上昇トレンドの場合、戦略はトレンド反転が確定した時点で空売りを行います。下降トレンドの場合、戦略はトレンド反転が確定した時点で買いを行います。

さらに、この戦略にはストップロストレーリング機能が備わっています。ポジション保有後、ストップロス価格をリアルタイムで更新し、利益を確定します。

優位性分析

この戦略の最大の利点は、二重移動平均線を使用して価格チャネルを構築し価格トレンドを判断した上で、反転時にエントリーすることで、高値追いや安値売りを回避できる点です。同時に、移動ストップロストレーリングにより利益を確定し、損失リスクを低減します。

その他の利点としては、パラメータの最適化の余地が大きく、さまざまな銘柄や時間枠に調整可能であること、ストップロス価格がリアルタイムで更新されるため運用リスクが低いことなどが挙げられます。

リスク分析

この戦略の主なリスクは、反転シグナルの判定精度が不十分で、誤判定が発生する可能性があることです。その場合はパラメータを最適化し、トレンド反転の確定効果を確実にする必要があります。

また、ストップロスの設定も非常に重要です。ストップロス幅が大きすぎると、十分なタイミングでロスカットできない可能性があります。逆に小さすぎると、過度なロスカットが発生する可能性があります。これは対象銘柄に応じて調整する必要があります。

最後に、データの問題によって戦略が無効になる可能性もあります。信頼性が高く、連続的で十分な履歴データを使用してバックテストと実運用による検証を行うことが重要です。

最適化の方向性

この戦略の最適化は主に以下の点に集中します。

- 短期EMAと長期EMAの期間を最適化し、異なるパラメータの組み合わせで効果を検証する

- 価格チャネルの上限線と下限線のパラメータも調整し、より適切な期間パラメータを模索する

- ストップロスの設定が重要であるため、さまざまなパラメータをテストしてストップロス戦略を最適化する

- トレンド反転を確定するために他の指標を導入するかどうかをテストし、エントリー精度を向上させる

まとめ

本戦略は全体的な運用フローが合理的かつスムーズで、二重移動平均線チャネルによるトレンド方向の判断に基づいてエントリーし、移動ストップロスで利益を確定する、比較的安定したトレンド追跡戦略です。パラメータ最適化とリスク管理設定の最適化により、本戦略は効率的な定量取引戦略の一つとなり得ます。

- 1