ドンチャンのトレンド追跡戦略

概要

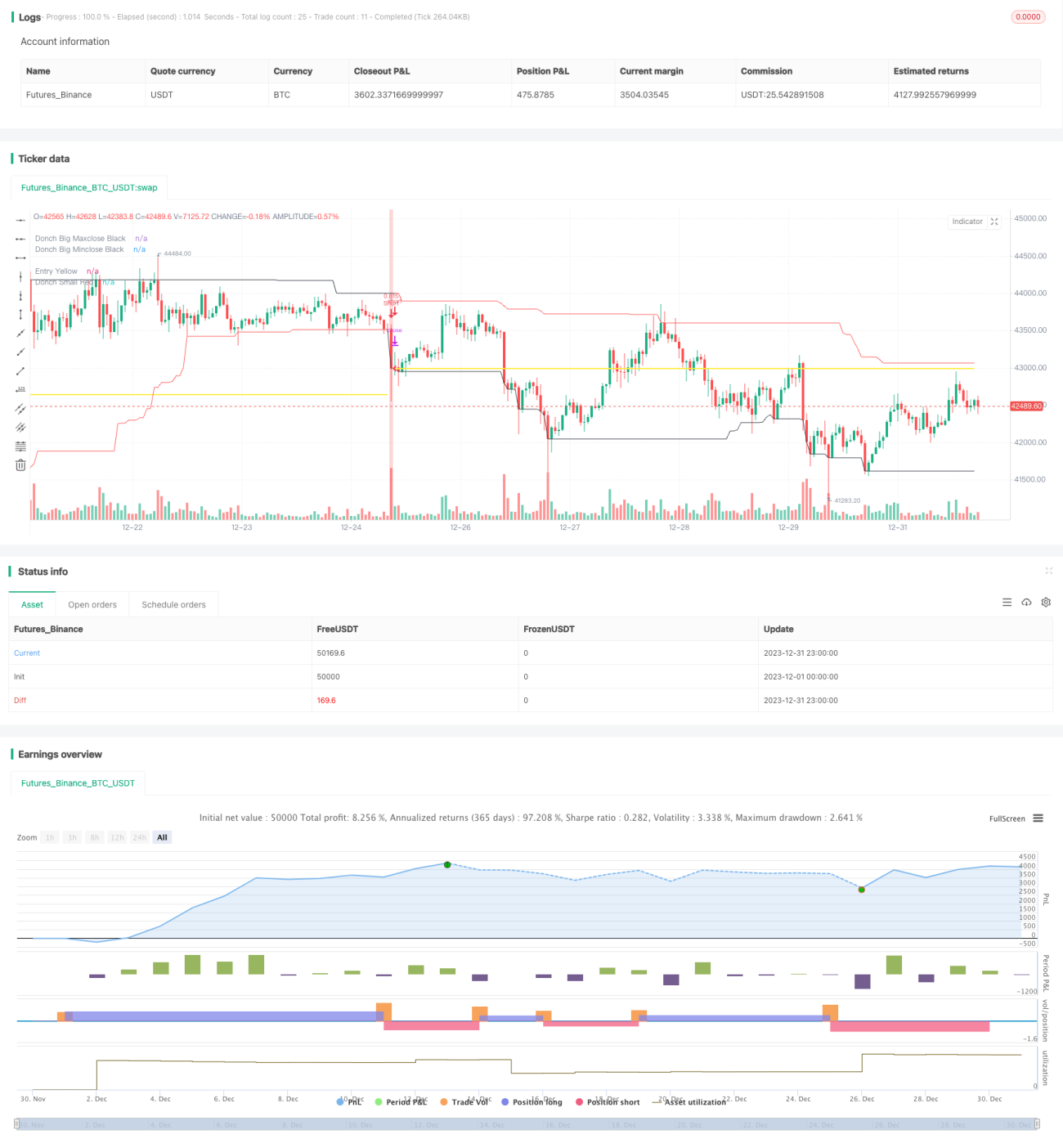

ドンチアン・トレンドフォロー戦略は、記事「Black Box Trend Following – Lifting the Veil」で説明されているドンチアンチャネルの原理に基づいて開発されたトレンドフォロー戦略です。この戦略は、ドンチアンチャネルを使用して価格のトレンドを判断し、価格が新高値または新安値を更新した際にロングまたはショートのポジションを取ります。

戦略の原理

この戦略は、ドンチアンチャネル指標に基づいてトレンドの方向性を判断します。ドンチアンチャネルは、より長い期間のチャネルとより短い期間のチャネルの2つで構成されます。価格が長い期間のチャネルをブレイクした場合、トレンドの開始と判断し、価格が短い期間のチャネルをブレイクした場合、トレンドの終了と判断します。

具体的には、長い期間のチャネルの長さは50日または20日、短い期間のチャネルの長さは50日、20日、または10日です。価格が50日間の最高値に等しい場合、ロングポジションを取ります。価格が50日間の最安値に等しい場合、ショートポジションを取ります。価格が20日間または10日間の最安値に等しい場合、ロングポジションを決済します。価格が20日間または10日間の最高値に等しい場合、ショートポジションを決済します。

これにより、異なる2つの期間のドンチアンチャネルを組み合わせることで、トレンドの開始時に方向性を決定してポジションを取り、トレンドの終了時に適切にストップロスを行ってポジションを離脱します。

優位性分析

この戦略の主な利点は以下の通りです。

-

トレンドを捉える能力が高い。ドンチアンチャネルのブレイクによってトレンドの開始と終了を判断することで、トレンドを効果的に追跡できます。

-

リスク管理が適切。トレーリングストップを使用して1回の取引の損失を管理します。

-

パラメーター調整が柔軟。チャネルの期間の組み合わせを自由に選択でき、異なる銘柄や市場環境に対応できます。

-

明確でシンプルな取引ロジック。理解・実装が容易です。

リスク分析

本戦略には以下のリスクも存在します。

-

レンジ相場に対応できない。トレンドが明確でない場合、小幅な調整が繰り返され、ストップロスによる損失が発生します。

-

ブレイク失敗のリスク。価格がチャネルをブレイクした後、再び押し戻される可能性があり、ストップロスが発生します。

-

期間選択のリスク。チャネルの期間設定が適切でない場合、ノイズの中での取引(trading in noise)につながります。

-

シャープレシオ低下のリスク。ポジションサイズを大きくしながらストップロスの幅を調整しない場合、シャープレシオが低下するリスクがあります。

対応策:

- パラメーターを最適化し、適切なチャネルの期間組み合わせを選択する。

- ポジションサイズとストップロスの幅を適宜調整し、リスクを管理する。

- トレンドが明確な銘柄や市場で本戦略を使用する。

最適化の方向性

本戦略は以下の方向で最適化が可能です。

-

フィルター条件を追加し、ダマシを回避する。例えば出来高指標などを組み合わせて真のブレイクを判断する。

-

チャネルの期間の組み合わせとポジションサイズ管理を最適化し、損益比を向上させる。適応型ストップロス機構を導入することも検討する。

-

ブレークポイント最適化を試み、最適なパラメーターの組み合わせを見つける。

-

機械学習アルゴリズムを追加し、パラメーターの動的最適化と調整を実現する。

まとめ

ドンチアン・トレンドフォロー戦略は、2つのチャネルを使用して価格トレンドの開始と終了を判断し、トレンドフォローの取引方法を採用することで、1回の取引の損失を効果的に管理します。この戦略はパラメーター調整が柔軟で実装も容易であり、非常に実用的なトレンドフォロー戦略です。ただし、レンジ相場での収益性不足やパラメーター選択によるリスクにも注意が必要です。さらなる最適化により、より良い戦略パフォーマンスを得ることができます。

- 1