モメンタム絶対値インジケーター戦略

1

Follow

1802

Followers

概要

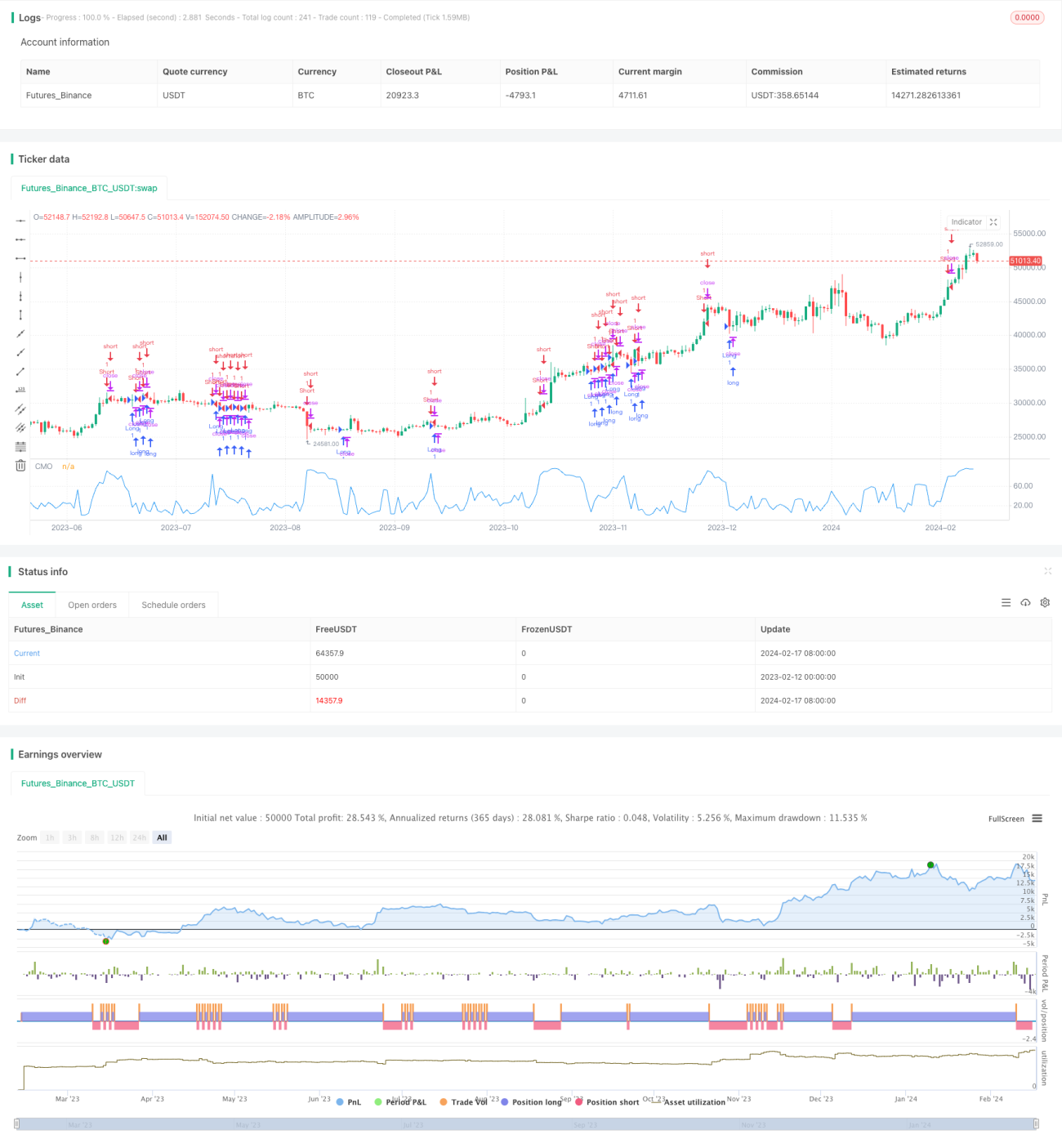

モメンタム絶対値インジケーター戦略は、Tushar Chandeが開発したモメンタム指標CMOの改良版です。この戦略は価格の絶対モメンタム値を計算することで、市場が現在買われすぎや売られすぎの状態にあるかどうかを判断し、中期の価格変動を捉えます。

戦略の原理

本戦略の核となる指標は、改良版CMOであるAbsCMOです。AbsCMOの計算式は以下の通りです。

AbsCMO = abs(100 * (最新終値 - Length期間前の終値) / (Length期間内の価格変動絶対値の単純移動平均 * Length))

ここでLengthは平均期間の長さを表します。AbsCMOの値域は0から100です。この指標はモメンタムの方向性と強度を組み合わせており、市場の中期的なトレンドや買われすぎ・売られすぎの領域を明確に判断できます。

AbsCMOが指定された上限線(デフォルト70)を上抜けた場合、市場が買われすぎ状態に入ったことを示し、売りシグナルとなります。AbsCMOが指定された下限線(デフォルト20)を下抜けた場合、市場が売られすぎ状態に入ったことを示し、買いシグナルとなります。

優位性分析

他のモメンタム指標と比較して、AbsCMO指標には以下のような利点があります。

- 価格の絶対モメンタムを反映するため、市場の中期的なトレンドをより正確に判断できます。

- 方向性と強度を組み合わせることで、買われすぎ・売られすぎの識別がより明確です。

- 値域が0~100に限定されているため、複数の銘柄間での比較に適しています。

- 短期的な激しい変動に影響されにくく、市場の中期的なトレンドを反映します。

- パラメータをカスタマイズでき、適応性が高いです。

リスク分析

本戦略には主に以下のリスクがあります。

- 中期指標であるため、短期的な変動への反応が十分ではありません。

- デフォルトパラメータがすべての銘柄に適しているとは限らず、最適化が必要です。

- 長期保有により大きなドローダウンが発生する可能性があります。

保有期間を適切に短縮したり、パラメータを最適化したり、他の指標と組み合わせて使用することでリスクを軽減できます。

最適化の方向性

本戦略は以下の点から最適化が可能です。

- AbsCMOのパラメータを最適化し、より多くの銘柄に適応させる。

- 他の指標を組み合わせて偽シグナルをフィルタリングする。

- ストップロスと利益確定ルールを設定し、リスクを管理する。

- 深層学習などの技術を活用して、より優れたエントリーポイントを見つける。

まとめ

モメンタム絶対値インジケーター戦略は、全体として実用的な中期トレード戦略です。価格の中期的な絶対モメンタム特性を反映し、市場の中期的なトレンドを判断する能力に優れています。しかし、短期的な激しい変動には鈍感で、一定のリスクが存在します。パラメータ最適化、インジケーターによるフィルタリング、ストップロスメカニズムなどのさらなる改善により、本戦略の実運用でのパフォーマンスをより安定・信頼性の高いものにすることができます。

Source

Pine

/*backtest

start: 2023-02-12 00:00:00

end: 2024-02-18 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 17/02/2017

// This indicator plots the absolute value of CMO. CMO was developed by Tushar Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1