二重逆転モメンタム戦略に基づく

概要

ダブルリバーサルモメンタム戦略は、価格反転シグナルとボラティリティ反転シグナルを組み合わせることで、トレンド取引を実現します。主に123パターンに基づいて価格反転ポイントを判断し、同時にドンチャンチャンネルのボラティリティを使用して偽のシグナルをフィルタリングします。この戦略は中長期のポジション保有に適しており、ダブルリバーサルフィルタリングにより市場の転換点を効果的に捉え、超過収益を実現できます。

戦略原理

価格反転部分では123パターンを使用して判断します。このパターンの意味は、最初の2本のローソク足で価格が逆方向(上昇または下落)に動き、3本目のローソク足で再び反転(下落または上昇)することから、123パターンと呼ばれます。価格に3本のローソク足の反転現象が現れた場合、通常は短期的なトレンドがまもなく転換することを示しています。価格反転の信頼性をさらに検証するために、この戦略ではストキャスティクス指標も使用して判断し、ストキャスティクスも反転した場合(快速線が下落または急速に上昇)にのみ取引シグナルが発せられます。

ボラティリティ反転部分ではドンチャンチャンネルのボラティリティを使用します。ドンチャンチャンネルは主に価格の変動範囲を反映します。価格変動が大きくなるとドンチャンチャンネルの幅も拡大し、価格変動が小さくなるとドンチャンチャンネルの幅も狭まります。ドンチャンチャンネルのボラティリティ(幅)は市場の変動度合いとリスクレベルを効果的に測定できます。この戦略ではドンチャンチャンネルのボラティリティの反転を使用して偽のシグナルをフィルタリングし、ボラティリティと価格の両方が同時に反転した場合にのみ取引シグナルを発し、迂回操作に巻き込まれるのを防ぎます。

以上より、この戦略はダブルリバーサル検証により、取引シグナルの信頼性を確保するとともにリスクをコントロールし、比較的堅実なトレンド戦略です。

戦略の利点

- ダブルフィルタリングメカニズムにより、取引シグナルの信頼性を確保し、誤ったブレイクを回避

- リスクをコントロールし、損失確率を低減

- 中長期のポジション保有に適し、市場ノイズを避け、超過収益を捉える

- パラメータ最適化の余地が大きく、最適な状態に調整可能

- 独自のスタイルで、一般的なテクニカル指標と組み合わせて使用すると効果的

戦略のリスク

- パラメータ最適化に依存しており、適切でないパラメータは戦略のパフォーマンスに影響を与える

- ストップロス戦略はさらに改善が必要で、最大ドローダウンのコントロールに改良の余地がある

- 取引頻度が低くなる可能性があり、高頻度アルゴリズム取引には対応できない

- 適切な銘柄と時間枠を選択する必要があり、適用範囲が限られる

- 機械学習などを用いて最適パラメータを探索することができる

最適化の方向性

- 適応型ストップロスモジュールを追加することで、最大ドローダウンを大幅に削減できる

- 出来高指標を追加し、高出来高のブレイクアウト時に入場することを確保

- パラメータを最適化して最適な安定性を得る

- 異なる銘柄や時間枠を試し、最適な適合環境を探す

- 他の指標や戦略と組み合わせて、1+1>2の相乗効果を得る

まとめ

ダブルリバーサルモメンタム戦略は、価格反転とボラティリティ反転の二重検証により、優れたリスク管理を実現します。単一の指標と比較して、大量のノイズをフィルタリングし、より高い安定性を発揮します。パラメータ最適化、ストップロスモジュールの強化、出来高の導入などの手段により、シグナルの品質と収益の安定性をさらに向上させることができます。この戦略は、株式や暗号資産などの中長期戦略の構成要素として適しており、他のモジュールと適切に組み合わせることで良好な超過収益を得ることができます。

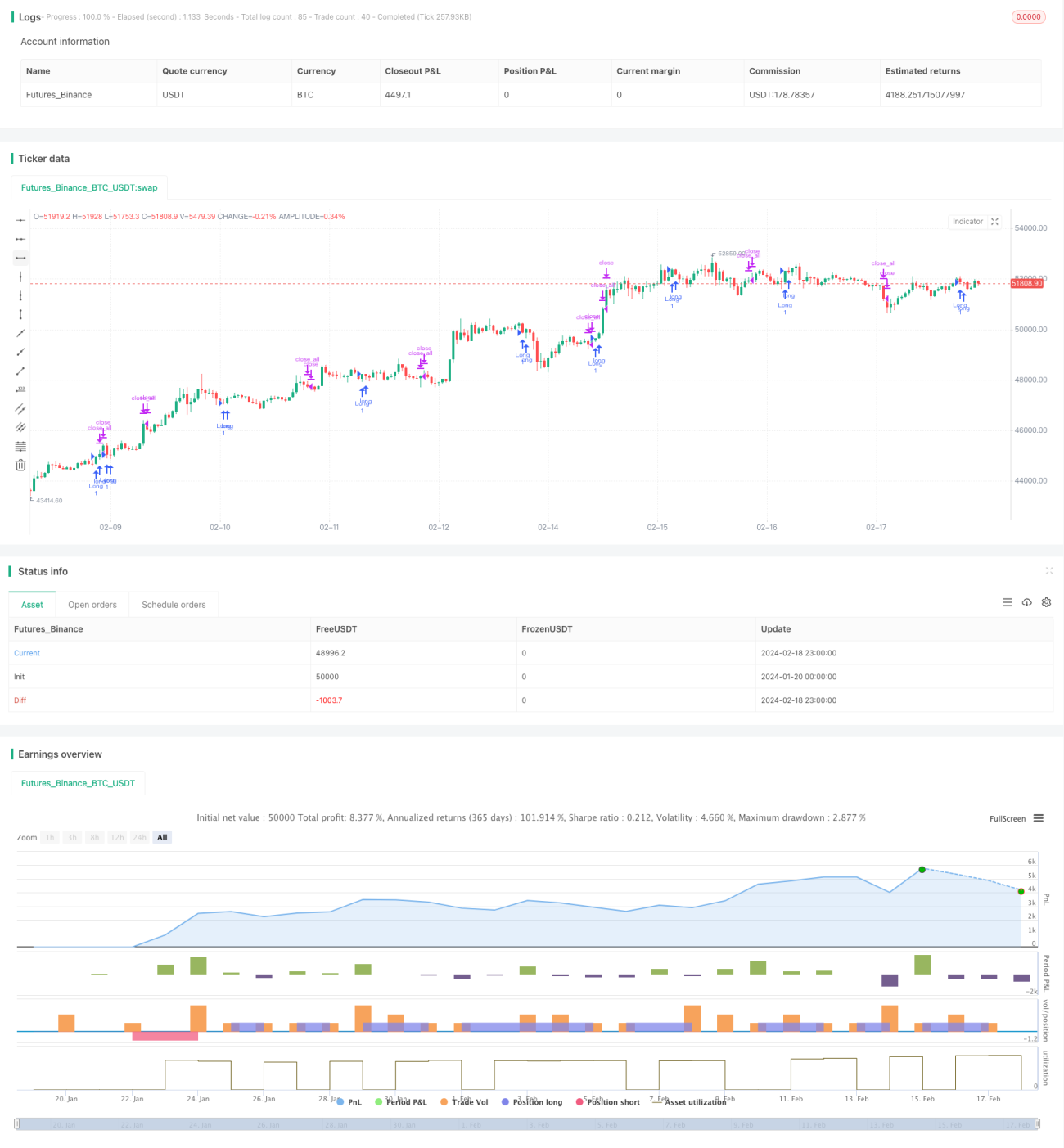

/*backtest

start: 2024-01-20 00:00:00

end: 2024-02-19 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 06/03/2020

// This is combo strategies for get a cumulative signal. - 1