모멘텀 돌파 추세 추종 전략

개요

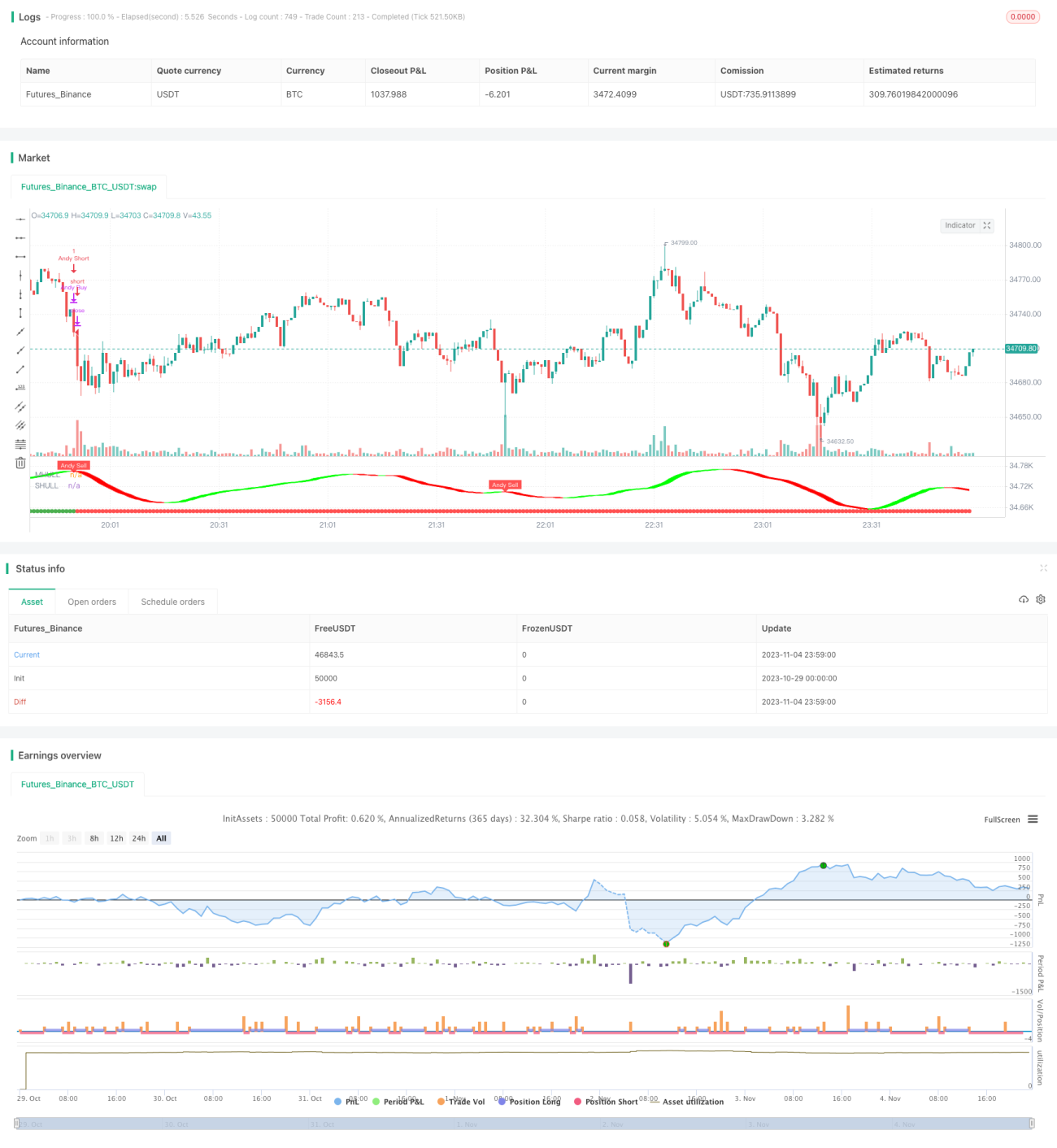

본 전략은 다양한 기술적 지표를 종합하여 추세 방향을 식별하고, 추세가 모멘텀 돌파를 일으킬 때 추적하여 초과 수익을 추구합니다.

전략 원리

-

Donchian 채널을 사용하여 전체 추세 방향을 판단합니다. 가격이 채널을 돌파하면 추세 전환이 확인됩니다.

-

Hull 이동 평균선은 추세 방향을 보조적으로 판단합니다. 이 지표는 가격 변화에 민감하여 추세 전환을 조기에 발견할 수 있습니다.

-

반 궤도 시스템은 매수 및 매도 신호를 발생시킵니다. 이 시스템은 가격 채널과 평균 실제 변동 범위를 기반으로 하여 거짓 돌파를 방지합니다.

-

Donchian 채널, Hull 지표 및 반 궤도 시스템이 동시에 신호를 보낼 때, 추세가 강력한 모멘텀 돌파를 일으켰다고 판단하여 매수에 진입합니다.

-

청산 조건: 위 지표들이 반대 신호를 보낼 때 추세 반전으로 판단하고 즉시 손절하여 이탈합니다.

장점 분석

-

여러 지표 조합으로 판단력 향상. Donchian 채널은 기본 방향, Hull 지표와 반 궤도는 세부 사항을 판단하여 추세의 정확한 전환점을 파악합니다.

-

모멘텀 돌파 참여로 초과 수익 추구. 강력한 돌파 시에만 진입하여 변동성 구간에서 갇히는 것을 방지합니다.

-

엄격한 손절로 자금 안전 보장. 지표가 반대 신호를 보내면 즉시 손절하여 손실 확대를 방지합니다.

-

매개변수 조정이 유연하여 다양한 시장에 적응. 채널 길이, 변동 범위 등을 조정하여 여러 주기에 최적화 가능합니다.

-

이해하고 구현하기 쉬워 초보자도 습득 가능. 지표와 조건 조합이 간단명료하여 프로그래밍 구현이 용이합니다.

위험 분석

-

초기 추세 기회를 놓칠 수 있음. 진입 시점이 늦어 초기 상승분을 포착하지 못함.

-

돌파 실패 시 되돌림 손실. 진입 후 돌파 실패 및 반전 발생 시 손실이 발생할 수 있음.

-

지표 오류 신호 가능성. 매개변수 설정 부적절로 인해 잘못된 판단이 발생할 수 있음.

-

거래 횟수 제한. 명확한 추세 돌파 시에만 진입하므로 연간 거래 횟수가 제한적임.

최적화 방향

-

매개변수 조합 최적화. 다양한 매개변수를 테스트하여 최적 조합 도출.

-

손절 라인 후퇴 조건 추가. 너무 이른 손절을 방지하여 추세 기회를 놓치지 않도록 함.

-

다른 지표 필터 추가. MACD, KDJ 등을 보조 판단에 활용하여 오류 신호 감소.

-

거래 시간대 최적화. 시간대별 매개변수 최적화 가능.

-

자금 효율성 향상. 레버리지, 정기 투자 등을 통해 자금 사용 효율 증대.

요약

본 전략은 여러 지표를 종합하여 추세의 모멘텀 돌파 시점을 판단하고, 이미 형성된 추세를 추적하여 초과 수익을 실현합니다. 엄격한 손절 메커니즘으로 리스크를 관리하고, 유연한 매개변수 조정으로 다양한 시장 환경에 적응합니다. 거래 빈도는 낮지만 각 거래에서 높은 수익을 추구합니다. 매개변수 최적화, 보조 지표 도입 등을 통해 지속적인 개선이 가능합니다.

- 1