공간 지향적 가격 반전 전략

1

Follow

1802

Followers

개요

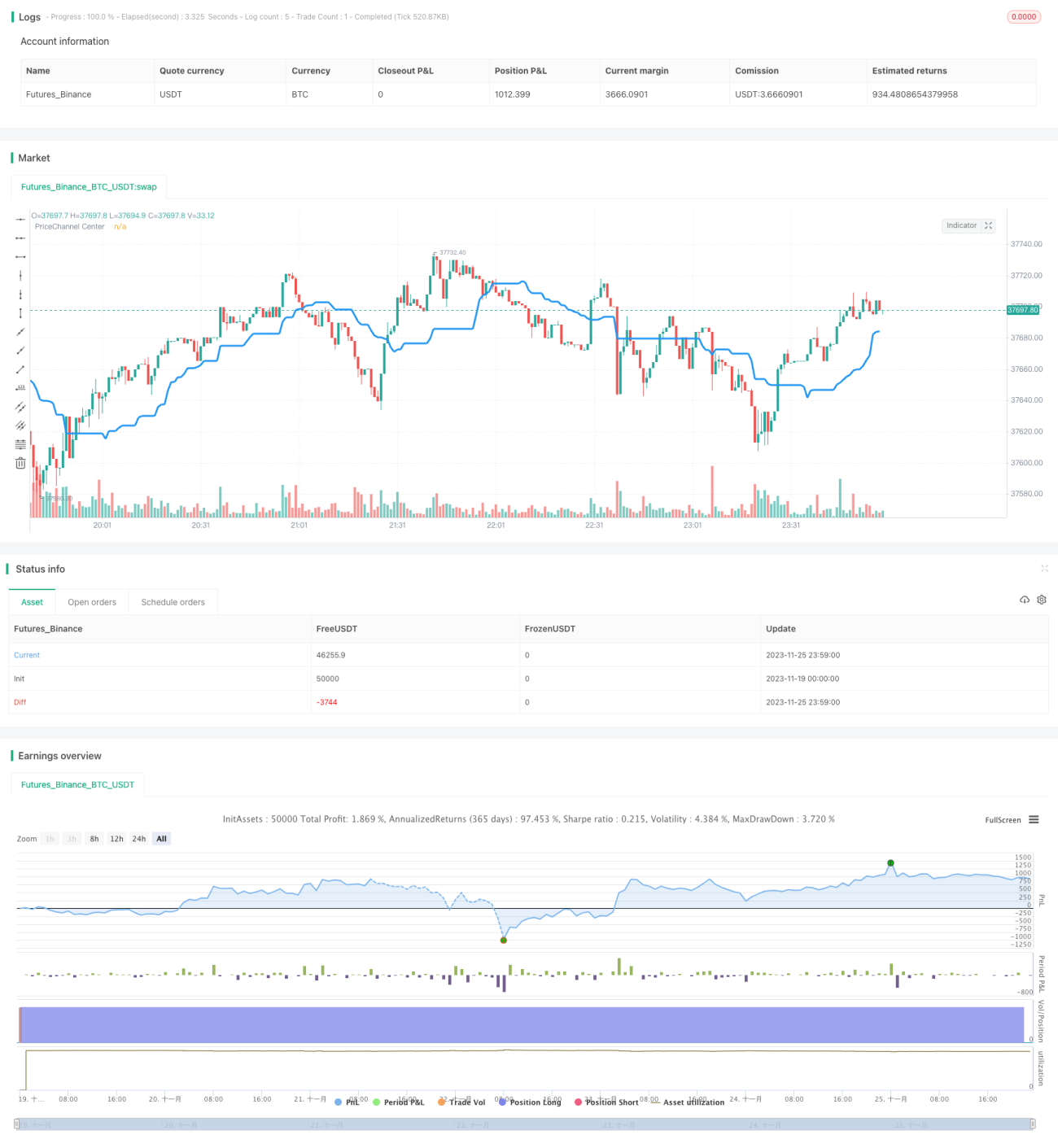

공간 지향 가격 반전 전략은 가격 채널 중심선을 계산하여 가격 변동의 추세 방향을 판단합니다. 가격이 채널 중심선에 근접하면 매수 또는 매도 신호를 발생시킵니다. 이 전략은 여러 필터 조건을 결합하여 높은 확률의 거래 기회를 찾습니다.

전략 원리

이 전략의 핵심 지표는 가격 채널 중심선입니다. 계산 방식은 최근 30개 캔들의 최고가와 최저가의 평균을 취하는 것입니다. 저점이 중심선보다 높으면 상승 추세, 고점이 중심선보다 낮으면 하락 추세로 간주합니다.

전략은 추세 배경이 전환될 때만 거래 신호를 발생시킵니다. 즉, 상승 배경에서는 캔들이 빨간색일 때만 매도하고, 하락 배경에서는 캔들이 초록색일 때만 매수합니다.

또한 이중 필터 조건을 설정합니다: 캔들 몸통 필터와 가격 채널 bars 필터. 캔들 몸통의 크기가 평균의 20%보다 클 때만 신호가 트리거되며, 필터 기간 내에 연속적인 추세 신호가 있어야 포지션을 오픈합니다.

장점 분석

이 전략은 추세, 가치 영역 및 캔들 패턴을 결합한 효율적인 반전 거래 전략입니다. 주요 장점은 다음과 같습니다.

- 가격 채널을 사용하여 주요 추세를 판단하여 변동장에서의 오도를 방지합니다.

- 가격 채널 중심선 근처에서 포인트를 선택하여 고전적인 저가 매수, 고가 매도 영역을 활용합니다.

- 캔들 몸통 및 채널 bars 필터가 신호 품질을 높여 오류 신호율을 낮춥니다.

- 명확한 반전 지점에서만 포지션을 오픈하여 추격 매수/매도를 피합니다.

위험 및 해결 방법

이 전략의 주요 위험은 가격 반전 지점을 놓치고 불필요하게 신호를 기다리는 데서 발생합니다. 다음과 같은 방법으로 최적화할 수 있습니다.

- 필터 조건의 엄격함을 조정하여 필터 기준을 낮추면 누락률을 줄일 수 있습니다.

- 반전 추세 초기에 포지션 크기를 늘려 추세 이익을 추적할 수 있습니다.

- 다른 지표와 결합하여 반전 신호 강도를 판단하고 주관적으로 필터 조건을 조정할 수 있습니다.

최적화 방향

이 전략은 다음과 같은 측면에서 최적화할 수 있습니다.

- 매개변수 최적화: 가격 채널 기간, 채널 bars 수 등의 매개변수 조정.

- 손절매 전략 추가: 손실이 일정 비율에 도달하면 손절매.

- 거래량 결합: 거래량에 따른 필터 조건 강도 조절(예: 거래량 증가 시 필터 완화).

- 머신러닝 모델 추가: 추세 전환 확률 판단을 위해 단순 필터 대체.

요약

공간 지향 가격 반전 전략은 가격 채널을 통해 반전 시점을 판단하고 이중 필터 조건을 설정하여 고품질 신호를 생성합니다. 매개변수 최적화와 리스크 관리 기반에서 신뢰할 수 있는 퀀트 전략입니다.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1