모멘텀 상품 선택 지수 전략

개요

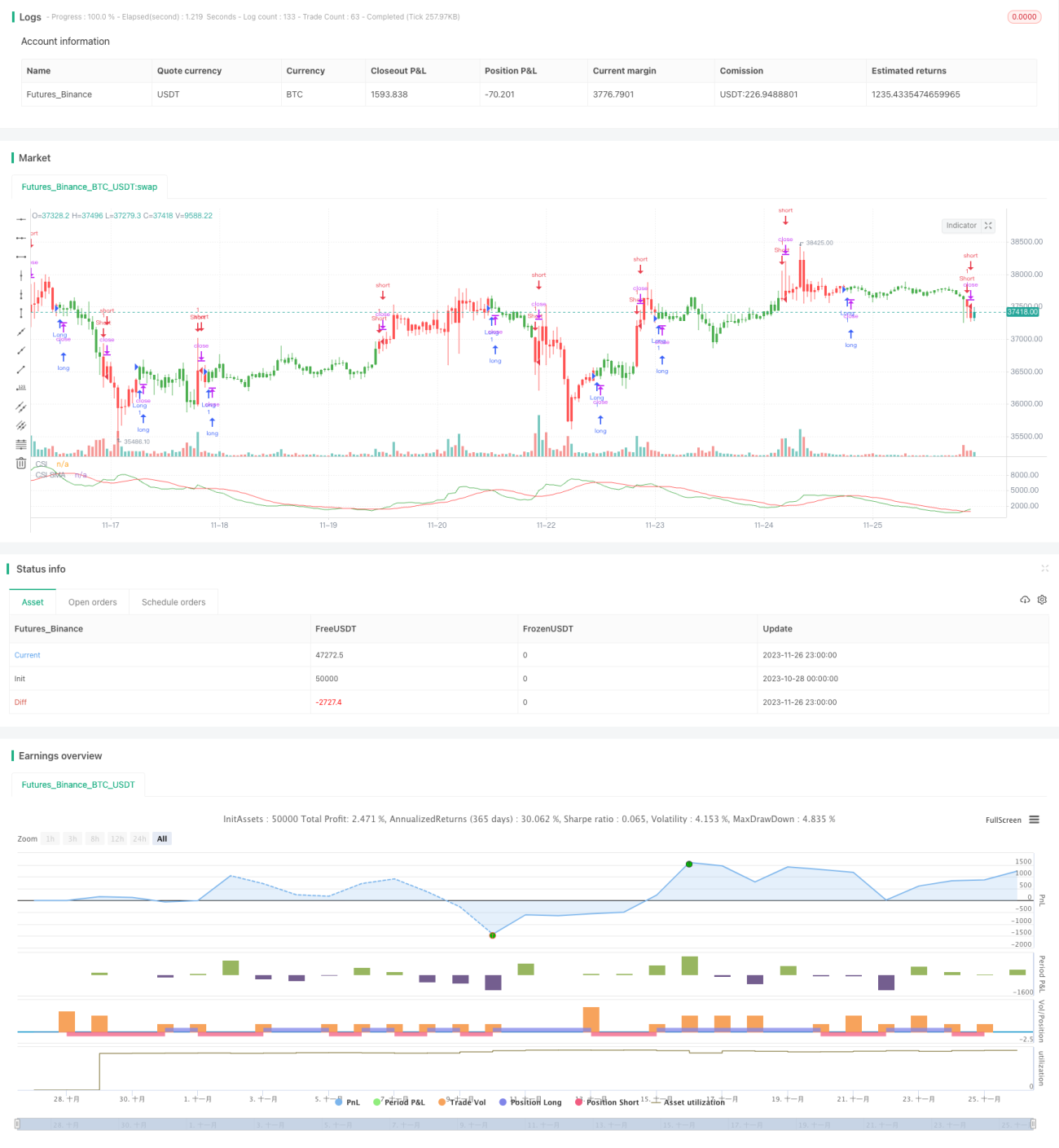

모멘텀 상품 선택 지수(Commodity Selection Index, CSI) 전략은 시장 모멘텀을 추적하는 단기 거래 전략입니다. 상품의 추세성과 변동성을 계산하여 강력한 모멘텀을 가진 상품을 식별하고 거래합니다. 이 전략은 Welles Wilder가 그의 저서 《New Concepts in Technical Trading Systems》에서 제안했습니다.

전략 원리

이 전략의 핵심 지표는 CSI 지수로, 상품의 추세성과 변동성을 종합적으로 고려합니다. 구체적인 계산 방법은 다음과 같습니다.

CSI = K × ATR × ((ADX + ADX의 n일 이동평균) / 2)

여기서 K는 스케일링 계수이고, ATR은 평균 실제 변동 범위(Average True Range)로 시장의 변동성을 측정합니다. ADX는 평균 방향 지수(Average Directional Index)로 시장의 추세성을 반영합니다.

각 상품의 CSI 지수 값을 계산하여 해당 상품의 n일 단순 이동평균선과 비교합니다. CSI가 이동평균선보다 높으면 매수 신호, 낮으면 매도 신호가 발생합니다.

이 전략은 CSI 지수가 높은 상품을 선택하여 거래합니다. 이러한 상품은 추세성과 변동성이 강하여 단기간에 더 큰 수익 잠재력을 얻을 수 있기 때문입니다.

장점 분석

해당 전략은 다음과 같은 장점을 가지고 있습니다.

- 시장 모멘텀을 포착하여 상품의 추세성과 변동성 특성을 최대한 활용할 수 있습니다.

- 이중 지표를 사용하여 거래 신호의 신뢰성을 높입니다.

- 간단하고 명확한 거래 규칙으로 자동 거래에 적합합니다.

- 단기 거래 전용으로 설계되어 단기 기회를 신속하게 포착할 수 있습니다.

위험 분석

해당 전략에는 다음과 같은 위험도 존재합니다.

- 기술 지표에 과도하게 의존하여 잘못된 신호가 발생할 수 있습니다.

- 모멘텀 추적 특성으로 인해 단기 거래에만 적합합니다.

- 변동성이 지나치게 크면 손절매가 유발되어 거래에 손실을 초래할 수 있습니다.

- 일정 수준의 레버리지를 감당해야 하므로 더 큰 자금 위험에 직면할 수 있습니다.

위험을 통제하기 위해서는 손절매 위치를 합리적으로 설정하고, 단일 포지션 규모를 관리하며, 다양한 시장 환경에 맞게 매개변수를 적절히 조정해야 합니다.

최적화 방향

이 전략은 다음과 같은 측면에서 최적화할 수 있습니다.

- 더 많은 매개변수 조합을 테스트하여 최적의 매개변수를 찾습니다.

- 다른 보조 지표를 추가하여 신호를 필터링합니다.

- 변동성 역전 등 다른 전략과 결합하여 조합 전략을 구성합니다.

- 머신러닝 모델을 학습시켜 더 신뢰할 수 있는 거래 신호를 생성합니다.

요약

모멘텀 상품 선택 지수 전략은 시장에서 추세성과 변동성이 큰 상품을 포착하여 간단하고 빠른 단기 거래를 구현합니다. 이러한 모멘텀 추적 방식은 신호를 명확하게 하고 자동화를 쉽게 적용할 수 있게 합니다. 물론 위험을 통제하고 시장 환경 변화에 맞춰 지속적으로 개선 및 업그레이드하는 것도 중요합니다.

/*backtest

start: 2023-10-28 00:00:00

end: 2023-11-27 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 20/03/2019

// The Commodity Selection Index ("CSI") is a momentum indicator. It was - 1