이중 이동평균선 교차 추세 추종형 전략

1

Follow

1802

Followers

개요

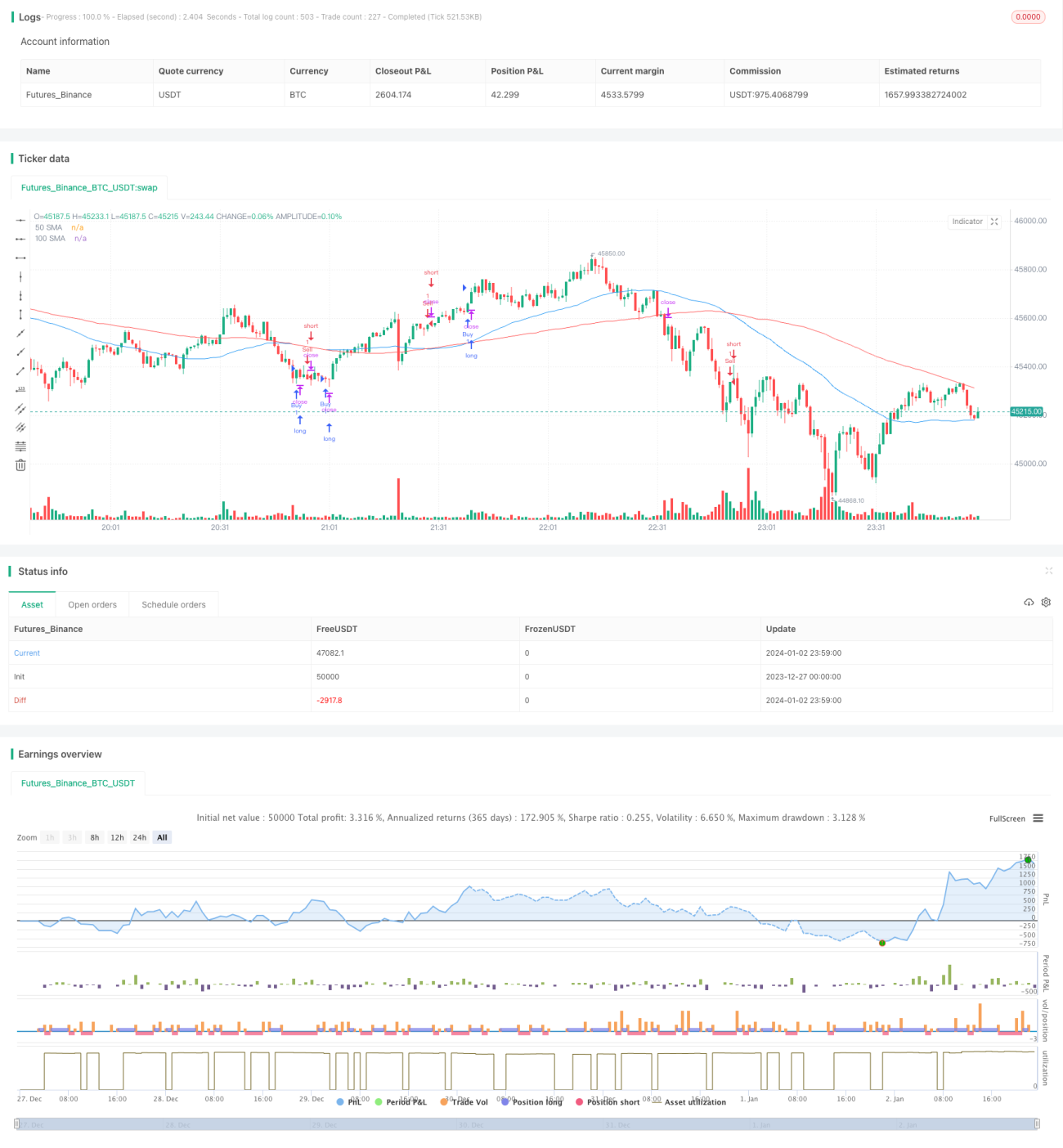

본 전략은 단순 이동평균선 교차와 평균 진폭 범위(ATR) 지표를 활용하여 매수 및 매도 신호를 생성하는 추세 추종형 전략입니다. 주로 50일 이동평균선과 100일 이동평균선의 교차를 통해 추세를 판단하고, ATR 지표를 이용해 손절매 지점을 설정하여 위험을 관리합니다.

전략 원리

- 50일 단순 이동평균선(SMA1)과 100일 단순 이동평균선(SMA2)을 계산합니다.

- SMA1이 SMA2를 상향 돌파하면 매수 신호를, SMA1이 SMA2를 하향 돌파하면 매도 신호를 발생시킵니다.

- 14일 ATR 지표를 계산합니다.

- ATR에 설정된 승수를 곱한 값을 손절매 지점으로 사용합니다.

- 매수 신호 발생 시 종가에서 손절매 지점을 뺀 값을 손절매(매도) 지점으로, 매도 신호 발생 시 종가에 손절매 지점을 더한 값을 손절매(매수) 지점으로 설정합니다.

즉, 이 전략은 이동평균선의 추세 판단 능력과 ATR 지표의 위험 관리 능력에 주로 의존합니다. 기본 원리는 간단명료하여 이해와 구현이 쉽습니다.

전략의 장점

- 원리가 명확하고 구현이 용이하여 초보자에게 적합합니다.

- 이동평균선을 활용해 주요 추세를 판단하므로 추세 추종에 효과적입니다.

- ATR 기반 손절매를 통해 개별 급등락으로 인한 손실을 효과적으로 제어할 수 있습니다.

- 파라미터를 쉽게 조정하여 다양한 시장 환경에 적응할 수 있습니다.

전략의 위험

- 횡보장에서는 이동평균선이 많은 가짜 신호를 생성하여 추세 반전 지점을 놓칠 가능성이 있습니다.

- ATR 지표는 급변하는 시장에 충분히 민감하게 반응하지 못해 예상보다 큰 손실을 초래할 수 있습니다.

- 지표 파라미터와 ATR 승수 설정은 경험에 의존하므로 부적절한 설정은 전략 성과에 악영향을 미칠 수 있습니다.

- 이중 이동평균선 자체의 지연성이 커서 전환점을 놓칠 수 있습니다.

위험 통제 방법:

- 이동평균선 기간을 적절히 단축하여 지표의 민감도를 높입니다.

- ATR 승수를 동적으로 조정하여 손절매를 더욱 유연하게 만듭니다.

- 다른 지표를 결합하여 가짜 신호를 걸러냅니다.

- 큰 규모의 구조적 관점에서 판단한 후에 거래를 실행합니다.

전략 최적화 방향

- 지수 이동평균선(EMA) 등 다른 유형의 이동평균선을 시도하여 더 나은 필터링 효과를 얻습니다.

- ATR 대신 켈트너 채널(Keltner Channel)과 같은 동적 손절매 방식을 고려합니다.

- 거래량 등 보조 지표를 추가하여 신호를 필터링합니다.

- 엘리엇 파동 이론, 지지 및 저항 수준 등을 결합하여 추세의 핵심 지점을 파악합니다.

요약

본 전략은 전형적인 추세 추종 전략으로, 이동평균선을 이용해 추세 방향을 판단하고 ATR로 손절매를 설정하여 위험을 제어합니다. 원리가 간단명료하여 이해하기 쉽습니다. 그러나 일정한 지연성과 가짜 신호의 위험이 존재하므로, 파라미터 조정, 지표 최적화, 추가 요소 결합 등을 통해 개선하여 변화무쌍한 시장 환경에 더 잘 적응할 수 있습니다. 전반적으로 초보자가 실습하고 최적화하기에 적합하지만, 실전에서는 신중하게 접근해야 합니다.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1