이중 이동 평균선 교차 기반의 되돌림 진입 전략

개요

EintSimple Pullback Strategy는 이중 이동평균선 교차를 기반으로 한 되돌림 진입 전략입니다. 이 전략은 먼저 장기 및 단기 두 개의 이동평균선을 사용하여, 단기 이동평균선이 장기 이동평균선을 아래에서 위로 돌파할 때 매수 신호를 생성합니다. 잘못된 돌파를 걸러내기 위해, 이 전략은 종가가 장기 이동평균선보다 높을 것을 요구합니다.

진입 후, 가격이 다시 단기 이동평균선을 하향 돌파하면 청산 신호가 발생합니다. 또한, 이 전략은 이탈 손절을 설정하여 최고점에서의 하락폭이 설정된 손절 비율에 도달하면 포지션을 청산합니다.

전략 로직

이 전략은 주로 이중 이동평균선의 골든 크로스를 기반으로 진입 시점을 판단합니다. 구체적으로, 롱 포지션을 열기 위해 다음 조건이 모두 충족되어야 합니다:

- 종가가 장기 이동평균선 ma1보다 큼

- 종가가 단기 이동평균선 ma2보다 작음

- 현재 보유 포지션이 없음

위 조건이 충족되면, 이 전략은 전액 매수합니다.

청산 신호는 두 가지 조건을 기반으로 합니다: 하나는 가격이 다시 단기 이동평균선을 하향 돌파하는 것이고, 다른 하나는 최고점에서의 하락폭이 설정된 손절 비율에 도달하는 것입니다. 구체적인 청산 조건은 다음과 같습니다:

- 종가가 단기 이동평균선 ma2보다 큼

- 최고점에서의 하락폭이 설정된 손절 비율에 도달함

위 조건 중 하나라도 충족되면, 이 전략은 모든 롱 포지션을 청산합니다.

장점

-

이중 이동평균선 교차와 실체 종가 판단을 결합하여 잘못된 돌파를 효과적으로 걸러낼 수 있습니다.

-

되돌림 진입을 사용하여 주가가 단기 저점을 형성한 후에 진입할 수 있습니다.

-

손절 설정이 있어 최대 하락폭을 제한할 수 있습니다.

위험

-

이중 이동평균선 교차 전략은 많은 거래 신호를 생성할 수 있어 추격 매수/매도 리스크가 있습니다.

-

이동평균선 파라미터 설정이 부적절하면 곡선이 너무 매끄럽거나 너무 민감해질 수 있습니다.

-

손절 설정이 너무 느슨하면 손실이 확대됩니다.

최적화 방향

-

다양한 길이의 장단기 이동평균선 파라미터 조합을 테스트하여 최적의 파라미터를 찾습니다.

-

종가와 대표 가격을 사용한 이동평균선 교차 판단 효과를 비교 테스트합니다.

-

거래량이나 변동성 지표 등의 필터를 추가하여 테스트합니다.

-

손절폭에 대한 백테스트 최적화를 통해 최적의 설정을 찾습니다.

결론

EintSimple Pullback Strategy는 간단하고 실용적인 이중 이동평균선 되돌림 전략입니다. 이 전략은 이동평균선의 지시 기능을 효과적으로 활용하면서 실체 종가 판단을 결합하여 잘못된 신호를 걸러냅니다. 이 전략은 잦은 거래와 추격 매수/매도 문제가 발생할 수 있지만, 파라미터 최적화와 필터 추가를 통해 더욱 개선할 수 있습니다. 전반적으로, 이 전략은 퀀트 트레이딩 초보자가 연습하고 최적화하기에 매우 적합한 전략입니다.

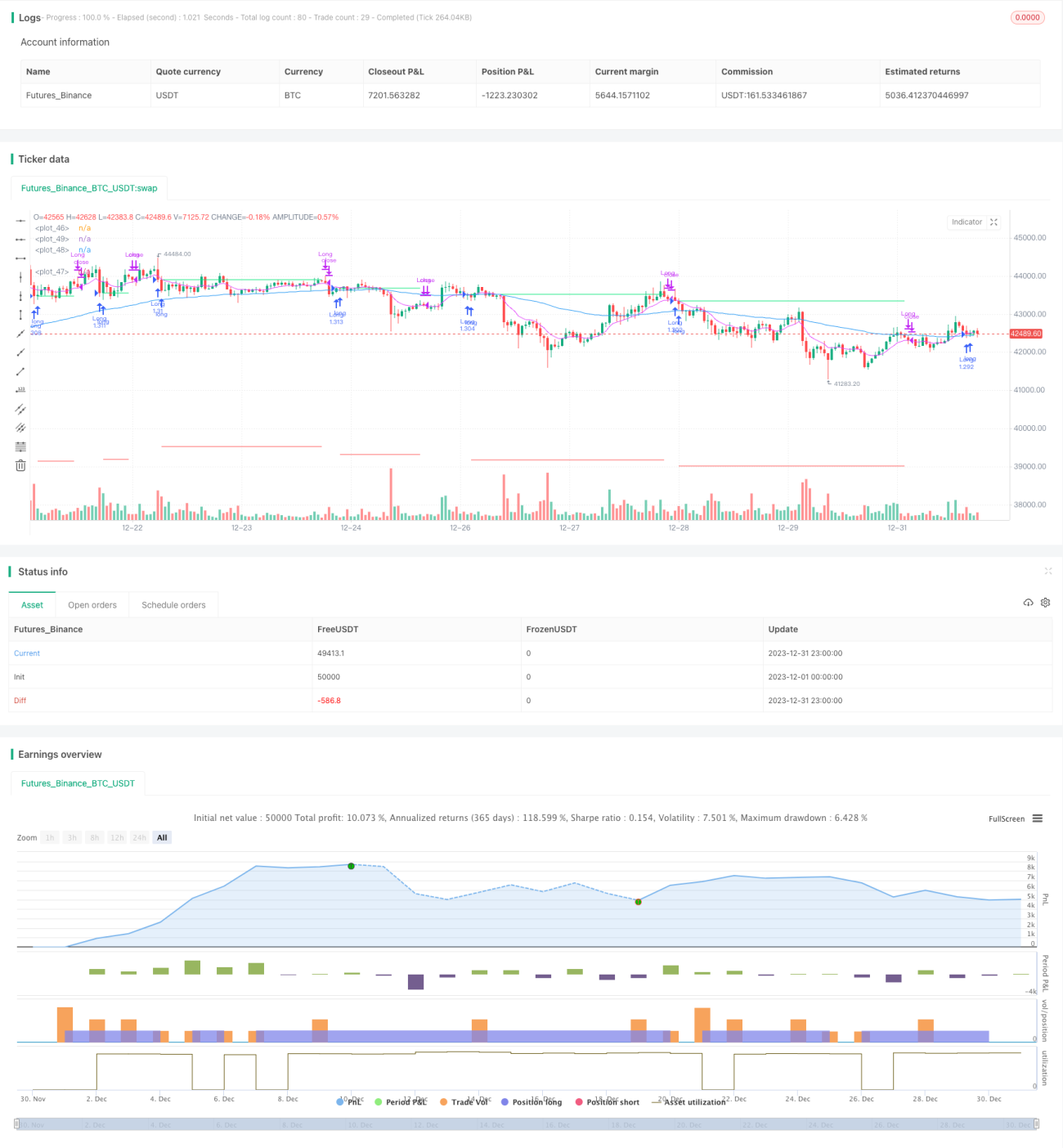

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © ZenAndTheArtOfTrading / www.PineScriptMastery.com

// @version=5

strategy("Simple Pullback Strategy", - 1