절대 모멘텀 지표 전략

개요

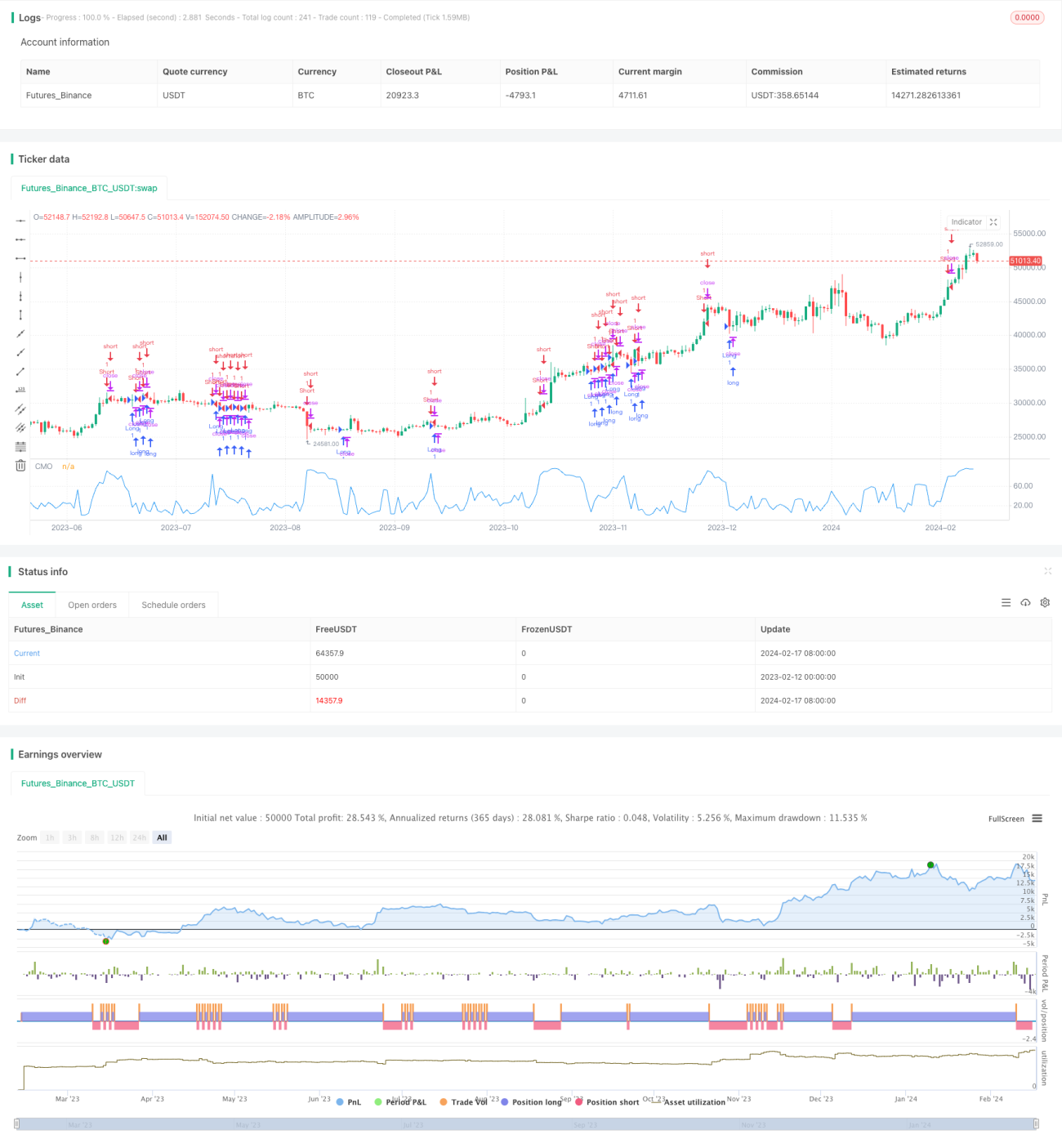

모멘텀 절대값 지표 전략은 Tushar Chande가 개발한 모멘텀 지표 CMO의 개선 버전입니다. 이 전략은 가격의 절대 모멘텀 값을 계산하여 현재 시장이 과매수 또는 과매도 상태인지 판단하고, 중기 가격 변동을 포착합니다.

전략 원리

이 전략의 핵심 지표는 개선된 CMO 지표인 AbsCMO입니다. AbsCMO 계산 공식은 다음과 같습니다:

AbsCMO = abs(100 * (最新收盘价 - Length周期前的收盘价) / (Length周期内价格波动绝对值的简单移动平均 * Length))

여기서 Length는 평균 기간 길이를 나타냅니다. AbsCMO 값 범위는 0부터 100입니다. 이 지표는 모멘텀 방향성과 강도 monumentality를 결합하여 중기 추세와 과매수/과매도 영역을 명확히 판단할 수 있습니다.

AbsCMO가 지정된 상단선(기본값 70)을 상향 돌파하면 시장이 과매수에 진입했음을 의미하며 공매도합니다. AbsCMO가 지정된 하단선(기본값 20)을 하향 돌파하면 시장이 과매도에 진입했음을 의미하며 매수합니다.

장점 분석

다른 모멘텀 지표와 비교하여 AbsCMO 지표는 다음과 같은 장점이 있습니다:

- 가격의 절대 모멘텀을 반영하여 중기 추세 판단이 더 정확합니다;

- 방향성과 강도를 결합하여 과매수/과매도 식별이 더 명확합니다;

- 범위가 0-100으로 제한되어 다양한 종목 간 비교에 더 적합합니다;

- 단기 급격한 변동에 민감하지 않으며 중기 시장 추세를 반영합니다;

- 매개변수를 사용자 정의할 수 있어 적응성이 높습니다.

리스크 분석

이 전략에는 주로 다음과 같은 리스크가 있습니다:

- 중기 지표로 단기 변동에 충분히 민감하게 반응하지 않습니다;

- 기본 매개변수가 모든 종목에 적합하지 않을 수 있으므로 최적화가 필요합니다;

- 장기 보유는 큰 하락을 초래할 수 있습니다.

보유 기간을 적절히 단축하고, 매개변수를 최적화하거나, 다른 지표와 조합하여 사용함으로써 리스크를 줄일 수 있습니다.

최적화 방향

이 전략은 다음과 같은 측면에서 최적화할 수 있습니다:

- AbsCMO의 매개변수를 최적화하여 더 많은 종목에 적응;

- 다른 지표와 결합하여 가짜 신호를 필터링;

- 손절 및 익절 규칙을 수립하여 리스크 관리;

- 딥러닝 등의 기술을 결합하여 더 나은 진입점 탐색.

요약

모멘텀 절대값 지표 전략은 전반적으로 비교적 실용적인 중기 거래 전략입니다. 가격의 중기 절대 모멘텀 특성을 반영하여 시장 중기 추세를 판단하는 능력이 우수합니다. 그러나 이 전략은 단기 급격한 변동에 민감하지 않아 일정한 리스크가 존재합니다. 매개변수 최적화, 지표 필터링, 손절 메커니즘 등을 통해 더욱 개선하면 실전 성과가 더욱 안정적이고 신뢰할 수 있게 됩니다.

/*backtest

start: 2023-02-12 00:00:00

end: 2024-02-18 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 17/02/2017

// This indicator plots the absolute value of CMO. CMO was developed by Tushar - 1