Strategi Penapisan Analisis Pembetulan Indeks

Gambaran Keseluruhan

Strategi ini menggunakan gabungan operasi modulo dan purata bergerak eksponen (EMA) untuk mewujudkan penapis arah aliran yang rawak dan kukuh bagi menentukan arah pegangan kedudukan. Strategi terlebih dahulu mengira sama ada baki apabila harga dibahagi dengan nombor yang ditetapkan adalah sifar. Jika ya, isyarat perdagangan akan muncul. Isyarat ini jika berada di bawah purata bergerak eksponen akan menjana isyarat jual; jika di atas purata bergerak eksponen akan menjana isyarat beli. Strategi ini menggabungkan sifat rawak operasi matematik dengan penentuan arah aliran teknikal, menggunakan pengesahan silang antara penunjuk kitaran yang berbeza, untuk menapis sebahagian pergerakan harga rawak yang mengganggu.

Prinsip Strategi

- Tetapkan nilai input harga a sebagai harga penutup close (boleh diubah); tetapkan nilai pembahagi b sebagai 4 (boleh diubah).

- Kira baki modulo apabila a dibahagi dengan b, tentukan sama ada baki adalah sifar.

- Tetapkan panjang purata bergerak eksponen MALen, secara lalai 70 kitaran, sebagai penunjuk arah aliran jangka sederhana hingga panjang harga.

- Apabila baki modulo adalah sifar, isyarat perdagangan evennumber dijana, dan hubungannya dengan EMA menentukan arah. Apabila harga menembusi ke atas garis EMA, isyarat beli BUY dijana; apabila harga menembusi ke bawah garis EMA, isyarat jual SELL dijana.

- Entri perdagangan akan memasuki kedudukan beli atau jual mengikut arah isyarat. Strategi boleh menghadkan pembukaan kedudukan bertentangan untuk mengawal bilangan dagangan.

- Syarat henti rugi ditetapkan berdasarkan tiga cara: henti rugi tetap, henti rugi ATR, henti rugi julat pergerakan harga. Syarat ambil untung adalah sebaliknya daripada henti rugi.

- Pilihan untuk menggunakan henti rugi bergerak untuk mengunci lebih banyak keuntungan, secara lalai tidak digunakan.

Analisis Kelebihan

- Sifat rawak operasi modulo mengelakkan kesan turun naik harga, digabungkan dengan penentuan arah aliran purata bergerak, boleh menapis isyarat tidak sah dengan berkesan.

- Purata bergerak eksponen sebagai penunjuk arah aliran jangka sederhana hingga panjang, digabungkan dengan isyarat jangka pendek daripada operasi modulo, mencapai pengesahan berlapis untuk mengelakkan isyarat palsu.

- Tetapan parameter yang boleh disesuaikan adalah sangat fleksibel, membolehkan pelarasan mengikut pasaran yang berbeza untuk mencari kombinasi parameter optimum.

- Mengintegrasikan pelbagai cara henti rugi untuk mengawal risiko. Pada masa yang sama, syarat ambil untung ditetapkan untuk mengunci keuntungan.

- Menyokong pembukaan kedudukan bertentangan secara langsung, membolehkan peralihan arah kedudukan tanpa celah. Juga boleh mematikan fungsi ini untuk mengurangkan bilangan dagangan.

Analisis Risiko

- Tetapan parameter yang tidak sesuai boleh menyebabkan terlalu banyak isyarat perdagangan, meningkatkan kekerapan dagangan dan kos gelinciran.

- Purata bergerak eksponen sebagai satu-satunya penunjuk arah aliran mungkin menyebabkan ketinggalan, terlepas masa pembalikan harga.

- Cara henti rugi tetap mungkin terlalu mekanikal, tidak dapat menyesuaikan diri dengan turun naik pasaran.

- Pembukaan kedudukan bertentangan secara langsung akan meningkatkan kekerapan pelarasan kedudukan, meningkatkan kos dagangan dan risiko.

Arah Pengoptimuman

- Boleh menguji penunjuk purata bergerak lain sebagai ganti EMA, atau menggabungkan EMA dengan purata bergerak lain, untuk melihat sama ada kadar keuntungan dapat ditingkatkan.

- Boleh mencuba menggabungkan penapis operasi modulo dengan strategi lain seperti Bollinger Bands, corak candlestick, dsb., untuk membentuk penapis yang lebih stabil.

- Boleh mengkaji cara henti rugi adaptif yang menyesuaikan jarak henti rugi berdasarkan tahap turun naik pasaran.

- Boleh menetapkan bilangan dagangan atau ambang untung/rugi untuk menghadkan kekerapan pembukaan kedudukan bertentangan.

Kesimpulan

Strategi ini menggabungkan penapisan rawak melalui operasi modulo dengan penentuan arah aliran purata bergerak secara berkesan. Tetapan parameter adalah fleksibel, membolehkan pelarasan dan pengoptimuman mengikut persekitaran pasaran yang berbeza, untuk mendapatkan isyarat perdagangan yang lebih boleh dipercayai. Pada masa yang sama, ia mengintegrasikan pelbagai mekanisme henti rugi untuk mengawal risiko, serta ambil untung dan henti rugi bergerak untuk mengunci keuntungan. Strategi ini mempunyai idea keseluruhan yang jelas, mudah difahami dan diubah suai, dan berpotensi besar untuk aplikasi dagangan sebenar selepas ujian dan pengoptimuman lanjut.

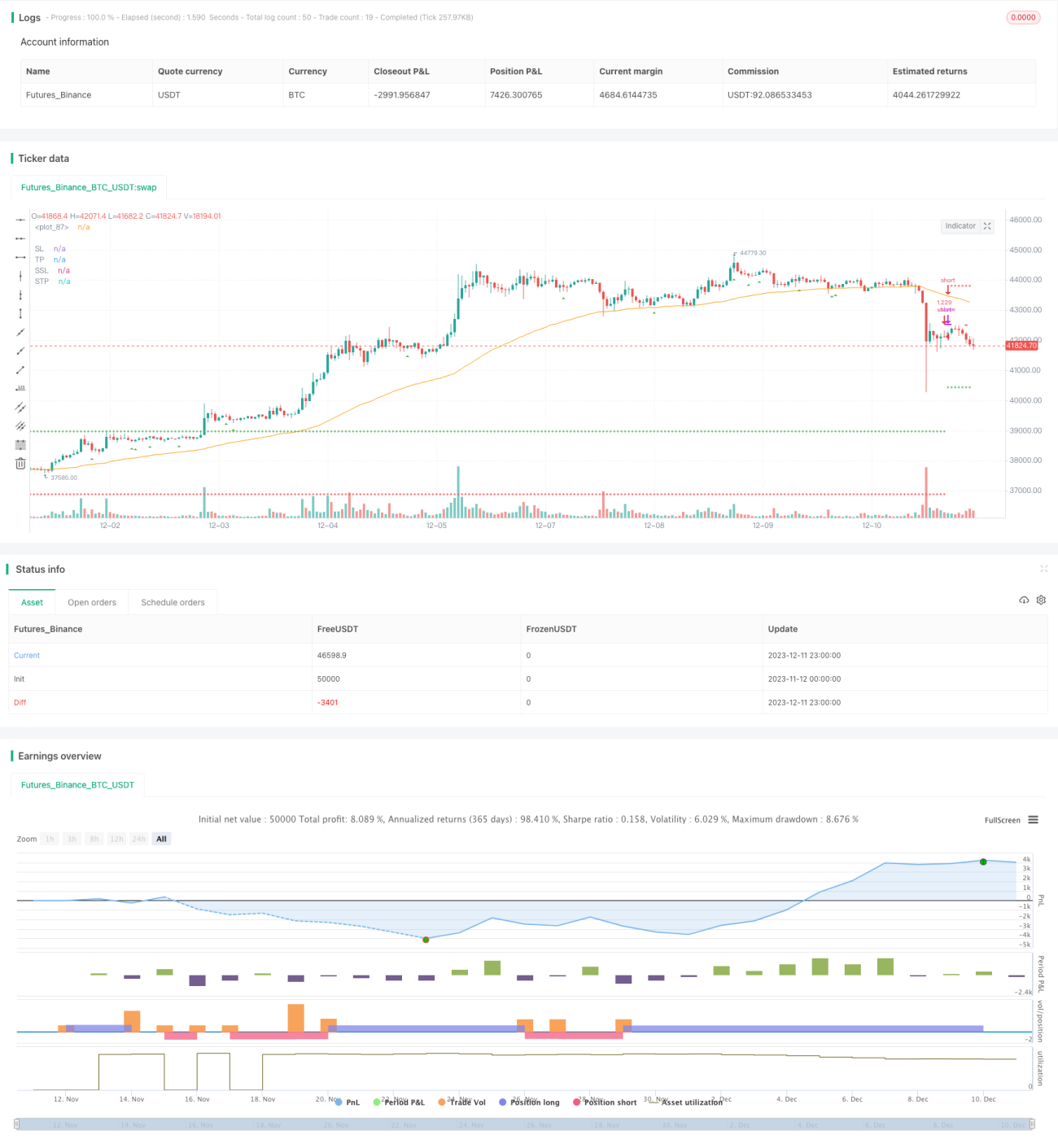

/*backtest

start: 2023-11-12 00:00:00

end: 2023-12-12 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tweakerID

// To understand this strategy first we need to look into the Modulo (%) operator. The modulo returns the remainder numerator - 1