Strategi Pembalikan Trend Ideologi Dinamik

Gambaran Keseluruhan

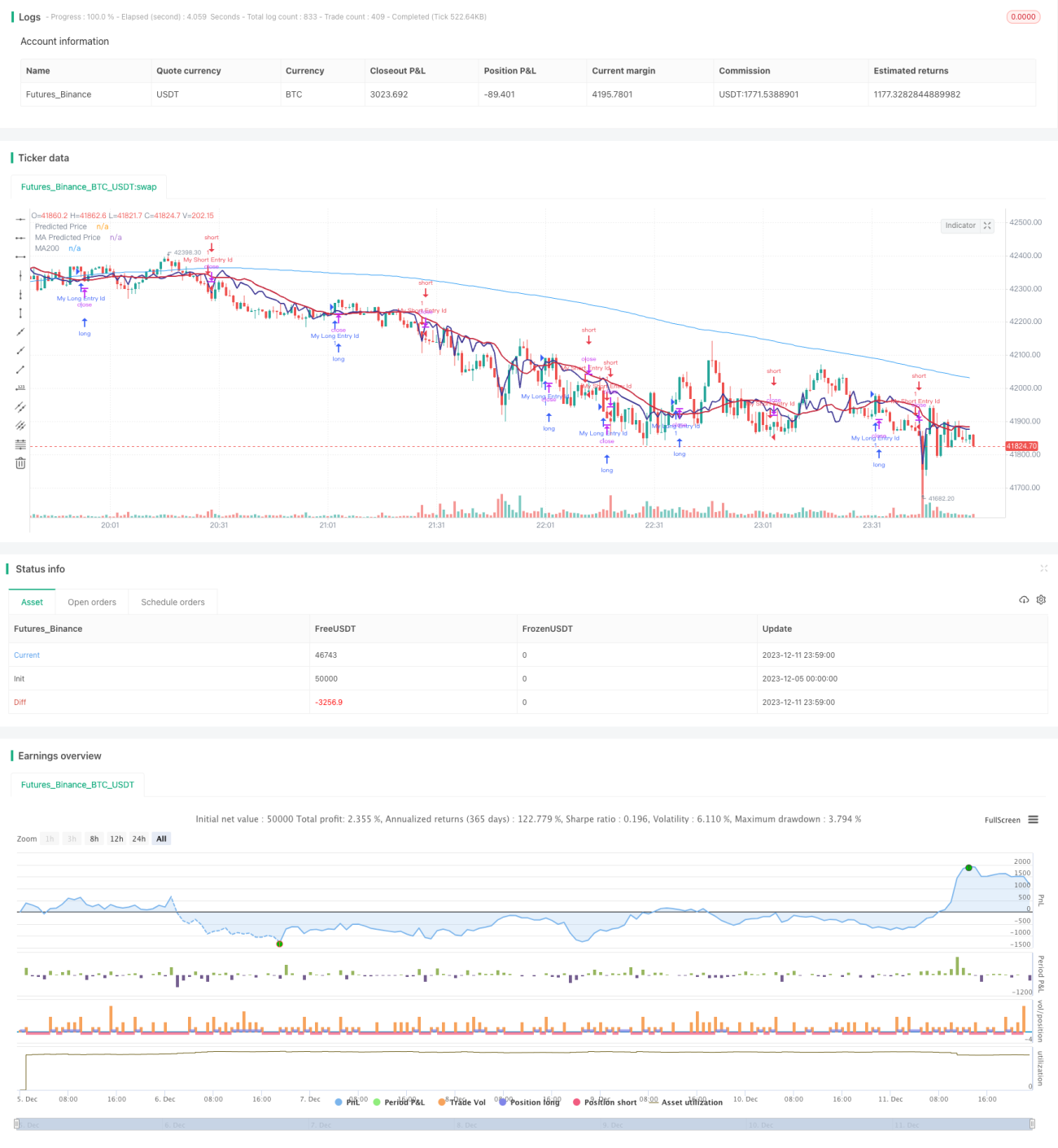

Strategi pembalikan arah aliran ideologi dinamik menggunakan regresi linear untuk meramalkan harga, dan menggabungkan ideologi yang dibentuk oleh purata bergerak untuk menjana isyarat dagangan. Apabila harga ramalan melintasi purata bergerak dari bawah ke atas, isyarat beli dijana; apabila harga ramalan melintasi purata bergerak dari atas ke bawah, isyarat jual dijana, untuk menangkap pembalikan arah aliran.

Prinsip Strategi

- Kira regresi linear harga saham berdasarkan volum dagangan untuk mendapatkan nilai ramalan harga.

- Kira purata bergerak di bawah keadaan diferentes.

- Apabila harga ramalan melintasi purata bergerak dari bawah ke atas, isyarat beli dihasilkan.

- Apabila harga ramalan melintasi purata bergerak dari atas ke bawah, isyarat jual dihasilkan.

- Gabungkan penunjuk MACD untuk menentukan masa pembalikan arah aliran.

Isyarat di atas digabungkan dengan pelbagai confirmation untuk mengelakkan penembusan palsu, dengan itu meningkatkan ketepatan isyarat.

Analisis Kelebihan

- Menggunakan regresi linear untuk meramalkan arah aliran harga, meningkatkan ketepatan isyarat.

- Menggabungkan purata bergerak untuk membentuk ideologi, menangkap pembalikan arah aliran.

- Mengira regresi linear berdasarkan volum dagangan, lebih bermakna dari segi ekonomi.

- Menggabungkan penunjuk seperti MACD untuk pelbagai confirmation, mengurangkan isyarat palsu.

Analisis Risiko

- Tetapan parameter regresi linear akan memberi kesan besar kepada keputusan.

- Tetapan purata bergerak juga akan mempengaruhi kualiti isyarat.

- Walaupun terdapat mekanisme confirmation, masih terdapat risiko isyarat palsu.

- Kod boleh dioptimumkan lagi untuk mengurangkan bilangan dagangan dan meningkatkan kadar keuntungan.

Arah Pengoptimuman

- Optimumkan parameter regresi linear dan purata bergerak.

- Tambah syarat confirmation untuk mengurangkan kadar isyarat palsu.

- Gabungkan lebih banyak faktor untuk menilai kualiti pembalikan arah aliran.

- Optimumkan strategi stop loss untuk mengurangkan risiko setiap dagangan.

Kesimpulan

Strategi pembalikan arah aliran ideologi dinamik mengintegrasikan ramalan regresi linear dan ideologi yang dibentuk oleh purata bergerak untuk menangkap masa pembalikan arah aliran. Berbanding dengan penunjuk tunggal, ia mempunyai kebolehpercayaan yang lebih tinggi. Pada masa yang sama, strategi boleh dipertingkatkan lagi dari segi kualiti isyarat dan tahap keuntungan melalui pelarasan parameter dan pengoptimuman syarat confirmation.

/*backtest

start: 2023-12-05 00:00:00

end: 2023-12-12 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © stocktechbot

//@version=5

strategy("Linear Cross", overlay=true, margin_long=100, margin_short=0)- 1