Strategi Perdagangan Kuantitatif Hibrid Dua Indikator

Gambaran Keseluruhan

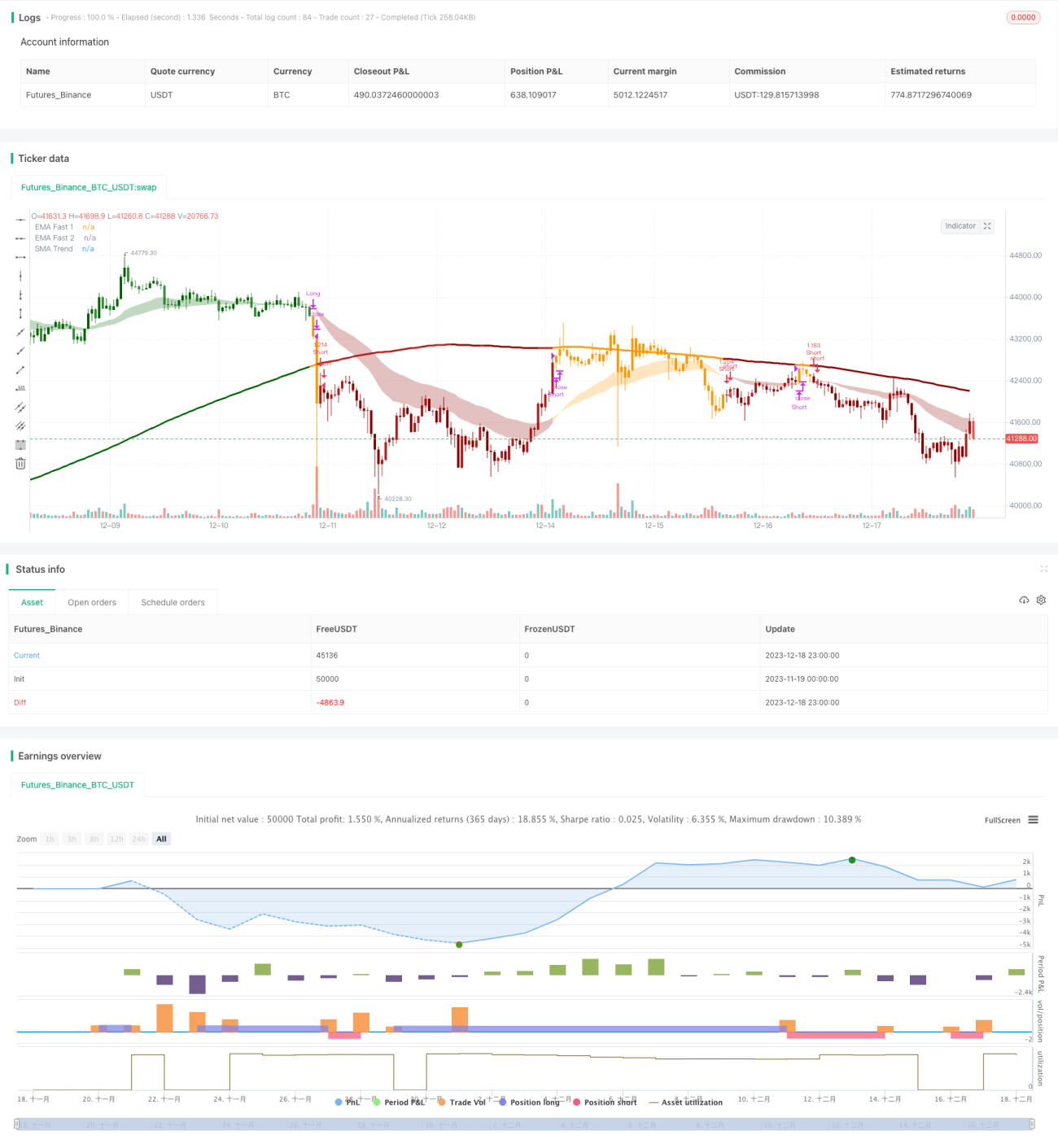

Strategi ini mengenal pasti arah trend dan membuat dagangan dengan menggabungkan dua set indikator. Pertama, ia menggunakan persilangan dua purata bergerak (garis pantas dan garis sederhana) untuk menilai trend jangka pendek; kedua, ia menggunakan julat saluran dan purata bergerak jangka panjang untuk menentukan arah trend utama. Isyarat dagangan hanya dijana apabila kedua-dua penilaian adalah konsisten. Penggunaan pelbagai indikator secara hibrid ini dapat menapis isyarat palsu dengan berkesan dan meningkatkan kestabilan.

Prinsip Strategi

Strategi ini menggunakan tiga kumpulan indikator untuk membuat pertimbangan. Pertama, persilangan emas dan persilangan mati antara EMA garis pantas (26 kitaran) dan EMA garis sederhana (50 kitaran) digunakan untuk menilai trend jangka pendek. Kedua, julat saluran dikira untuk menentukan sama ada harga menembusi julat tersebut bagi menilai arah pasaran jangka sederhana (bullish atau bearish). Akhir sekali, SMA garis panjang (200 kitaran) dikira dan dibandingkan dengan harga untuk menentukan arah trend utama. Isyarat dagangan hanya dijana apabila ketiga-tiga penilaian adalah konsisten sepenuhnya.

Secara spesifik, logik penilaian adalah seperti berikut:

-

Persilangan garis pantas dan garis sederhana (persilangan emas menunjukkan kenaikan, persilangan mati menunjukkan penurunan) digunakan untuk menentukan arah trend jangka pendek.

-

Sama ada harga menembusi julat saluran digunakan untuk menentukan arah trend jangka sederhana. Julat saluran adalah berdasarkan purata bergerak jangka panjang ditambah atau ditolak ATR yang didarab dengan satu pekali. Jika harga menembusi had atas, ia adalah kenaikan; jika harga menembusi had bawah, ia adalah penurunan.

-

Perbandingan antara harga dan purata bergerak jangka panjang digunakan untuk menentukan arah trend utama.

Akhirnya, isyarat dagangan hanya dijana apabila ketiga-tiga penilaian (jangka pendek, sederhana, dan panjang) adalah konsisten sepenuhnya. Penilaian hibrid ini dapat menapis isyarat palsu dengan berkesan dan meningkatkan kestabilan.

Kelebihan Strategi

Strategi hibrid dua set indikator ini mempunyai beberapa kelebihan:

-

Penapisan isyarat palsu yang berkesan dan peningkatan kestabilan. Isyarat dagangan memerlukan pengesahan daripada pelbagai indikator (jangka pendek, sederhana, panjang), sekali gus mengelakkan isyarat salah yang disebabkan oleh satu indikator sahaja.

-

Fleksibiliti tinggi, parameter indikator boleh dilaraskan mengikut pasaran. Parameter purata bergerak pantas dan perlahan serta julat saluran boleh diubah suai untuk menyesuaikan diri dengan persekitaran pasaran yang berbeza.

-

Gabungan perdagangan trend dan perdagangan julat. Indikator jangka sederhana dan pendek menangkap trend, manakala indikator jangka panjang menentukan julat. Secara keseluruhan, ia menggabungkan kelebihan strategi trend dan strategi pembalikan.

-

Kecekapan penggunaan modal yang tinggi. Pesanan hanya dibuat apabila pelbagai indikator konsisten, membolehkan penggunaan modal yang cekap dan mengelakkan dagangan yang tidak perlu.

Risiko Strategi

Strategi ini juga mempunyai beberapa risiko:

-

Risiko penetapan parameter. Kitaran purata bergerak dan parameter julat saluran perlu ditetapkan dengan betul. Jika tidak sesuai, ia mungkin gagal mengesan trend dengan berkesan atau menyebabkan terlalu banyak isyarat palsu.

-

Dua set indikator meningkatkan kos peluang dagangan. Berbanding dengan strategi satu indikator, ia mungkin terlepas sebahagian peluang dagangan dan tidak dapat masuk atau keluar pada titik terbaik.

-

Strategi henti rugi perlu berhati-hati. Mekanisme henti rugi penembusan dalam strategi ini boleh menyebabkan kerugian yang tidak perlu; peratusan henti rugi perlu ditetapkan dengan teliti.

-

Keberkesanan mungkin berkurangan dalam pasaran yang sangat berombak. Strategi ini lebih sesuai untuk persekitaran pasaran yang mempunyai trend yang jelas.

Hala Tuju Pengoptimuman Strategi

Strategi ini boleh dioptimumkan dari beberapa aspek berikut:

-

Menguji kombinasi parameter yang berbeza untuk mencari parameter optimum. Ujian dengan lebih banyak data sejarah boleh membantu mencari tetapan parameter yang terbaik.

-

Menambah mekanisme henti rugi adaptif. Boleh menggabungkan indikator turun naik (Volatility Indicator) untuk melaraskan magnitud henti rugi secara dinamik.

-

Menambah indikator volum sebagai bantuan penilaian. Membantu menentukan saiz posisi pada titik penting untuk meningkatkan kecekapan penggunaan modal.

-

Mengoptimumkan logik masuk. Pertimbangkan strategi kos purata dengan masuk secara berperingkat untuk mengurangkan risiko bagi setiap kemasukan.

-

Menggabungkan model pembelajaran mesin untuk penilaian. Memperkenalkan model seperti rangkaian neural untuk menilai keteguhan model dan kebaikan kesesuaian (goodness of fit).

Rumusan

Strategi ini menggunakan penilaian tiga peringkat (pantas, sederhana, panjang) dan mekanisme pengesahan berganda, yang dapat menekan isyarat palsu dengan berkesan dan meningkatkan kestabilan. Pada masa yang sama, ia menggabungkan kelebihan perdagangan trend dan perdagangan julat, serta mempunyai kecekapan penggunaan modal yang tinggi. Ia boleh diperbaiki melalui pengoptimuman parameter, pengoptimuman henti rugi, dan penggabungan indikator volum, menjadikannya strategi kuantitatif hibrid yang disyorkan.

- 1