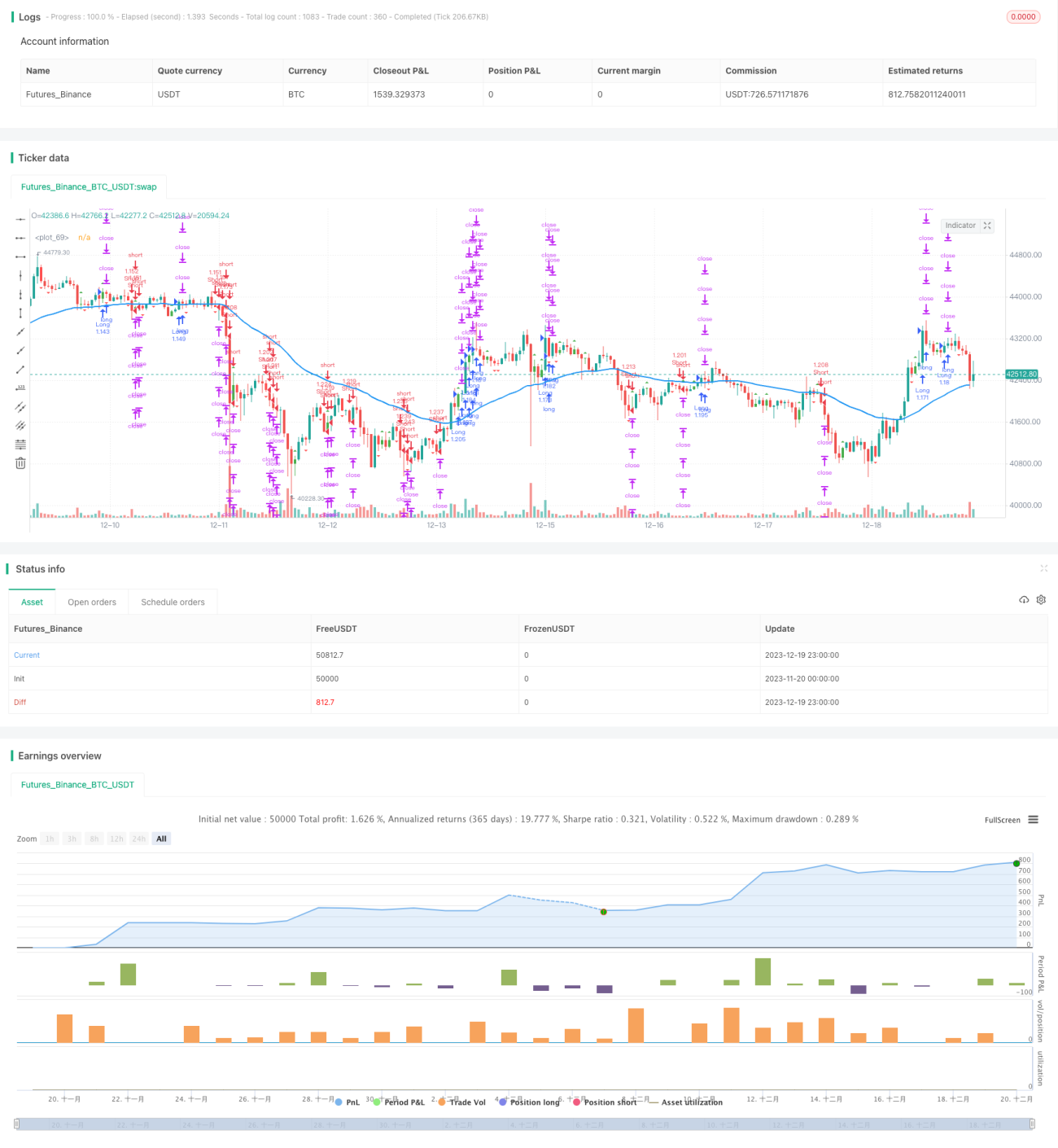

Strategi perdagangan kuantitatif automatik berdasarkan bar dalaman dan purata bergerak

Ringkasan

Strategi ini berdasarkan pada gabungan corak bar dalaman (inside bar) dan penunjuk purata bergerak (moving average) untuk melaksanakan dagangan automatik. Apabila corak bar dalaman muncul, ia menunjukkan kemungkinan perubahan arah aliran semasa. Pada ketika itu, kedudukan purata bergerak digunakan untuk menentukan arah dagangan akhir.

Prinsip Strategi

-

Mencari corak bar dalaman. Corak bar dalaman berlaku apabila harga tertinggi dan terendah suatu lilin berada dalam lingkungan badan lilin sebelumnya. Berdasarkan warna badan lilin, kita boleh menentukan sama ada bar dalaman itu adalah bar dalaman menaik (bullish inside bar) atau bar dalaman menurun (bearish inside bar).

-

Menentukan kedudukan purata bergerak. Apabila corak bar dalaman dikesan, jika harga berada di atas purata bergerak, ia adalah isyarat menaik; jika harga berada di bawah purata bergerak, ia adalah isyarat menurun.

-

Menggabungkan corak bar dalaman dan isyarat menaik/menurun daripada purata bergerak untuk mendapatkan arah dagangan akhir. Iaitu, bar dalaman menurun yang menembusi ke bawah purata bergerak akan menjana isyarat jual (short), manakala bar dalaman menaik yang menembusi ke atas purata bergerak akan menjana isyarat beli (long).

Kelebihan Strategi

-

Menggabungkan penunjuk teknikal dan corak harga untuk meningkatkan ketepatan keputusan dagangan.

-

Corak bar dalaman itu sendiri mengandungi isyarat perubahan arah yang kuat, membolehkan pengesanan titik perubahan arah aliran lebih awal.

-

Purata bergerak menapis sebahagian hingar, mengelakkan terperangkap dalam julat pasaran yang berayun (sideways market).

-

Melaksanakan dagangan automatik sepenuhnya, mengurangkan masa dan kos tenaga kerja dagangan manual dengan ketara.

Risiko Strategi dan Penyelesaian

-

Apabila harga berayun di sekitar purata bergerak, banyak isyarat palsu mungkin timbul, menyebabkan dagangan berlebihan. Ini boleh dikurangkan dengan mengoptimumkan parameter purata bergerak atau menambah syarat penapisan tambahan.

-

Strategi ini lebih sesuai untuk pasaran yang mempunyai arah aliran yang jelas. Dalam pasaran yang tidak menentu (sideways atau choppy), prestasinya mungkin kurang memberangsangkan. Penunjuk penentu arah aliran seperti ADX boleh digunakan untuk mengawal pengaktifan algoritma.

-

Terdapat sedikit ketinggalan masa. Parameter boleh dipendekkan atau kaedah pengiraan purata bergerak dioptimumkan untuk mengurangkan ketinggalan.

-

Risiko pengeluaran (drawdown) agak tinggi. Henti rugi (stop loss) boleh dipasang untuk mengawal risiko kerugian, dan pengurusan kedudukan yang sesuai juga dapat membantu mengurangkan pengeluaran.

Hala Tuju Pengoptimuman Strategi

-

Mengoptimumkan tempoh pengesanan bar dalaman untuk mencari kombinasi parameter terbaik.

-

Mencuba pelbagai jenis purata bergerak seperti EMA, SMA, dsb., untuk menentukan penunjuk purata bergerak yang paling sesuai.

-

Menambah penunjuk tambahan seperti MACD, KDJ, dsb., untuk memperkayakan asas penentuan menaik/menurun dan meningkatkan ketepatan isyarat.

-

Memasukkan penapis seperti ADX, ATR untuk mengawal persekitaran pengaktifan algoritma, mengelakkan ia berjalan dalam pasaran yang tidak sesuai.

-

Mengoptimumkan strategi pengurusan kedudukan, seperti kawalan saiz kedudukan berdasarkan risiko, pengurusan kedudukan untuk mengejar keuntungan yang terlepas, dsb., bagi mengawal risiko dan mengejar pulangan yang lebih tinggi.

Kesimpulan

Strategi ini menggabungkan isyarat bar dalaman yang dijejaki secara dinamik dengan penunjuk purata bergerak untuk menghasilkan satu pelan dagangan kuantitatif automatik sepenuhnya. Penjanaan isyarat strategi adalah ringkas dan jelas, mudah difahami dan diikuti. Ia menunjukkan prestasi yang baik dalam pasaran yang mempunyai arah aliran yang jelas. Dengan mengoptimumkan parameter dan peraturan selanjutnya, kestabilan dan keuntungan strategi boleh dipertingkatkan lagi.

- 1