Strategi Indikator Mo Fei yang Merentasi Masa

Gambaran Keseluruhan

Ini adalah strategi kuantitatif mudah yang menggunakan penunjuk Mofei (Mo Fei) untuk mengenal pasti "jerung besar" dalam pasaran. Ia sesuai untuk jangka masa 5 minit dan terutamanya digunakan untuk perdagangan mata wang kripto.

Prinsip Strategi

Strategi ini menggunakan penunjuk Mofei dengan panjang 3, menetapkan garis terlebih beli pada 100 dan garis terlebih jual pada 0. Strategi menunggu penunjuk Mofei mencapai tahap terlebih beli, menunjukkan kehadiran "jerung besar" dalam pasaran. Jika pada hari yang sama dua titik terlebih beli pertama penunjuk Mofei berlaku dan harga masih dapat mengekalkan kenaikan, ini adalah isyarat masuk beli.

Apabila penunjuk Mofei = 100 dan lilin seterusnya adalah lilin hijau besar, masuk posisi beli. Henti rugi ditetapkan pada titik terendah hari dagangan tersebut, dan ambil untung dalam 60 minit selepas masuk.

Untuk posisi jual, logik cermin boleh digunakan. Iaitu apabila penunjuk Mofei mencapai terlebih jual dan lilin seterusnya adalah lilin merah besar, masuk posisi jual.

Kelebihan Strategi

-

Menggunakan penunjuk Mofei dapat mengenal pasti tingkah laku "jerung besar" dalam mengumpul saham berpotensi, yang mungkin terus meningkat.

-

Menggunakan badan lilin sebenar untuk mengenal pasti titik penembusan yang kuat dapat menapis banyak penembusan palsu.

-

Menggabungkan penapis SMA untuk mengelakkan membeli saham yang berada dalam aliran menurun, dapat mengurangkan risiko perdagangan dengan berkesan.

-

Menggunakan kaedah operasi ultra-pendek intraday, ambil untung dalam 60 minit dapat mengunci keuntungan dengan cepat dan mengurangkan kebarangkalian pengeluaran.

Risiko Strategi

-

Penunjuk Mofei mungkin menghasilkan isyarat palsu yang menyebabkan kerugian yang tidak perlu. Parameter boleh diselaraskan atau penunjuk lain ditambah untuk menapis.

-

Kaedah operasi ultra-pendek 60 minit mungkin terlalu agresif dan tidak sesuai untuk saham dengan turun naik tinggi. Masa ambil untung boleh diselaraskan atau henti rugi bergerak digunakan untuk pengoptimuman.

-

Tidak mengambil kira risiko impak pasaran akibat peristiwa makroekonomi besar. Strategi harus dihentikan sementara dan diteruskan selepas pasaran stabil.

Arah Pengoptimuman Strategi

-

Boleh menguji kombinasi parameter yang berbeza, seperti melaraskan panjang penunjuk Mofei, mengoptimumkan parameter tempoh SMA, dll.

-

Cuba tambah penunjuk lain seperti Bollinger Bands, penunjuk KD, untuk melihat sama ada ketepatan isyarat dapat ditingkatkan.

-

Uji melonggarkan tahap henti rugi untuk melihat sama ada keuntungan tunggal yang lebih besar dapat diperoleh.

-

Cuba bangunkan versi strategi yang sesuai untuk jangka masa lain, seperti 15 minit atau 30 minit, berdasarkan rangka kerja strategi ini.

Kesimpulan

Strategi ini secara keseluruhannya sangat ringkas dan mudah difahami, idea asasnya konsisten dengan kaedah klasik mengikuti "jerung besar". Dengan mengenal pasti titik penting terlebih beli dan terlebih jual penunjuk Mofei, digabungkan dengan penapisan badan lilin sebenar, banyak bunyi dapat ditapis. Penambahan penapis SMA juga meningkatkan kestabilan strategi.

Kaedah operasi ultra-pendek 60 minit dapat memperoleh keuntungan dengan cepat, tetapi juga membawa risiko operasi yang lebih tinggi. Secara keseluruhan, ini adalah templat strategi kuantitatif yang sangat bernilai praktikal, layak untuk penyelidikan dan pengoptimuman yang mendalam, serta memberikan kita pemikiran pembangunan strategi yang berharga.

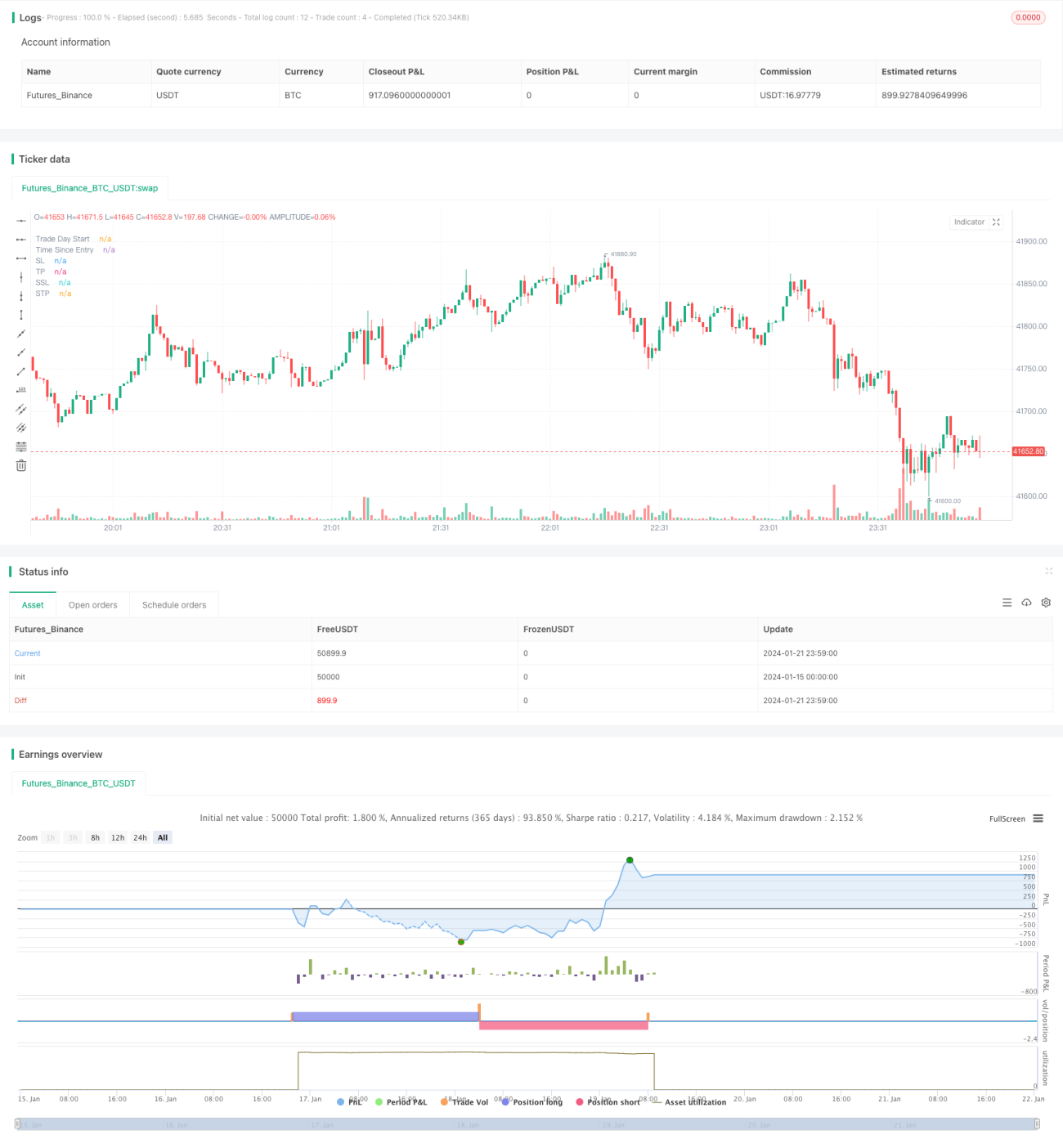

/*backtest

start: 2024-01-15 00:00:00

end: 2024-01-22 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// From "Crypto Day Trading Strategy" PDF file.

- 1