Strategi Mengikuti Trend Saluran Harga Dua Purata Bergerak

Gambaran Keseluruhan

Strategi ini adalah strategi penjejakan arah aliran yang membina saluran harga berdasarkan dua EMA, menggunakan julat saluran untuk menilai arah harga dan menetapkan henti rugi pengesanan untuk mengunci keuntungan.

Prinsip Strategi

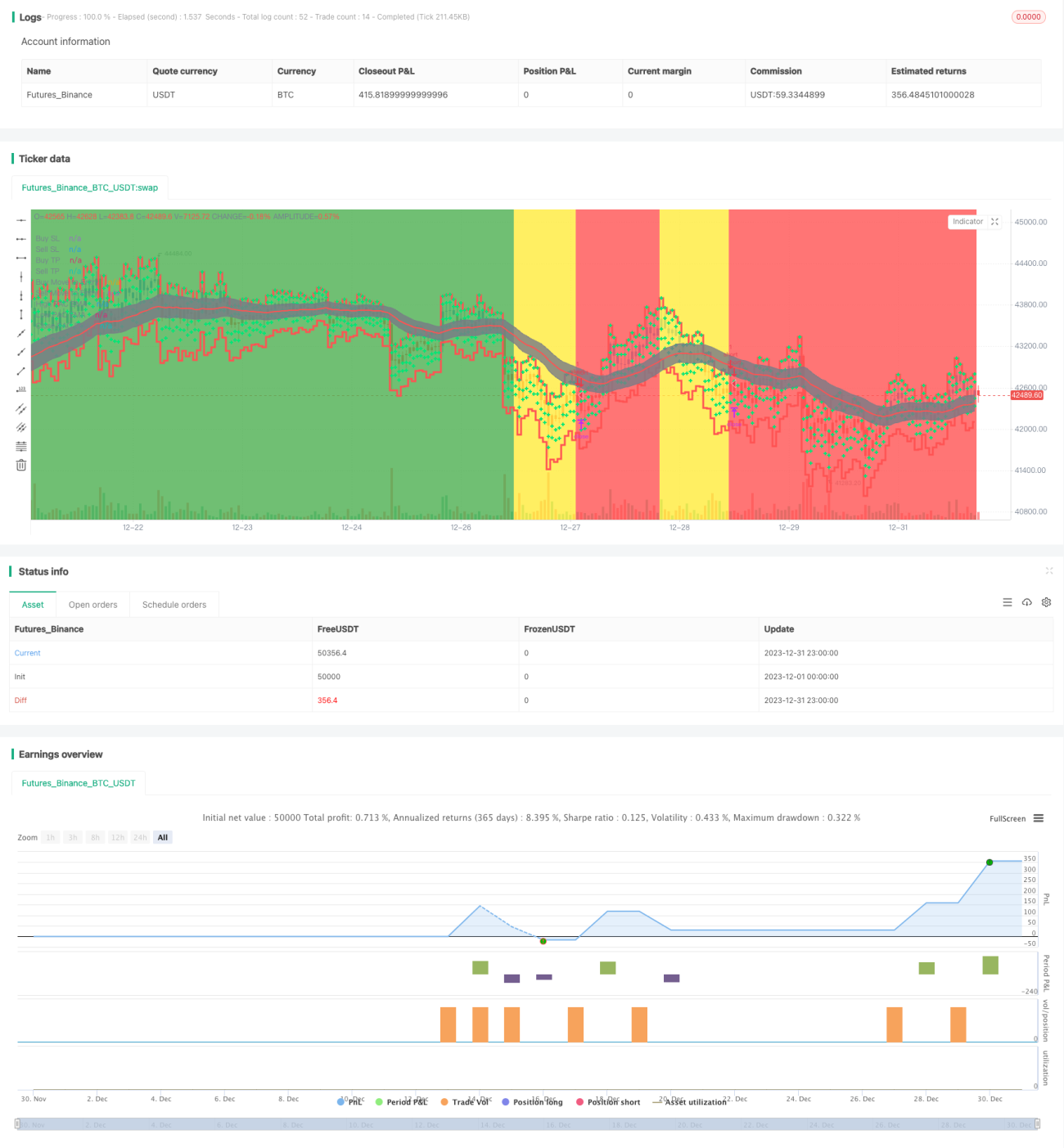

Strategi saluran harga dua EMA menggunakan EMA pantas dan EMA perlahan untuk membina saluran harga. Parameter EMA pantas ialah 89 kitaran, dan EMA perlahan ialah 200 kitaran. Pada masa yang sama, tiga purata bergerak berdasarkan harga tinggi, rendah dan tutup digunakan untuk membina julat saluran harga. Garis atas dan garis bawah saluran masing-masing adalah EMA tinggi dan EMA rendah 34 kitaran.

Apabila EMA pantas berada di atas EMA perlahan dan harga berada di bawah garis bawah, ia dianggap sebagai arah aliran menaik; apabila EMA pantas berada di bawah EMA perlahan dan harga berada di atas garis atas, ia dianggap sebagai arah aliran menurun.

Dalam arah aliran menaik, strategi akan menjual pendek apabila pengesahan pembalikan arah aliran berlaku; dalam arah aliran menurun, strategi akan membeli panjang apabila pengesahan pembalikan arah aliran berlaku.

Selain itu, strategi ini dilengkapi dengan fungsi henti rugi pengesanan. Selepas memegang kedudukan, harga henti rugi pengesanan akan dikemas kini secara masa nyata untuk mengunci keuntungan.

Analisis Kelebihan

Kelebihan utama strategi ini ialah menggunakan dua EMA untuk membina saluran harga bagi menilai arah aliran, digabungkan dengan perdagangan pembalikan, bagi mengelakkan pembelian pada harga tinggi dan penjualan pada harga rendah. Ia juga dilengkapi dengan fungsi henti rugi bergerak untuk mengunci keuntungan dan mengurangkan risiko kerugian.

Kelebihan lain termasuk: ruang pengoptimuman parameter yang besar, boleh dilaraskan untuk instrumen dan kitaran yang berbeza; harga henti rugi dikemas kini masa nyata, risiko operasi rendah.

Analisis Risiko

Risiko utama strategi ini ialah keberkesanan isyarat pembalikan yang kurang baik, yang boleh menyebabkan salah taksir. Dalam kes ini, parameter perlu dioptimumkan untuk memastikan pengesahan pembalikan arah aliran yang tepat.

Selain itu, penentuan titik henti rugi juga sangat penting. Titik henti rugi yang terlalu besar mungkin menyebabkan ketidakcukupan dalam pelaksanaan henti rugi; titik henti rugi yang terlalu kecil mungkin menyebabkan henti rugi berlebihan. Ini perlu diselaraskan mengikut instrumen tertentu.

Akhir sekali, masalah data juga boleh menyebabkan strategi gagal. Pastikan menggunakan data sejarah yang boleh dipercayai, berterusan dan mencukupi untuk ujian balik dan pengesahan dagangan langsung.

Arah Pengoptimuman

Pengoptimuman strategi ini tertumpu pada beberapa aspek berikut:

-

Kitaran untuk EMA pantas dan EMA perlahan boleh dioptimumkan dengan menetapkan kombinasi parameter yang berbeza untuk menilai keberkesanan.

-

Parameter garis atas dan garis bawah saluran harga juga boleh dilaraskan untuk mencari kitaran yang lebih sesuai.

-

Penentuan titik henti rugi adalah penting; parameter yang berbeza boleh diuji untuk mengoptimumkan strategi henti rugi.

-

Boleh diuji sama ada penunjuk lain perlu diperkenalkan untuk menentukan pembalikan arah aliran bagi meningkatkan prestasi perdagangan.

Kesimpulan

Strategi ini mempunyai aliran operasi yang munasabah dan lancar secara keseluruhan, menggunakan saluran dua EMA untuk menilai arah aliran dan membuat perdagangan, serta dilengkapi dengan henti rugi bergerak untuk mengunci keuntungan. Ia merupakan strategi penjejakan arah aliran yang agak stabil. Melalui pengoptimuman parameter dan persediaan pengurusan risiko, strategi ini boleh menjadi salah satu strategi perdagangan kuantitatif yang cekap.

- 1