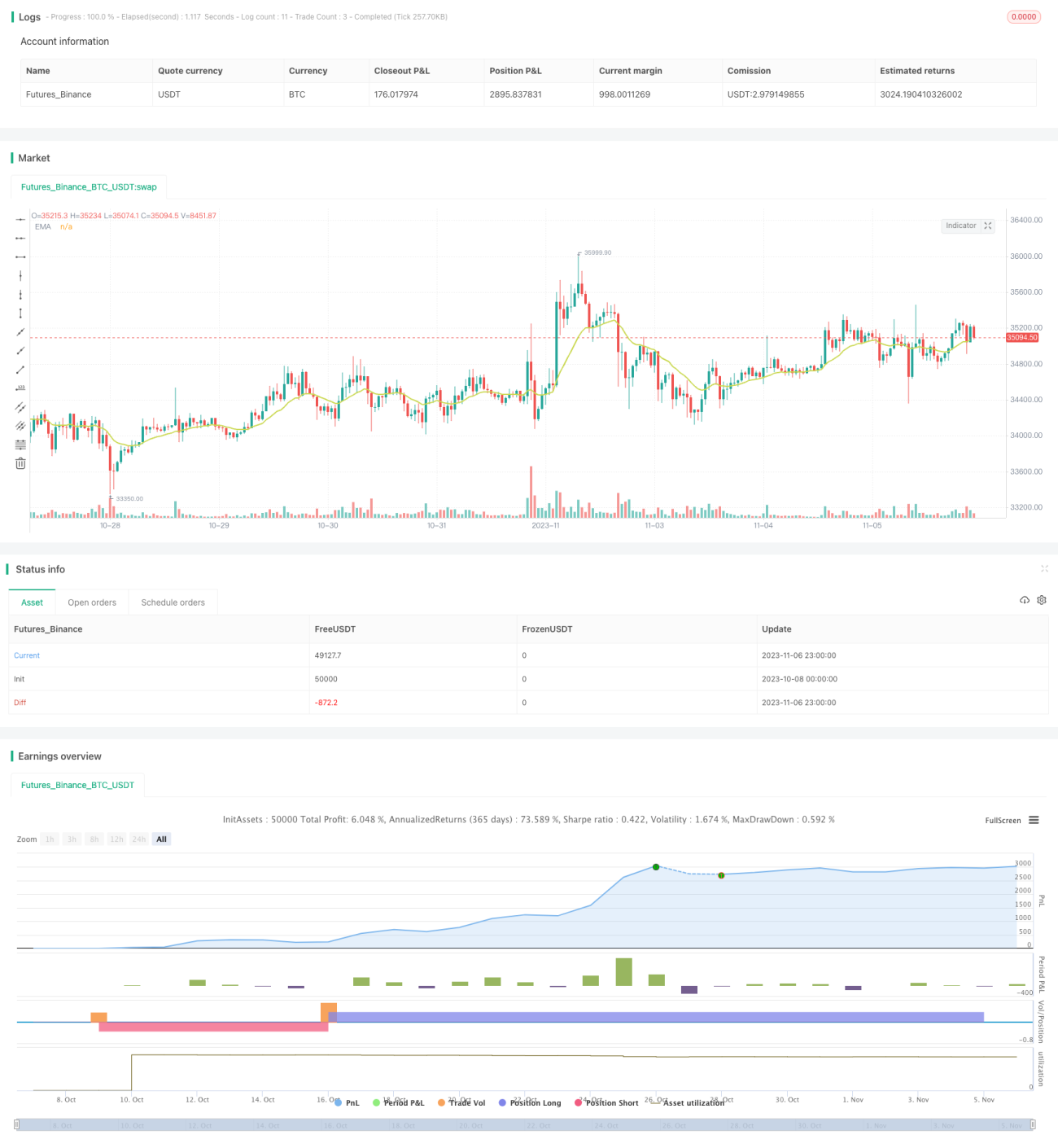

Estratégia de Rompimento Bidirecional do RSI

Visão Geral

Esta estratégia é baseada no indicador de Índice de Força Relativa (RSI), utilizando o princípio de sobrecompra e sobrevenda do RSI para realizar operações bidirecionais de rompimento. Quando o RSI cruza para cima da linha de sobrecompra definida, abre-se uma posição comprada; quando o RSI cruza para baixo da linha de sobrevenda definida, abre-se uma posição vendida. Trata-se de uma estratégia típica de reversão.

Princípio da Estratégia

-

Define os parâmetros para o cálculo do RSI conforme a entrada do usuário, incluindo o período do RSI, o limite de sobrecompra e o limite de sobrevenda.

-

Com base na posição da curva do RSI em relação às linhas de sobrecompra e sobrevenda, determina se está em zona de sobrecompra ou sobrevenda.

-

Quando o RSI sai da zona de sobrevenda e cruza a respectiva linha de limite, realiza-se uma operação de abertura na direção oposta. Por exemplo, ao sair da zona de sobrecompra cruzando a linha de sobrecompra, considera-se uma reversão, abrindo uma posição comprada; ao sair da zona de sobrevenda cruzando a linha de sobrevenda, considera-se uma reversão, abrindo uma posição vendida.

-

Após abrir a posição, são definidos níveis de stop loss e take profit. Acompanha-se a situação de stop loss e take profit, fechando a posição quando as condições forem atendidas.

-

A estratégia também oferece uma funcionalidade opcional de usar uma Média Móvel Exponencial (EMA) como filtro. Somente quando o sinal de compra ou venda do RSI for acompanhado pelo preço rompendo a EMA, a posição é aberta.

-

A estratégia também permite negociar apenas em horários específicos. O usuário pode definir um período de negociação; após esse horário, as posições são fechadas.

Análise de Vantagens

- Utiliza o clássico princípio de rompimento do RSI, com bons resultados em backtests.

- Permite ajustar flexivelmente os limites de sobrecompra e sobrevenda, adaptando-se a diferentes ativos.

- Oferece a opção de usar filtro EMA para evitar aberturas e fechamentos frequentes devido a oscilações de curto prazo.

- Suporta stop loss e take profit, aumentando a estabilidade da estratégia.

- Permite definir um horário específico de negociação, evitando períodos inadequados.

- Suporta operações bidirecionais (compra e venda), aproveitando as oscilações do mercado em ambas as direções.

Análise de Riscos

- O RSI pode apresentar divergências, e depender apenas dele pode gerar sinais imprecisos. É necessário combinar com tendências, médias móveis, etc.

- Limites de sobrecompra/sobrevenda mal ajustados podem levar a negociações excessivas ou perda de oportunidades.

- Stop loss e take profit mal configurados podem tornar a estratégia muito agressiva ou conservadora.

- O filtro EMA mal ajustado pode perder oportunidades de negociação ou filtrar sinais válidos.

Soluções para os riscos:

- Otimizar os parâmetros do RSI, ajustando-os para diferentes ativos.

- Combinar com indicadores de tendência para identificar divergências e evitar sinais falsos.

- Testar e otimizar os parâmetros de stop loss e take profit para encontrar os melhores valores.

- Testar e otimizar os parâmetros da EMA para encontrar o melhor nível de filtro.

Direções de Otimização da Estratégia

A estratégia pode ser otimizada nos seguintes aspectos:

-

Otimizar os parâmetros do RSI, buscando a melhor combinação para cada ativo. Pode-se realizar backtests exaustivos para encontrar os melhores limites de sobrecompra e sobrevenda.

-

Experimentar substituir ou combinar o RSI com outros indicadores para formar sinais mais fortes, como MACD, KD, Bandas de Bollinger, etc.

-

Otimizar a estratégia de stop loss e take profit para aumentar a estabilidade. Pode-se usar stop loss ajustável com base na volatilidade do mercado ou estratégias com trailing stop.

-

Otimizar o parâmetro do filtro EMA ou testar outros filtros de indicadores para evitar ficar preso em posições perdedoras.

-

Adicionar um módulo de identificação de tendência para evitar operar vendido em tendências de alta ou comprado em tendências de baixa.

-

Testar diferentes parâmetros de horário de negociação para determinar quais períodos são adequados para a estratégia e quais devem ser evitados.

Resumo

A estratégia de rompimento bidirecional baseada no RSI possui uma lógica clara, utilizando o clássico princípio de sobrecompra/sobrevenda para operações de reversão. Ela pode capturar oportunidades de reversão nas zonas de sobrecompra e sobrevenda, ao mesmo tempo que controla o risco por meio do filtro EMA e de stop loss/take profit. Com amplo espaço para otimização de parâmetros e módulos, pode ser transformada em uma estratégia de reversão mais estável e confiável. Vale a pena testar e otimizar ainda mais antes de aplicar na prática.

- 1