Estratégia de Filtro de Análise de Correção de Índice

Visão Geral

Esta estratégia utiliza uma combinação de operações de módulo e médias móveis exponenciais para criar um filtro de tendência com forte componente aleatória, que determina a direção da posição. A estratégia primeiro calcula se o resto da divisão do preço por um número definido é igual a 0; se for, um sinal de negociação é gerado. Se este sinal estiver abaixo da média móvel exponencial, a posição é vendida (short); se estiver acima, é comprada (long). A estratégia combina a aleatoriedade das operações matemáticas com a análise de tendência dos indicadores técnicos, utilizando a validação cruzada entre indicadores de diferentes períodos para filtrar eficazmente parte da aleatoriedade do mercado que impacta os preços.

Princípio da Estratégia

- Define-se o valor de entrada

acomo o preço de fechamento (close), que pode ser alterado; define-se o valor do divisorbcomo 4, que pode ser alterado. - Calcula-se o resto

moduloda divisão deaporbe verifica-se se o resto é igual a 0. - Define-se o comprimento da média móvel exponencial

MALen, com valor padrão de 70 períodos, como um indicador da tendência de médio/longo prazo do preço. - Quando o resto

moduloé igual a 0, um sinal de negociaçãoevennumberé gerado, e a sua relação com a EMA determina a direção. Quando o preço cruza acima da linha EMA, um sinal de COMPRA (BUY) é gerado; quando o preço cruza abaixo da linha EMA, um sinal de VENDA (SELL) é gerado. - As ordens de entrada (

entries) seguem a direção do sinal, abrindo posições compradas ou vendidas. A estratégia pode restringir a abertura de posições em direção oposta para controlar o número de negociações. - As condições de stop loss são definidas com base em três métodos: stop loss fixo, stop loss por ATR e stop loss por faixa de volatilidade do preço. As condições de take profit são o inverso do stop loss.

- Existe a opção de usar um stop loss móvel para travar mais lucros; o padrão é não utilizar.

Análise de Vantagens

- A aleatoriedade da operação de módulo evita ser influenciada pelas oscilações de preço. Combinada com a análise de tendência da média móvel, pode filtrar eficazmente sinais inválidos.

- A média móvel exponencial, como indicador de tendência de médio/longo prazo, é usada em conjunto com o sinal de curto prazo da operação de módulo, permitindo uma validação em múltiplas camadas e evitando sinais falsos.

- Os parâmetros personalizáveis são muito flexíveis, permitindo ajustes para diferentes mercados e a procura da melhor combinação de parâmetros.

- Integra vários métodos de stop loss para controlar o risco. Além disso, define condições de take profit para travar lucros.

- Suporta a abertura direta de posições em direção oposta, permitindo uma mudança perfeita na direção da posição. Esta funcionalidade também pode ser desativada para reduzir o número de negociações.

Análise de Riscos

- Uma configuração inadequada dos parâmetros pode gerar demasiados sinais de negociação, aumentando a frequência de negociações e os custos de slippage.

- A média móvel exponencial, como único indicador de análise de tendência, pode gerar atraso e perder o momento de reversão do preço.

- O método de stop loss fixo pode ser demasiado mecânico, não conseguindo ajustar-se às flutuações do mercado.

- A abertura direta de posições em direção oposta pode aumentar a frequência de ajuste de posição, elevando os custos de negociação e o risco.

Direções de Otimização

- Testar diferentes indicadores de média móvel para substituir a EMA, ou combinar a EMA com outras médias móveis, para verificar se a taxa de lucro pode ser melhorada.

- Tentar combinar o filtro da operação de módulo com outras estratégias, como Bandas de Bollinger, padrões de candlestick, etc., para formar um filtro mais estável.

- Pesquisar métodos de stop loss adaptativos que ajustem a distância do stop loss com base no nível de volatilidade do mercado.

- Definir um limite para o número de negociações ou um limiar de lucro/perda para restringir o número de vezes que se abre uma posição em direção oposta.

Resumo

Esta estratégia combina eficazmente a filtragem aleatória da operação de módulo com a análise de tendência da média móvel. Os seus parâmetros são flexíveis e podem ser ajustados e otimizados de acordo com diferentes ambientes de mercado para obter sinais de negociação mais fiáveis. Ao mesmo tempo, integra vários mecanismos de stop loss para controlar o risco, bem como take profit e stop loss móvel para travar lucros. A lógica geral da estratégia é clara, fácil de entender e modificar, merecendo mais testes e otimizações, com um grande potencial para aplicação prática em mercado real.

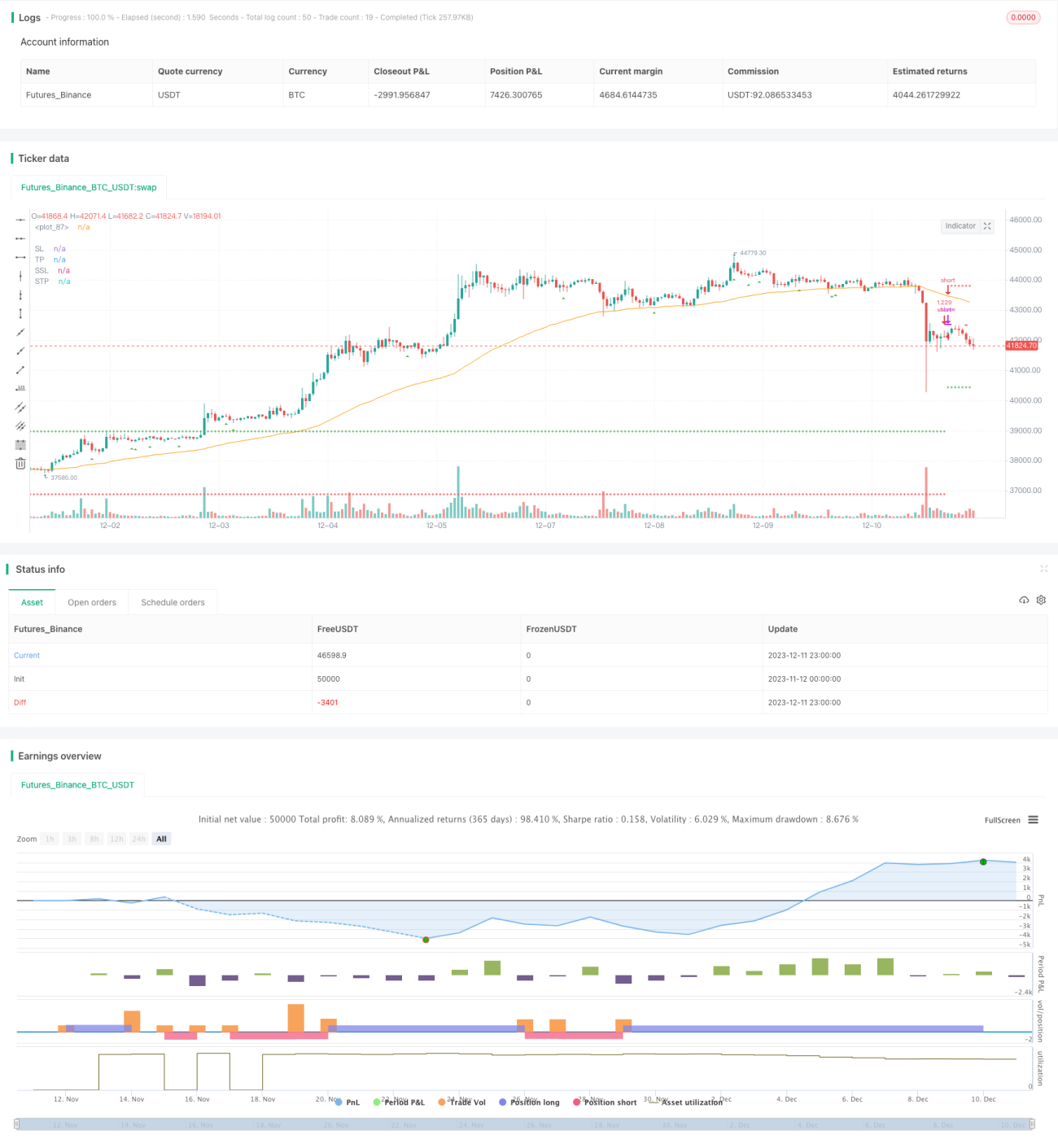

/*backtest

start: 2023-11-12 00:00:00

end: 2023-12-12 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tweakerID

// To understand this strategy first we need to look into the Modulo (%) operator. The modulo returns the remainder numerator - 1