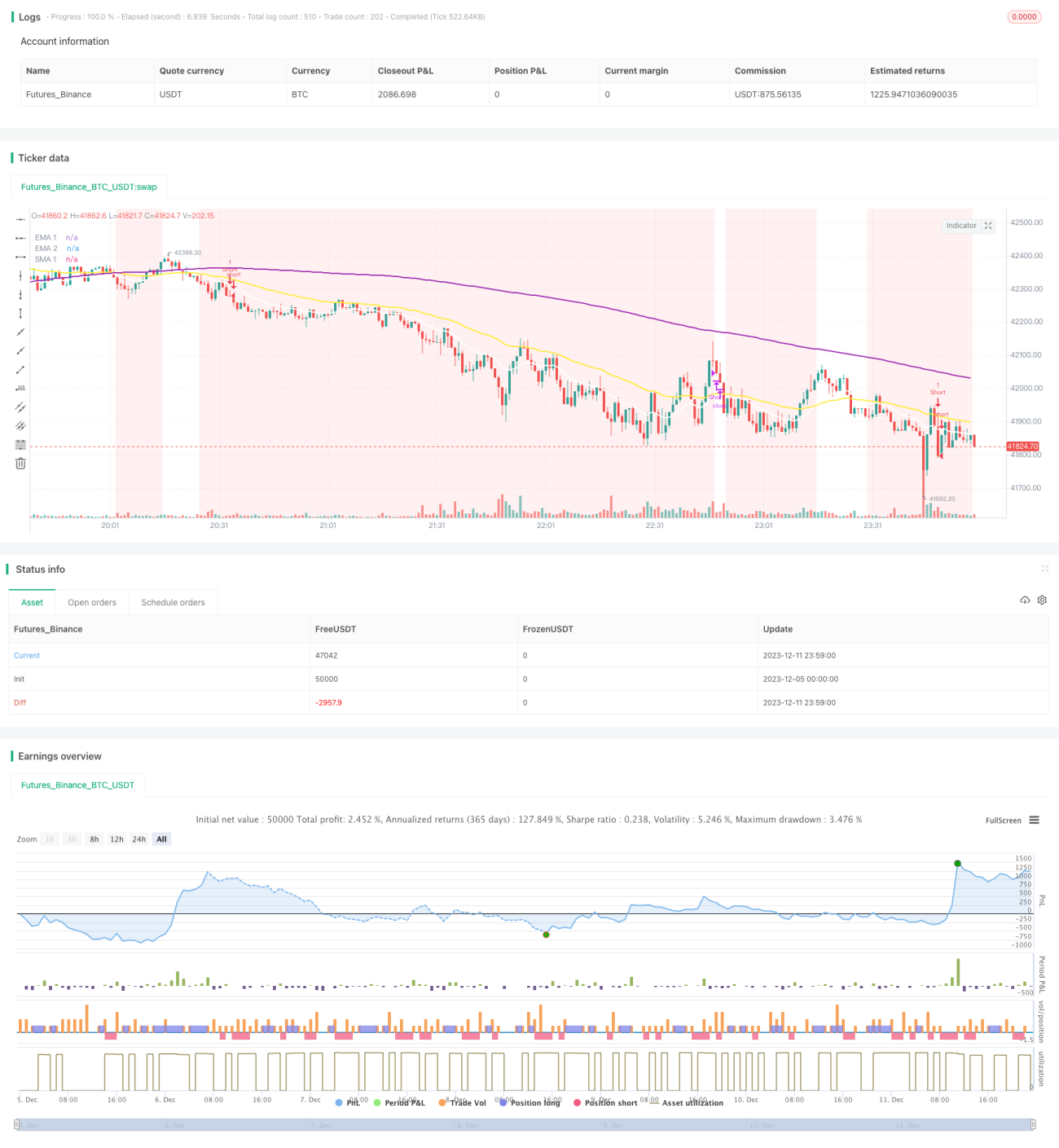

Estratégia de Rompimento de Momentum Composto

Visão Geral

Esta estratégia combina o uso de médias móveis, o indicador Laguerre RSI e o indicador ADX para realizar negociações de rompimento. Quando a média móvel rápida cruza acima da média móvel lenta, o Laguerre RSI está acima de 80 e o ADX está acima de 20, é feita uma posição comprada; quando a média móvel rápida cruza abaixo da média móvel lenta, o Laguerre RSI está abaixo de 20 e o ADX está acima de 20, é feita uma posição vendida. A estratégia captura o momentum do mercado, entrando no mercado no início do desenvolvimento da tendência.

Princípio

A estratégia utiliza principalmente os seguintes indicadores para determinar a tendência e o momento de entrada:

-

Combinação de médias móveis: EMA de 16 períodos, EMA de 48 períodos, SMA de 200 períodos. Quando a média de curto prazo cruza acima da média de longo prazo, o mercado é considerado de alta; quando cruza abaixo, é considerado de baixa.

-

O indicador Laguerre RSI identifica zonas de sobrecompra e sobrevenda. RSI acima de 80 é um sinal de alta; abaixo de 20 é um sinal de baixa.

-

O indicador ADX avalia o estado da tendência. ADX acima de 20 indica um estado de tendência, adequado para negociações de rompimento.

O sinal de entrada é dado pela combinação de médias móveis para determinar a direção da tendência, pelo Laguerre RSI para identificar o momento de entrada, e pelo ADX para filtrar mercados sem tendência. O sinal de saída é dado pela reversão das médias móveis. O quadro geral de julgamento da estratégia é razoável, com cada indicador cooperando para determinar alta/baixa e entrada/saída.

Vantagens

Esta estratégia apresenta as seguintes vantagens:

-

Captura do momentum da tendência: A estratégia só entra no mercado quando a tendência começa a se desenvolver, podendo capturar lucros exponenciais posteriores.

-

Perda limitada: O stop loss é definido adequadamente, permitindo controlar a perda de cada operação dentro de um determinado intervalo. Mesmo em caso de "armadilha", há oportunidades de lucro.

-

Julgamento preciso da combinação de indicadores: As médias móveis, o Laguerre RSI e o ADX conseguem avaliar com relativa precisão a direção do mercado e o momento de entrada.

-

Implementação simples: A estratégia utiliza apenas três indicadores, sendo de fácil implementação e compreensão.

Riscos

Esta estratégia também apresenta certos riscos:

-

Risco de reversão da tendência: A estratégia é do tipo seguidor de tendência. Se não identificar a reversão a tempo, pode gerar grandes perdas.

-

Risco de drawdown: Em mercados laterais, o stop loss pode ser violado, causando drawdown na conta.

-

Risco de otimização de parâmetros: Os parâmetros dos indicadores precisam ser ajustados conforme os diferentes mercados, caso contrário, podem perder eficácia.

Contramedidas:

-

Stop loss rigoroso para controlar a perda por operação.

-

Otimizar os parâmetros dos indicadores e ajustar os limiares de rompimento.

-

Utilizar métodos como hedge com futuros para gerenciar o drawdown.

Direções de Otimização

Esta estratégia pode ser otimizada nos seguintes aspectos:

-

Otimização dos melhores parâmetros: Testar os períodos das médias móveis, os parâmetros do Laguerre RSI e os parâmetros do ADX para encontrar a combinação ideal.

-

Otimização dos limiares de rompimento: Testar diferentes limiares de cruzamento das médias móveis para encontrar um equilíbrio entre o número de operações e a taxa de lucro.

-

Otimização das condições de entrada: Testar a combinação de outros indicadores com o Laguerre RSI para encontrar condições mais precisas de entrada.

-

Otimização das condições de saída: Pesquisar outros indicadores combinados com as médias móveis como sinais de saída mais precisos.

-

Otimização de meta de lucro e stop loss: Testar diferentes estratégias de take profit e stop loss para otimizar o retorno da conta.

Resumo

Esta estratégia, ao utilizar três indicadores – médias móveis, Laguerre RSI e ADX – consegue capturar eficazmente as tendências do mercado. Ela entra no mercado no início do desenvolvimento da tendência, acompanhando o movimento para capturar lucros exponenciais. Ao mesmo tempo, define estratégias de stop loss para controlar as perdas individuais. Esta estratégia é adequada para investidores ativos que têm capacidade de julgar o mercado, bem como para ser executada automaticamente via trading algorítmico após a otimização dos parâmetros. No geral, a estratégia possui forte aplicabilidade prática.

- 1