Estratégia de negociação quantitativa baseada nos indicadores TRSI e SuperTrend

Visão Geral

Esta estratégia combina o Índice de Força Relativa (TRSI) e o indicador Super Trend, formando um conjunto de estratégias de negociação quantitativa relativamente completo. A estratégia é usada principalmente para capturar tendências de médio e longo prazo, ao mesmo tempo que utiliza indicadores de curto prazo para filtrar sinais de negociação com ruído.

Princípio da Estratégia

- Calcular o indicador TRSI para avaliar se o mercado está em condição de sobrecompra ou sobrevenda, gerando sinais de compra e venda.

- Usar o indicador Super Trend para filtrar sinais de ruído e confirmar a tendência fundamental.

- Definir pontos de stop-loss e take-profit em diferentes estágios de lucro.

Especificamente, a estratégia primeiro calcula o indicador TRSI para determinar se o mercado apresenta área de sobrevenda, depois calcula o indicador Super Trend para determinar a direção da tendência principal. Combinando ambos, gera sinais de negociação. Em seguida, são definidos pontos de stop-loss e take-profit, com diferentes proporções de capital retiradas em diferentes estágios de lucro.

Análise de Vantagens

Esta estratégia possui as seguintes vantagens:

- Combinação de múltiplos indicadores, aumentando a precisão dos sinais. O TRSI determina o momento, o Super Trend filtra a direção.

- Adequada para negociação de tendências de médio e longo prazo. Sinais de sobrecompra/sobrevenda tendem a formar reversões de tendência.

- Definição razoável de stop-loss e take-profit, com diferentes estágios de lucro envolvendo diferentes proporções de retração, controlando efetivamente o risco.

Análise de Riscos

Esta estratégia também apresenta alguns riscos:

- Negociação de médio e longo prazo, incapaz de capturar oportunidades de curto prazo.

- Parâmetros do TRSI configurados inadequadamente podem perder a zona de sobrecompra/sobrevenda.

- Parâmetros do Super Trend configurados inadequadamente podem gerar sinais errados.

- Espaçamento de stop-loss excessivamente grande, incapaz de controlar o risco de forma eficaz.

Para esses riscos, podemos otimizar a partir dos seguintes aspectos:

Direções de Otimização

- Combinar mais indicadores de curto prazo para identificar mais oportunidades de negociação.

- Ajustar os parâmetros do TRSI para reduzir a margem de erro.

- Testar e otimizar os parâmetros do Super Trend.

- Definir stop-loss flutuante, acompanhando a linha de stop-loss em tempo real.

Resumo

Esta estratégia utiliza de forma abrangente múltiplos indicadores como TRSI e Super Trend, formando uma estratégia de negociação quantitativa relativamente completa. Pode identificar efetivamente tendências de médio e longo prazo, ao mesmo tempo que define stop-loss e take-profit para controlar riscos. A estratégia ainda tem grande espaço para otimização, podendo ser melhorada em aspectos como aumento da precisão dos sinais e identificação de mais oportunidades de negociação. No geral, é um bom ponto de partida para estratégias quantitativas.

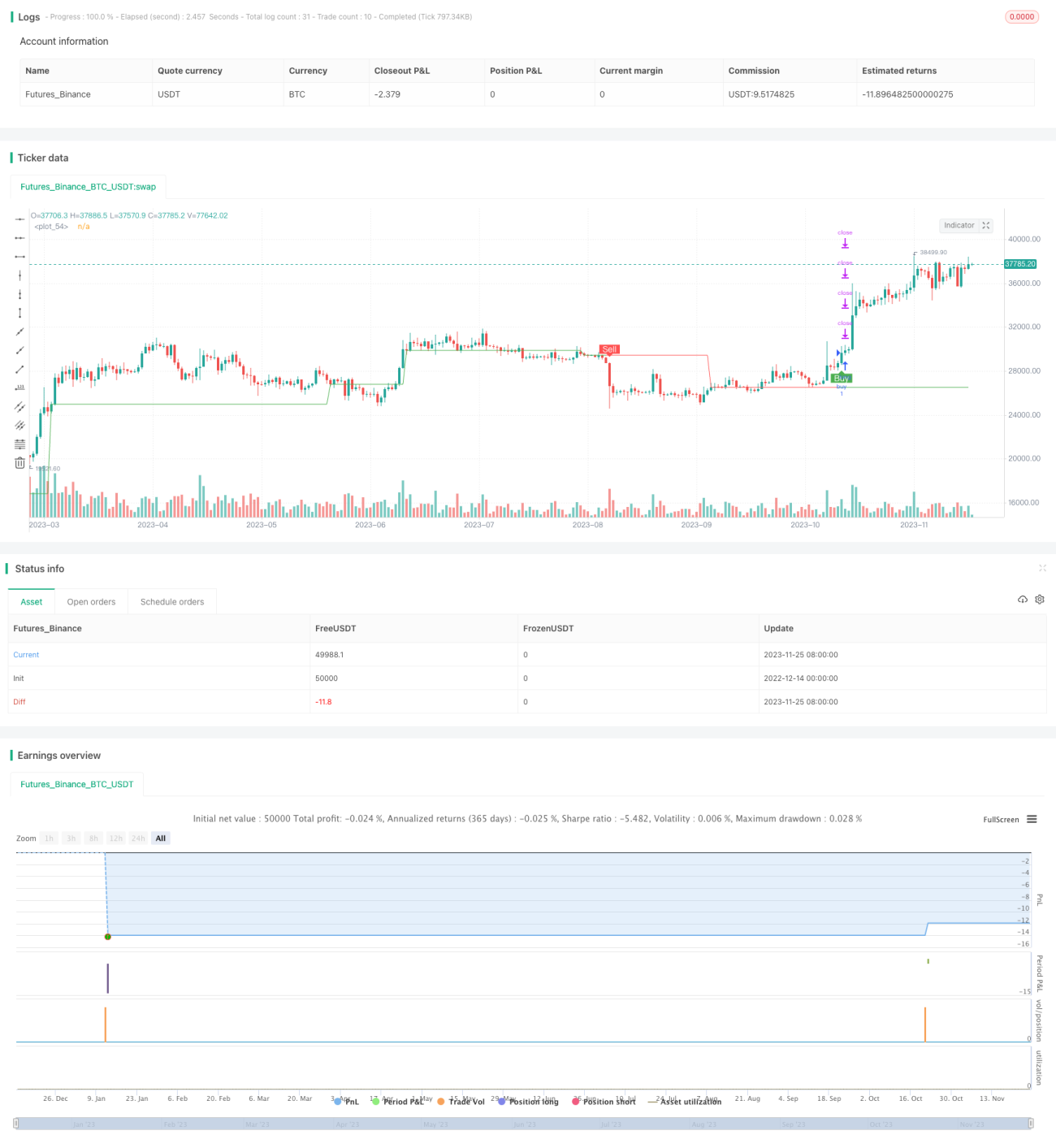

/*backtest

start: 2022-12-14 00:00:00

end: 2023-11-26 05:20:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title = "SuperTREX strategy", overlay = true)

strat_dir_input = input(title="Strategy Direction", defval="long", options=["long", "short", "all"])- 1