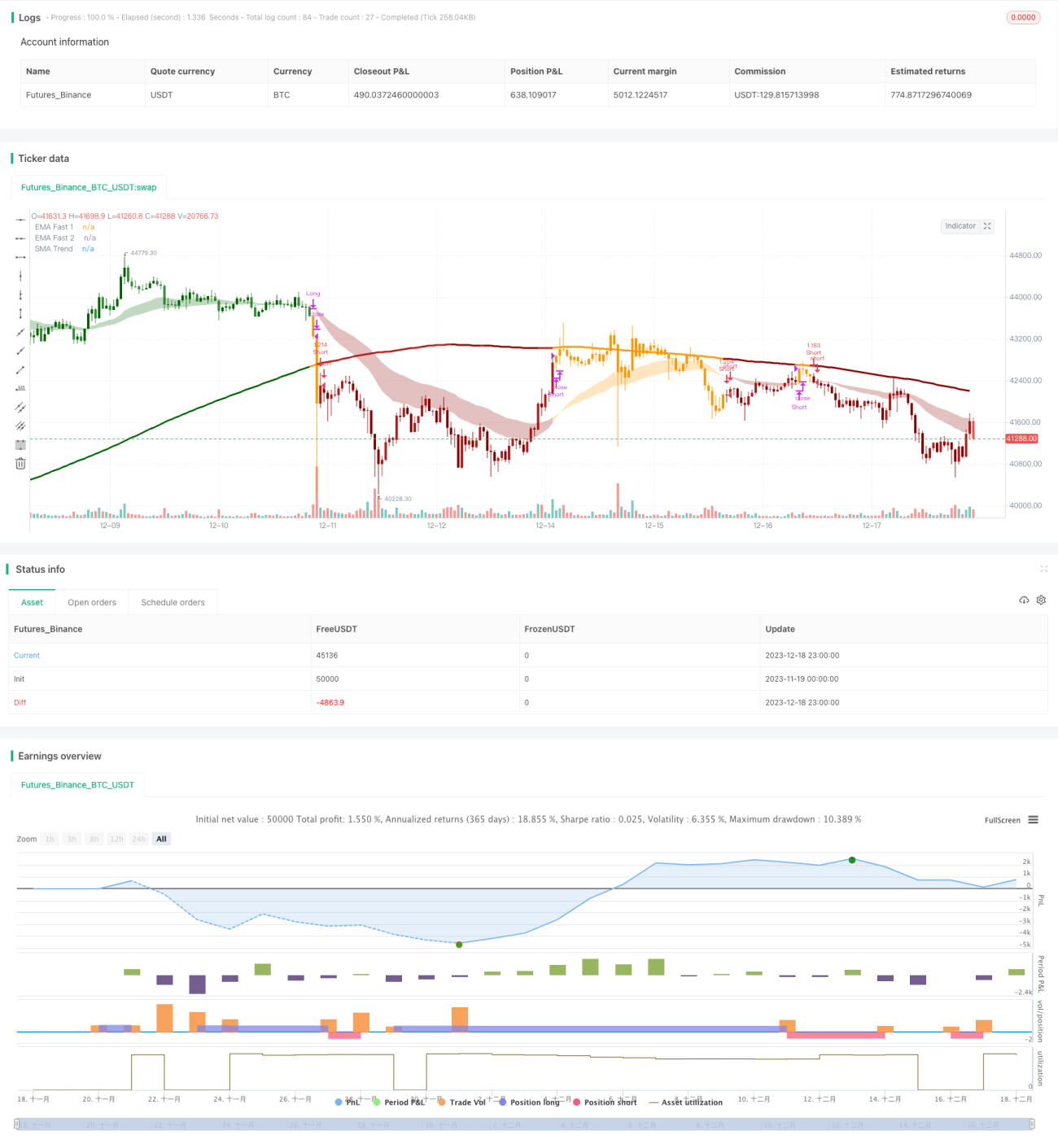

Estratégia de trading quantitativa mista de duplo indicador

Visão Geral

Esta estratégia identifica a direção da tendência e realiza negociações combinando dois indicadores. Primeiro, usa o cruzamento de duas médias móveis (linha rápida e linha média) para julgar a tendência de curto prazo; em segundo lugar, usa a faixa de canal e uma média móvel de longo prazo para determinar a direção principal da tendência. Somente quando os dois julgamentos são consistentes, um sinal de negociação é gerado. Essa abordagem híbrida de múltiplos indicadores pode filtrar sinais falsos e melhorar a estabilidade.

Princípios da Estratégia

A estratégia usa três grupos de indicadores para análise. Primeiro, o cruzamento de ouro (golden cross) e cruzamento da morte (death cross) entre a EMA rápida (período 26) e a EMA média (período 50) determina a tendência de curto prazo; em segundo lugar, calcula a faixa de canal e verifica se o preço rompe essa faixa para julgar a direção de médio prazo (alta ou baixa); por fim, calcula a média móvel simples de longo prazo SMA (período 200) e a compara com o preço para determinar a tendência principal. Somente quando todos os três julgamentos são consistentes, um sinal de negociação é emitido.

Especificamente, a lógica de julgamento é:

-

O cruzamento das linhas rápida e média (golden cross indica alta, death cross indica baixa) determina a direção da tendência de curto prazo.

-

Se o preço rompe a faixa do canal, determina a direção da tendência de médio prazo. A faixa do canal é baseada na média móvel de longo prazo mais ou menos o ATR multiplicado por um coeficiente. Se o preço rompe o limite superior, é de alta; se rompe o limite inferior, é de baixa.

-

A comparação entre o preço e a média móvel de longo prazo determina a direção principal da tendência.

Finalmente, o sinal de negociação só é emitido quando os três julgamentos (curto, médio e longo prazo) são todos consistentes. Essa análise mista filtra efetivamente sinais falsos, melhorando a estabilidade.

Vantagens da Estratégia

Esta estratégia híbrida de indicadores duplos oferece várias vantagens:

-

Filtra efetivamente sinais falsos, aumentando a estabilidade. Como o sinal de negociação requer validação de indicadores de curto, médio e longo prazo, evita-se erros causados por um único indicador.

-

Alta flexibilidade: os parâmetros dos indicadores podem ser ajustados conforme o mercado. Os períodos das médias móveis rápidas/lentas e os parâmetros da faixa do canal podem ser calibrados para diferentes ambientes de mercado.

-

Combina negociação de tendência com negociação de intervalo. Os indicadores de curto e médio prazo capturam a tendência, enquanto o indicador de longo prazo define o intervalo, oferecendo vantagens tanto de estratégias de tendência quanto de reversão.

-

Alta eficiência no uso de capital. Como as ordens são executadas apenas quando múltiplos indicadores concordam, o capital é utilizado de forma eficaz, evitando negociações desnecessárias.

Riscos da Estratégia

A estratégia também apresenta alguns riscos:

-

Risco de configuração de parâmetros. Os períodos das médias móveis e os parâmetros da faixa do canal precisam ser definidos adequadamente. Se inadequados, podem não detectar tendências de forma eficaz ou gerar excesso de sinais falsos.

-

Indicadores duplos aumentam o custo de oportunidade da negociação. Comparada a estratégias de indicador único, pode perder algumas oportunidades de negociação, não conseguindo entrar ou sair nos melhores pontos.

-

A estratégia de stop loss requer cuidado. O mecanismo de stop loss por rompimento pode causar perdas desnecessárias; a porcentagem de stop deve ser definida com cautela.

-

Pode ter desempenho insatisfatório em mercados muito voláteis. A estratégia é mais adequada para ambientes de mercado com tendências claras.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

-

Testar diferentes combinações de parâmetros para encontrar os melhores. Podem ser realizados testes com mais dados históricos para descobrir a configuração ideal.

-

Adicionar um mecanismo de stop loss adaptativo. Combinar com o Indicador de Volatilidade para ajustar dinamicamente a amplitude do stop.

-

Incluir indicadores de volume como suporte adicional. Em pontos-chave, ajudar a decidir o tamanho da posição, melhorando a eficiência do uso de capital.

-

Otimizar a lógica de entrada. Considerar mais estratégias de custo médio (cost averaging) para reduzir o risco de entrada única.

-

Incorporar modelos de aprendizado de máquina para análise. Introduzir redes neurais e outros modelos para avaliar a robustez e o ajuste do modelo.

Resumo

Esta estratégia, por meio de três indicadores (rápido, médio e longo prazo) e um mecanismo de validação dupla, suprime efetivamente sinais falsos e melhora a estabilidade. Ao mesmo tempo, combina as vantagens da negociação de tendência e de intervalo, com alta eficiência no uso de capital. Pode ser aprimorada por meio de otimização de parâmetros, otimização de stop loss e combinação com indicadores de volume, sendo uma estratégia quantitativa híbrida recomendável.

- 1