Estratégia de alta e baixa para criptomoedas baseada em múltiplos indicadores

Visão Geral

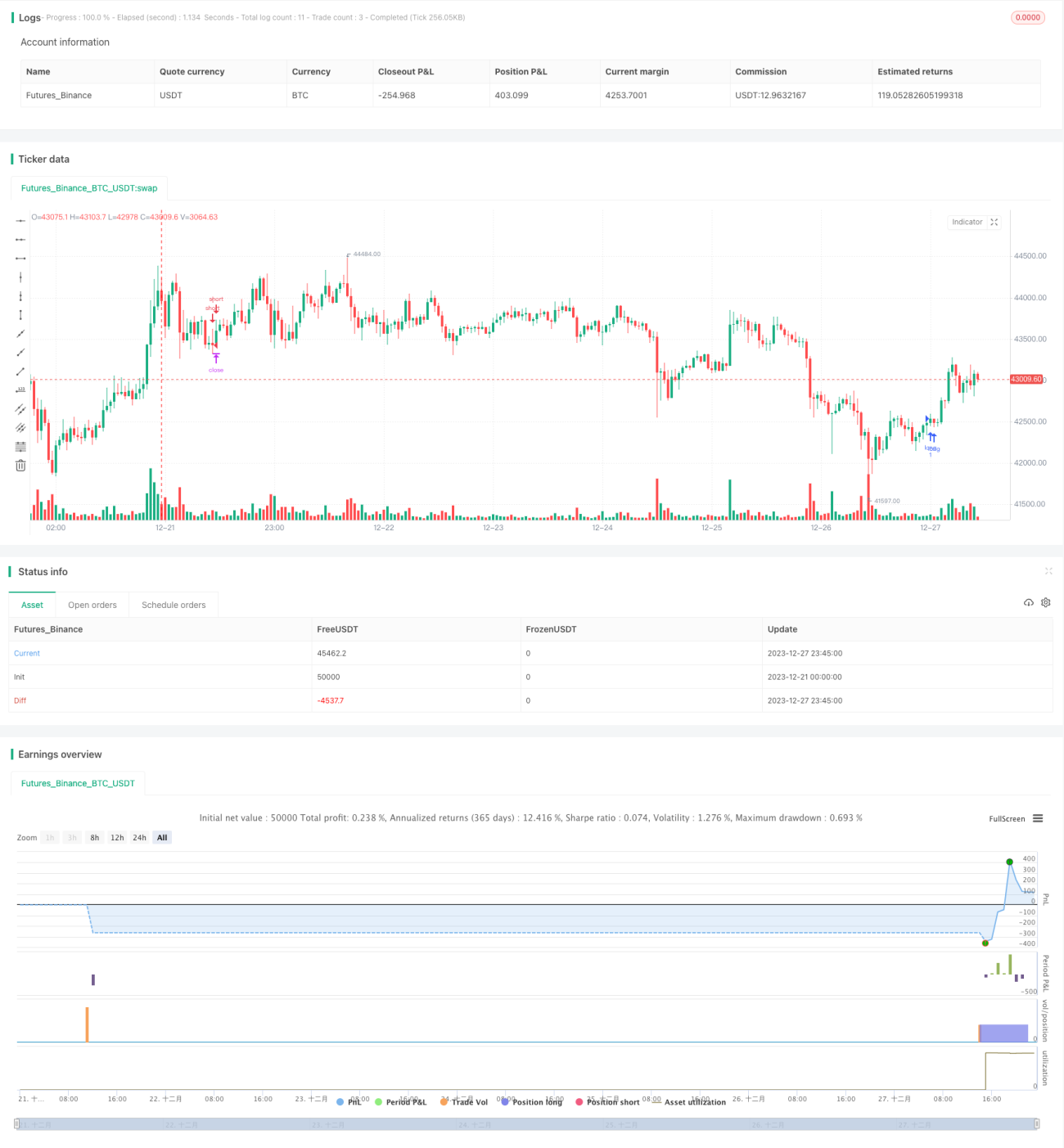

Esta estratégia é uma estratégia de pontos altos e baixos adequada para o mercado de criptomoedas. Ela combina vários indicadores como MACD, PSAR, ATR e Ondas de Elliott, operando em timeframes mais altos, como 1 hora, 4 horas ou 1 dia. A vantagem da estratégia é sua alta relação risco-retorno, com um fator de lucro médio entre 1,5 e 2,5.

Princípio da Estratégia

Os sinais de negociação desta estratégia são gerados a partir de pontos altos e baixos de preço combinados com uma avaliação abrangente de múltiplos indicadores. A lógica específica é:

-

Identificar se o candle apresenta uma faixa de preço alto-baixo, ou seja, máximas consecutivamente mais altas e mínimas consecutivamente mais baixas.

-

Verificar o nível do histograma do MACD.

-

Verificar a direção da tendência com o indicador PSAR.

-

Verificar a direção da tendência com um indicador formado por ATR e MA.

-

Confirmar a direção da tendência com o indicador de Ondas de Elliott.

Se todas as cinco condições acima apontarem para a mesma direção, é gerado um sinal de compra ou venda.

Vantagens da Estratégia

-

Alta relação risco-retorno, podendo chegar a 1:30.

-

Fator de lucro médio elevado, geralmente entre 1,5 e 2,5.

-

Combinação de múltiplos indicadores que filtra efetivamente falsos rompimentos.

Riscos da Estratégia

-

Taxa de acerto baixa, apenas entre 10% e 20%.

-

Existe certo risco de drawdown e de mercado lateral.

-

A eficácia dos indicadores pode ser afetada pelo ambiente de mercado.

-

Exige forte resiliência psicológica.

Medidas correspondentes:

-

Aumentar o volume de capital de negociação para equilibrar a taxa de acerto.

-

Controlar rigorosamente o stop loss de cada operação.

-

Ajustar os parâmetros dos indicadores conforme os diferentes mercados.

-

Preparar-se psicologicamente e controlar o tamanho das posições.

Direções de Otimização

-

Testar parâmetros dos indicadores para diferentes criptomoedas e ambientes de mercado.

-

Adicionar estratégias de stop loss e take profit para otimizar o gerenciamento de capital.

-

Combinar métodos de aprendizado de máquina para aumentar a taxa de acerto.

-

Incluir indicadores de sentimento social para filtrar os sinais de negociação.

-

Considerar a confirmação de múltiplos timeframes.

Resumo

No geral, esta é uma estratégia de alto risco e alto retorno adequada para criptomoedas. Sua vantagem está na alta relação risco-retorno, capaz de proporcionar um fator de lucro médio elevado. O principal risco é a baixa taxa de acerto, exigindo forte resiliência psicológica. As próximas direções de otimização podem incluir ajuste de parâmetros, melhoria do gerenciamento de capital e aumento da taxa de acerto, entre outras dimensões. De modo geral, esta estratégia possui valor prático para traders de criptomoedas que buscam altos retornos.

- 1