Estratégia de acompanhamento de tendência baseada no Average True Range (ATR)

Visão Geral

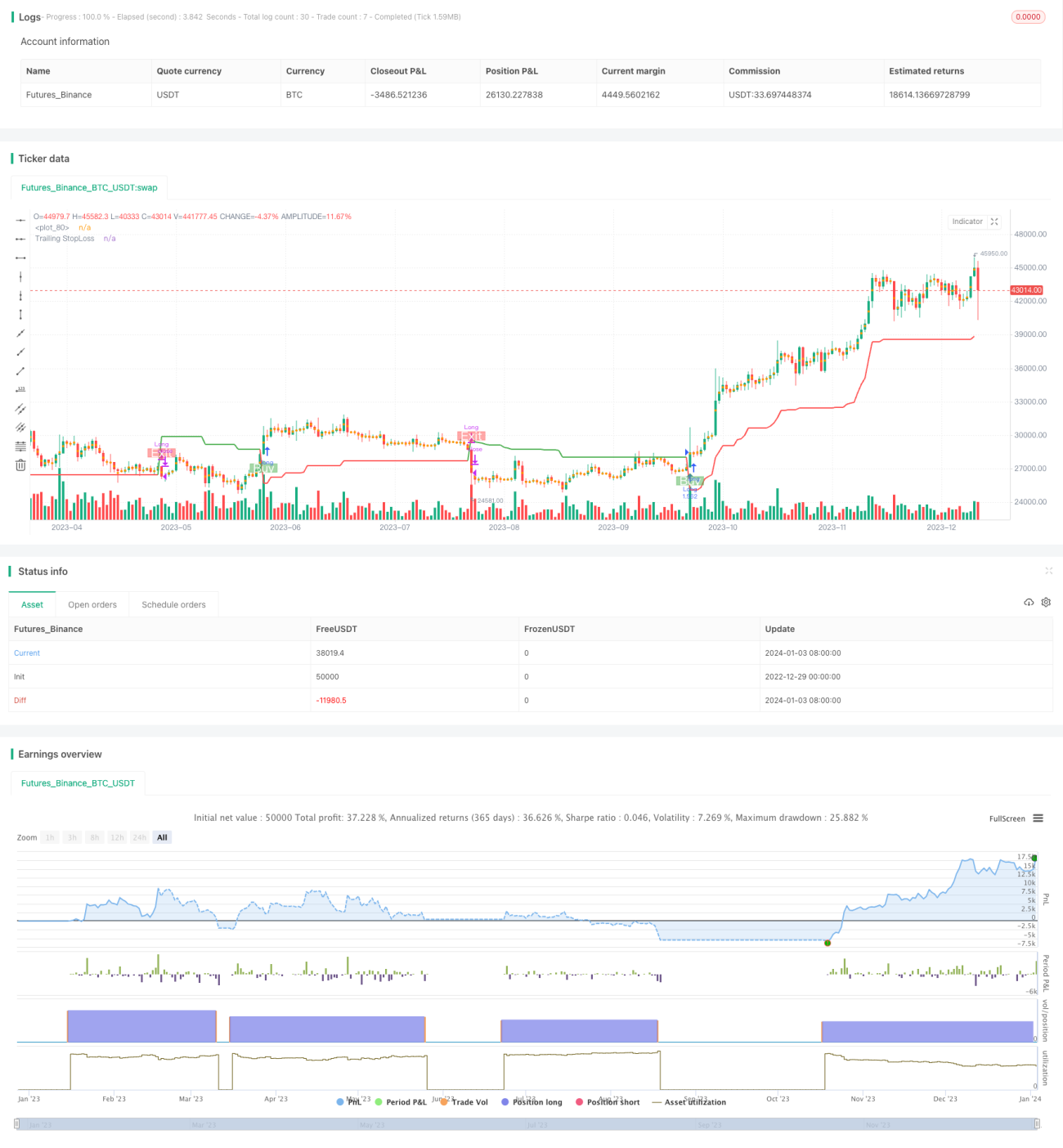

Esta estratégia é uma estratégia de rastreamento de tendências baseada no Average True Range (ATR). Ela utiliza o ATR para calcular os valores dos indicadores, determinando assim a direção da tendência do preço. A estratégia também fornece um mecanismo de stop loss para controlar o risco.

Princípio da Estratégia

A estratégia usa três parâmetros principais: Período (Period), Multiplicador (Multiplier) e Ponto de Entrada/Saída (Entry/Exit Point). Os parâmetros padrão são um período de 14 para o ATR e um multiplicador de 4x.

A estratégia primeiro calcula o preço médio de compra (buyavg) e o preço médio de venda (sellavg), depois compara o preço atual com essas duas médias para determinar a direção da tendência atual. Se o preço estiver acima do preço médio de venda, é considerado uma tendência de alta; se o preço estiver abaixo do preço médio de compra, é considerado uma tendência de baixa.

Além disso, a estratégia combina o ATR para definir um trailing stop loss. Especificamente, a distância do stop é calculada multiplicando a média móvel ponderada de 14 períodos do ATR por um multiplicador (padrão de 4). Isso permite ajustar a distância do stop de acordo com a volatilidade do mercado.

Quando o stop é acionado, a estratégia fecha a posição para realizar o lucro.

Vantagens da Estratégia

- Baseada na determinação da tendência, permite negociar a favor da tendência e obter lucros contínuos.

- Utiliza o ATR para ajustar dinamicamente a distância do stop loss, controlando efetivamente o risco.

- O cálculo dos pontos de compra e venda é simples e direto, fácil de entender e implementar.

Riscos e Contramedidas

- Quando a tendência se inverte, pode haver perdas significativas.

- Ajustar adequadamente o período do ATR e o multiplicador para otimizar a distância do stop.

- Em mercados oscilantes, podem ocorrer múltiplas pequenas perdas.

- Adicionar filtros para evitar mercados sem tendência clara.

- Parâmetros mal configurados podem piorar o desempenho da estratégia.

- Realizar testes de otimização com múltiplas combinações de parâmetros para encontrar os melhores valores.

Direções de Otimização da Estratégia

- Adicionar outros indicadores para filtrar sinais, evitando entradas e saídas em mercados oscilantes.

- Otimizar os parâmetros de período e multiplicador do ATR para tornar a distância do stop loss mais adequada.

- Incluir controle de tamanho de posição na abertura, ajustando o tamanho da posição de acordo com as condições do mercado.

Resumo

No geral, esta estratégia é uma estratégia de rastreamento de tendências simples e prática. Ela requer apenas alguns parâmetros para ser implementada e, ao ajustar dinamicamente o stop loss por meio do ATR, pode controlar o risco de forma eficaz. Se combinada com outros indicadores auxiliares, pode ser ainda mais otimizada, filtrando alguns sinais ruidosos. Em suma, esta estratégia é adequada para quem deseja aprender estratégias de rastreamento de tendências e também pode ser usada como componente básico para outras estratégias mais avançadas.

/*backtest

start: 2022-12-29 00:00:00

end: 2024-01-04 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('Trend Strategy by zdmre', shorttitle='Trend Strategy', overlay=true, pyramiding=0, currency=currency.USD, default_qty_type=strategy.percent_of_equity, initial_capital=10000, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.005)

show_STOPLOSSprice = input(true, title='Show TrailingSTOP Prices')

src = input(close, title='Source')- 1