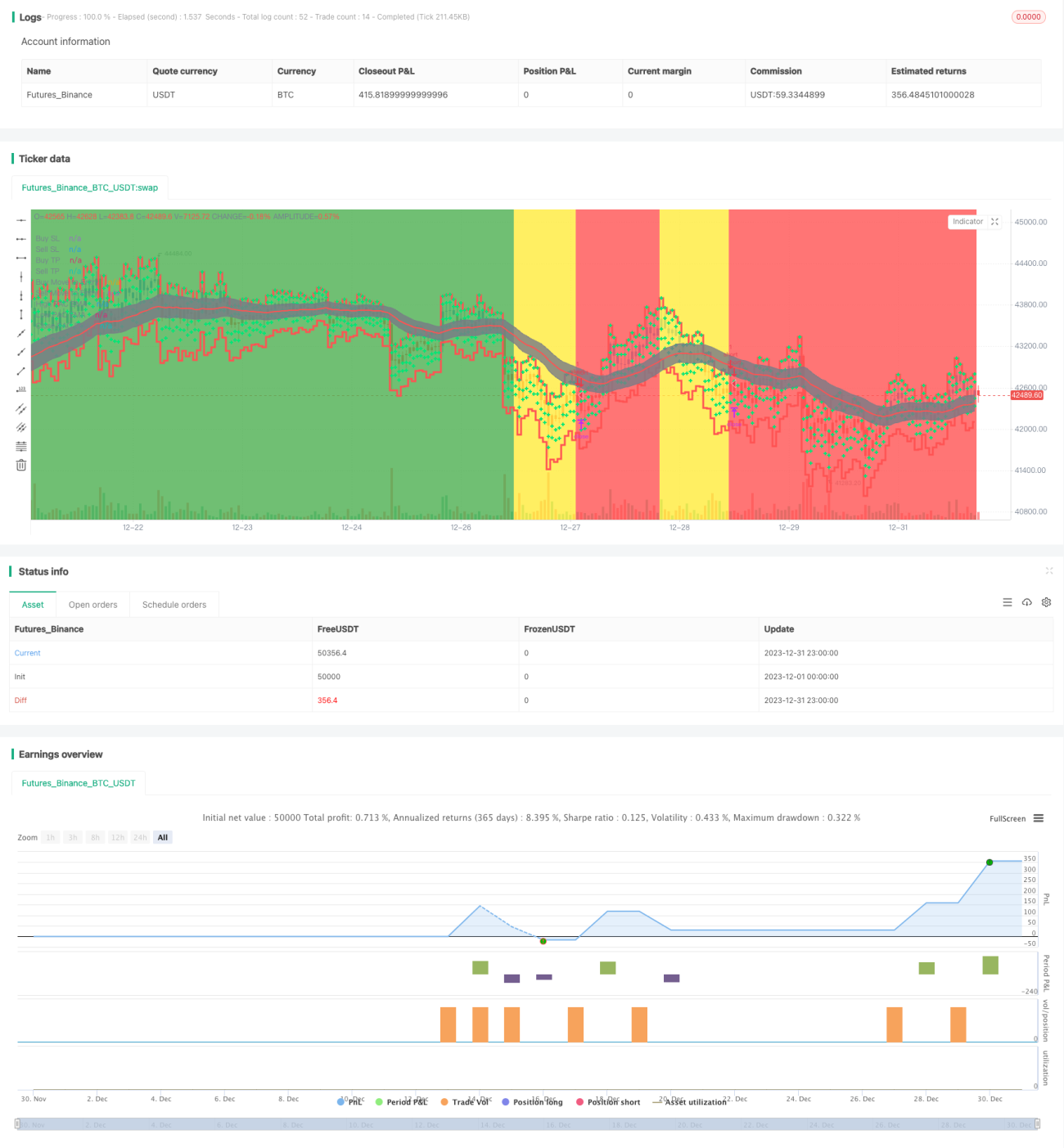

Estratégia de Rastreamento de Tendência com Canal de Preços de Duas Médias Móveis

Visão Geral

Esta estratégia é uma estratégia de acompanhamento de tendência que constrói um canal de preços com base em duas médias móveis, usa o intervalo do canal para determinar a direção da tendência de preços e define um trailing stop para travar lucros.

Princípio da Estratégia

A estratégia de canal de preços com duas médias móveis usa uma EMA rápida e uma EMA lenta para construir o canal de preços. A EMA rápida tem período 89, a EMA lenta tem período 200. Ao mesmo tempo, usa três médias móveis baseadas no preço máximo, mínimo e de fechamento para construir o intervalo do canal de preços. As linhas superior e inferior do canal são, respectivamente, a EMA de 34 períodos do preço máximo e a EMA de 34 períodos do preço mínimo.

Quando a EMA rápida está acima da EMA lenta e o preço está abaixo da linha inferior, considera-se uma tendência de alta; quando a EMA rápida está abaixo da EMA lenta e o preço está acima da linha superior, considera-se uma tendência de baixa.

Em tendência de alta, a estratégia realiza vendas (short) quando se confirma a reversão da tendência; em tendência de baixa, a estratégia realiza compras (long) quando se confirma a reversão da tendência.

Além disso, a estratégia possui função de trailing stop. Após a posição ser aberta, o preço do trailing stop é atualizado em tempo real, travando os lucros.

Análise de Vantagens

A maior vantagem desta estratégia é usar as duas médias móveis para construir um canal de preços para determinar a tendência de preços e, em seguida, combinar com negociações de reversão, evitando comprar caro e vender barato. Ao mesmo tempo, possui função de trailing stop móvel, que pode travar lucros e reduzir o risco de perdas.

Outras vantagens incluem: grande espaço para otimização de parâmetros, que podem ser ajustados para diferentes ativos e períodos; atualização em tempo real do preço de stop, baixo risco operacional.

Análise de Riscos

O principal risco desta estratégia é a eficácia da determinação do sinal de reversão, que pode resultar em falsos julgamentos. Nesse caso, é necessário otimizar os parâmetros para garantir a eficácia na determinação da reversão da tendência.

Além disso, a definição do ponto de stop também é crucial. Um ponto de stop muito grande pode resultar em stop não decisivo; um ponto de stop muito pequeno pode resultar em stop excessivo. Isso precisa ser ajustado de acordo com o ativo específico.

Finalmente, problemas de dados também podem levar à ineficácia da estratégia. É necessário garantir que sejam usados dados históricos confiáveis, contínuos e suficientes para backtest e validação em tempo real da estratégia.

Direções de Otimização

A otimização desta estratégia concentra-se principalmente nos seguintes aspectos:

-

Os períodos da EMA rápida e da EMA lenta podem ser otimizados, configurando diferentes combinações de parâmetros para avaliar a eficácia.

-

Os parâmetros das linhas superior e inferior do canal de preços também podem ser ajustados, buscando parâmetros de período mais adequados.

-

A definição do ponto de stop é crucial; diferentes parâmetros podem ser testados para otimizar a estratégia de stop.

-

Pode-se testar a introdução de outros indicadores para determinar a reversão da tendência, melhorando a eficácia das negociações.

Resumo

O processo operacional geral desta estratégia é razoável e suave. Usa o canal de duas médias móveis para determinar a direção da tendência e realizar negociações, e possui trailing stop para travar lucros, sendo uma estratégia de acompanhamento de tendência relativamente estável. Através da otimização de parâmetros e da configuração de gerenciamento de risco, esta estratégia pode se tornar uma das estratégias de negociação quantitativa eficientes.

- 1