متحرک نظریاتی رجحان الٹنے کی حکمت عملی

جائزہ

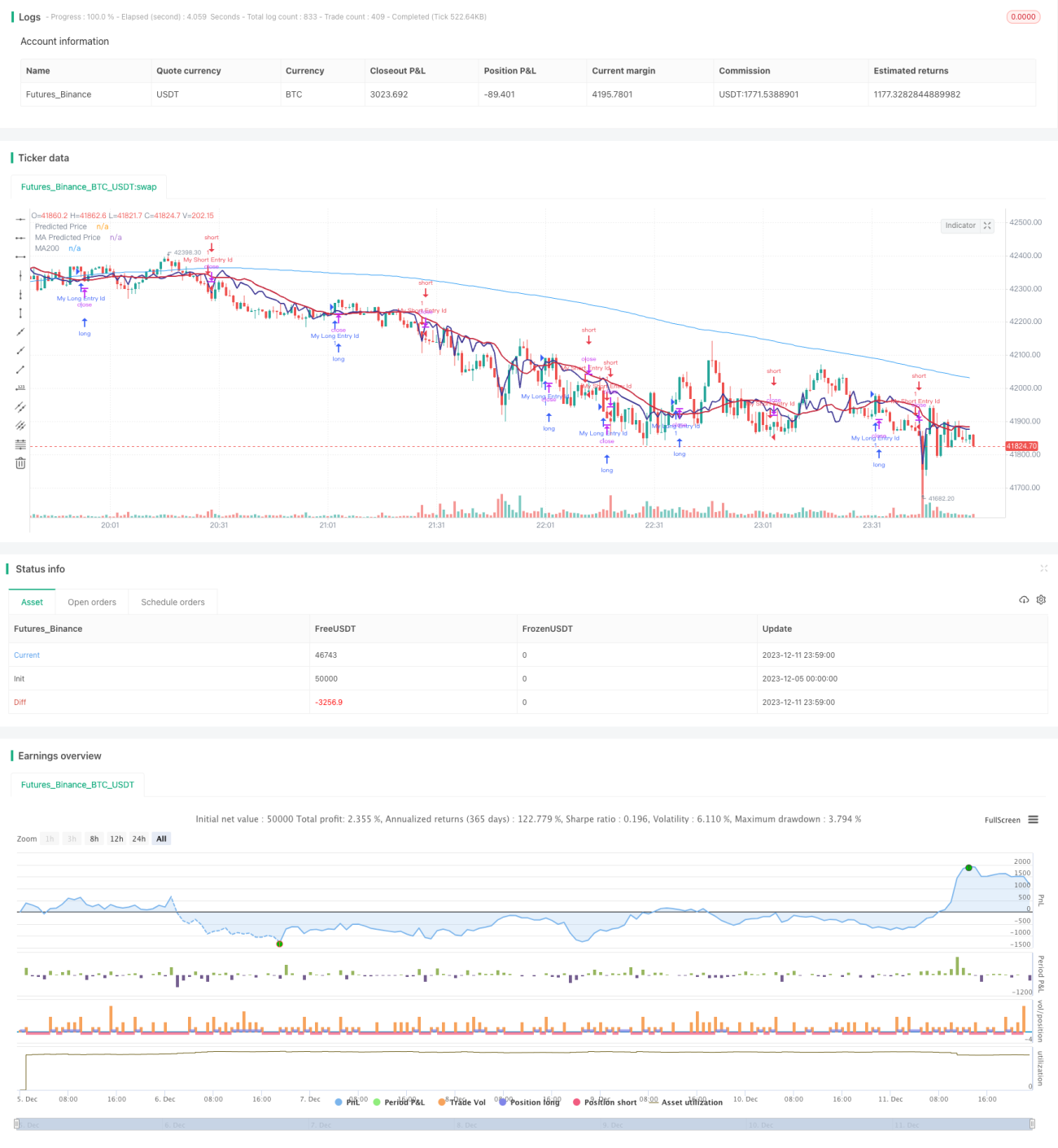

متحرک نظریاتی رجحان الٹنے کی حکمت عملی لکیری ریگریشن کے ذریعے قیمت کی پیش گوئی کرتی ہے اور موونگ ایوریج سے بننے والے نظریے کو ٹریڈنگ سگنل جنریشن کے لیے استعمال کرتی ہے۔ جب پیش گوئی شدہ قیمت نیچے سے اوپر موونگ ایوریج کو عبور کرتی ہے تو خرید کا سگنل پیدا ہوتا ہے؛ جب پیش گوئی شدہ قیمت اوپر سے نیچے موونگ ایوریج کو عبور کرتی ہے تو فروخت کا سگنل پیدا ہوتا ہے، اس طرح رجحان کے الٹنے کو پکڑا جاتا ہے۔

حکمت عملی کا اصول

- تجارتی حجم کی بنیاد پر اسٹاک کی قیمت کے لکیری ریگریشن کا حساب لگا کر قیمت کی پیش گوئی کی جاتی ہے

- مختلف شرائط میں موونگ ایوریج کا حساب لگایا جاتا ہے

- جب پیش گوئی شدہ قیمت نیچے سے اوپر موونگ ایوریج کو عبور کرتی ہے تو خرید کا سگنل پیدا ہوتا ہے

- جب پیش گوئی شدہ قیمت اوپر سے نیچے موونگ ایوریج کو عبور کرتی ہے تو فروخت کا سگنل پیدا ہوتا ہے

- ایم اے سی ڈی انڈیکیٹر کے ساتھ مل کر رجحان کے الٹنے کے وقت کا تعین کیا جاتا ہے

مندرجہ بالا سگنل مختلف تصدیقات کے ساتھ مل کر جھوٹی بریک آؤٹ سے بچتے ہیں، اس طرح سگنل کی درستگی میں اضافہ ہوتا ہے۔

فوائد کا تجزیہ

- لکیری ریگریشن کے ذریعے قیمت کے رجحان کی پیش گوئی کرکے سگنل کی درستگی میں اضافہ

- موونگ ایوریج کے ساتھ مل کر نظریہ تشکیل دے کر رجحان کے الٹنے کو پکڑنا

- تجارتی حجم کی بنیاد پر لکیری ریگریشن کا حساب لگانا زیادہ معاشی معنی رکھتا ہے

- ایم اے سی ڈی جیسے انڈیکیٹرز کے ساتھ متعدد تصدیقات کرکے جھوٹے سگنلز کو کم کرنا

خطرات کا تجزیہ

- لکیری ریگریشن کے پیرامیٹرز کی سیٹنگ نتائج پر بہت زیادہ اثر ڈالتی ہے

- موونگ ایوریج کی سیٹنگ بھی سگنل کے معیار کو متاثر کرتی ہے

- تصدیق کے طریقہ کار کے باوجود جھوٹے سگنلز کا خطرہ موجود ہے

- کوڈ کو مزید بہتر بنایا جا سکتا ہے تاکہ ٹریڈز کی تعداد کم ہو اور منافع کی شرح بڑھے

بہتری کی سمت

- لکیری ریگریشن اور موونگ ایوریج کے پیرامیٹرز کو بہتر بنانا

- تصدیق کی شرائط بڑھانا تاکہ جھوٹے سگنلز کی شرح کم ہو

- رجحان کے الٹنے کے معیار کا تعین کرنے کے لیے مزید عوامل شامل کرنا

- سٹاپ لاس کی حکمت عملی کو بہتر بنانا تاکہ ایک ٹریڈ کے خطرے کو کم کیا جا سکے

خلاصہ

متحرک نظریاتی رجحان الٹنے کی حکمت عملی لکیری ریگریشن کی پیش گوئی اور موونگ ایوریج سے بننے والے نظریے کو یکجا کرتی ہے تاکہ رجحان کے الٹنے کے وقت کو پکڑا جا سکے۔ ایک واحد انڈیکیٹر کے مقابلے میں اس کی قابل اعتمادی زیادہ ہے۔ ساتھ ہی، حکمت عملی کو پیرامیٹرز کی ایڈجسٹمنٹ اور تصدیق کی شرائط کی بہتری کے ذریعے مزید سگنل کے معیار اور منافع کی سطح کو بہتر بنایا جا سکتا ہے۔

/*backtest

start: 2023-12-05 00:00:00

end: 2023-12-12 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © stocktechbot

//@version=5

strategy("Linear Cross", overlay=true, margin_long=100, margin_short=0)- 1