Chiến lược theo dõi xu hướng đột phá động lượng

Tổng quan

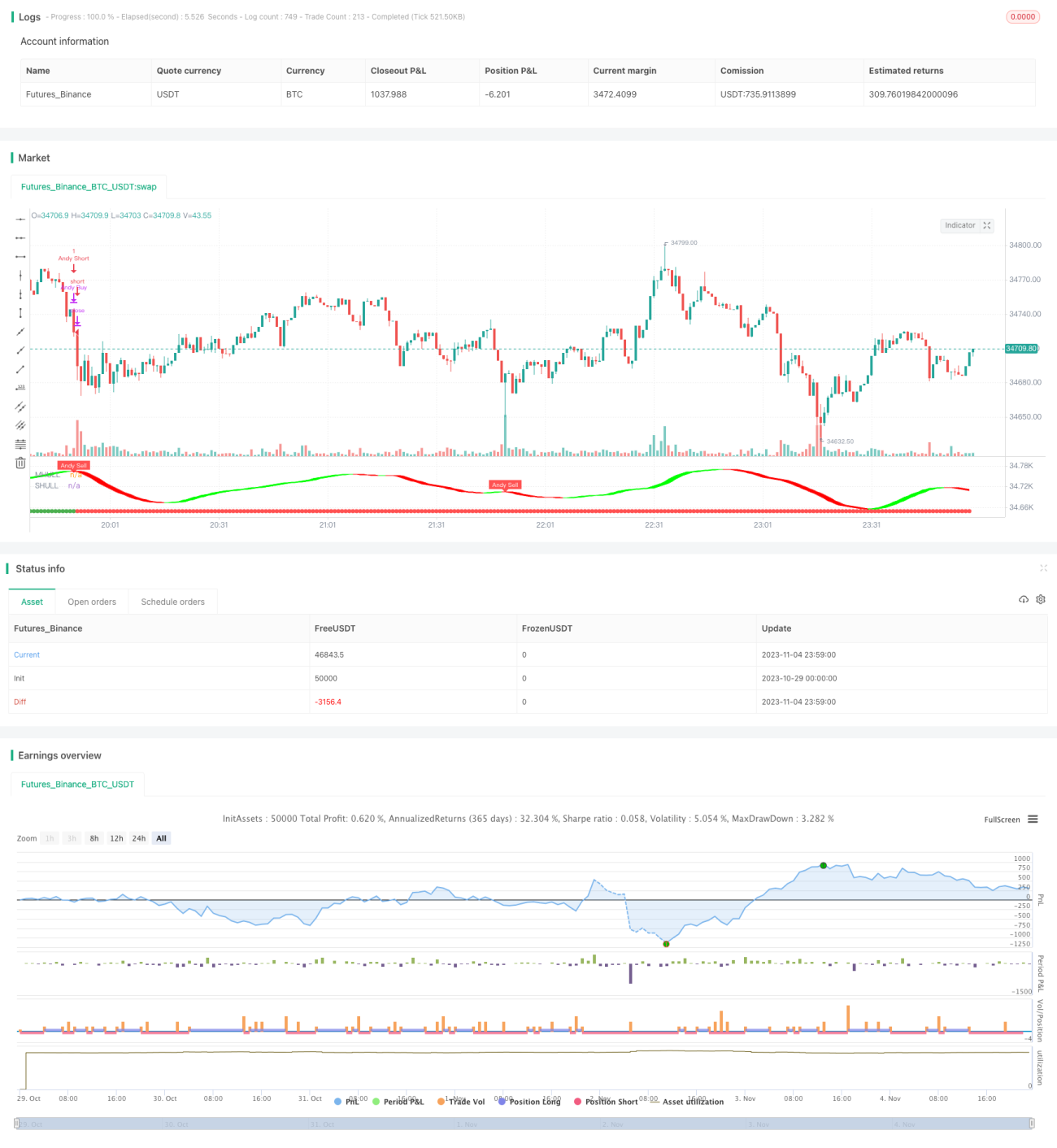

Chiến lược này kết hợp nhiều chỉ báo kỹ thuật để xác định hướng xu hướng, theo dõi khi xu hướng có sự bứt phá động lượng, nhằm đạt được lợi nhuận vượt trội.

Nguyên lý chiến lược

-

Sử dụng kênh Donchian để xác định hướng xu hướng tổng thể. Khi giá phá vỡ kênh này, xác nhận xu hướng đã thay đổi.

-

Đường trung bình động Hull hỗ trợ xác định hướng xu hướng. Chỉ báo này nhạy cảm với biến động giá, có thể phát hiện sớm sự đảo chiều xu hướng.

-

Hệ thống bán quỹ đạo phát ra tín hiệu mua và bán. Hệ thống này dựa trên kênh giá và phạm vi dao động thực trung bình, giúp tránh các phá vỡ giả.

-

Khi kênh Donchian, chỉ báo Hull và hệ thống bán quỹ đạo đồng thời phát tín hiệu, xác định xu hướng có sự bứt phá động lượng mạnh, lúc này vào lệnh.

-

Điều kiện thoát lệnh: Khi các chỉ báo trên phát tín hiệu ngược chiều, xác định xu hướng đảo chiều, cắt lỗ ngay lập tức để thoát.

Phân tích ưu điểm

-

Kết hợp nhiều chỉ báo, khả năng phán đoán mạnh hơn. Kênh Donchian xác định xu hướng cơ bản, chỉ báo Hull và bán quỹ đạo xác định chi tiết, nắm bắt chính xác điểm đảo chiều xu hướng.

-

Tham gia bứt phá động lượng, theo đuổi lợi nhuận vượt trội. Chỉ vào lệnh khi xu hướng có sự bứt phá mạnh, tránh bị kẹt trong dao động.

-

Cắt lỗ nghiêm ngặt, bảo vệ an toàn vốn. Khi chỉ báo phát tín hiệu ngược chiều, cắt lỗ ngay, tránh thua lỗ mở rộng.

-

Tham số điều chỉnh linh hoạt, thích ứng với nhiều loại thị trường. Có thể điều chỉnh độ dài kênh, phạm vi biến động và các tham số khác, tối ưu hóa cho các chu kỳ khác nhau.

-

Dễ hiểu và dễ thực hiện, người mới cũng có thể nắm bắt. Các chỉ báo và điều kiện kết hợp đơn giản, dễ dàng lập trình.

Phân tích rủi ro

-

Bỏ lỡ cơ hội đầu xu hướng. Thời điểm vào lệnh muộn, không bắt được đà tăng ban đầu.

-

Rủi ro thoái lui sau khi phá vỡ thất bại. Sau khi vào lệnh có thể xảy ra phá vỡ thất bại và đảo chiều, gây thua lỗ.

-

Chỉ báo phát tín hiệu sai. Do cài đặt tham số không phù hợp, phán đoán của chỉ báo có thể sai.

-

Số lần giao dịch hạn chế. Chỉ vào lệnh khi xu hướng bứt phá rõ ràng, số lần giao dịch trong năm có hạn.

Hướng tối ưu hóa

-

Tối ưu hóa tổ hợp tham số. Thử nghiệm các tham số khác nhau để tìm ra tổ hợp tốt nhất.

-

Thêm điều kiện thoái lui tuyến tính cắt lỗ. Tránh cắt lỗ quá sớm, bỏ lỡ cơ hội xu hướng.

-

Thêm các chỉ báo khác để lọc. Ví dụ MACD, KDJ hỗ trợ phán đoán, giảm tín hiệu sai.

-

Tối ưu hóa khung thời gian giao dịch. Tham số có thể tối ưu hóa cho các khung thời gian khác nhau.

-

Mở rộng hiệu suất sử dụng vốn. Sử dụng đòn bẩy, đầu tư định kỳ để nâng cao hiệu quả sử dụng vốn.

Tổng kết

Chiến lược này kết hợp nhiều chỉ báo để xác định thời điểm xu hướng bứt phá động lượng, theo dõi xu hướng đã hình thành để đạt được lợi nhuận vượt trội. Cơ chế cắt lỗ nghiêm ngặt kiểm soát rủi ro, tham số linh hoạt thích ứng với các môi trường thị trường khác nhau. Mặc dù tần suất giao dịch thấp, nhưng mỗi giao dịch đều cố gắng đạt được lợi nhuận cao. Thông qua tối ưu hóa tham số, đưa vào các chỉ báo phụ trợ, chiến lược này có thể được cải thiện liên tục.

- 1