Chiến lược đường trung bình động phá vỡ dải Bollinger

1

Follow

1802

Followers

Tổng quan

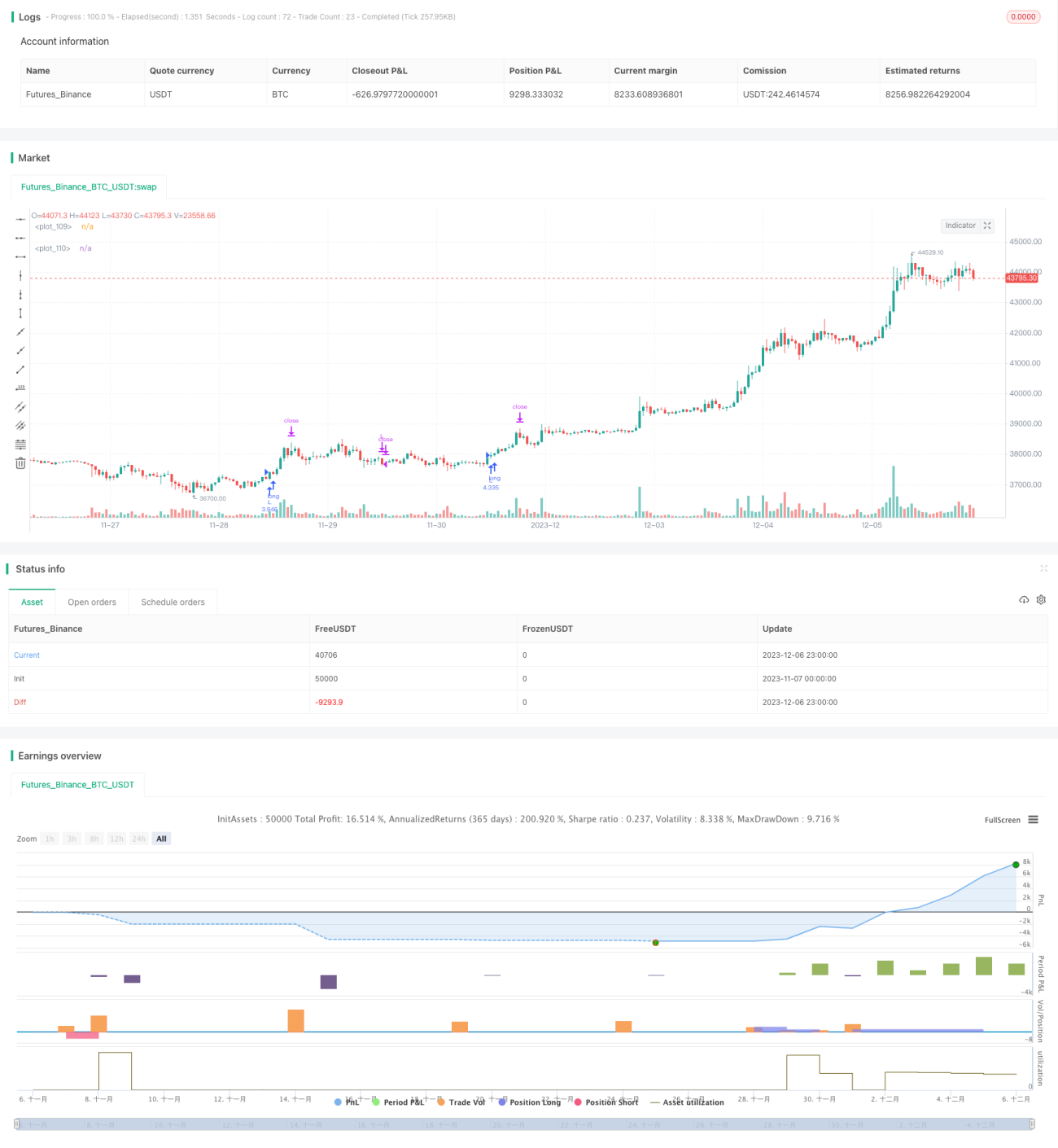

Chiến lược này kết hợp chỉ báo đường trung bình động, chỉ báo Bollinger Bands và chỉ báo UT Bot Alerts để thực hiện một chiến lược giao dịch phá vỡ đơn giản. Khi giá phá vỡ dải trên của Bollinger Bands, vào lệnh mua; khi giá phá vỡ dải dưới của Bollinger Bands, vào lệnh bán.

Nguyên lý chiến lược

- Sử dụng EMA chu kỳ 200 làm trục giữa để xác định xu hướng. Giá nằm trên EMA là xu hướng tăng, giá nằm dưới EMA là xu hướng giảm.

- Chỉ báo UT Bot Alerts kết hợp với ATR tạo ra tín hiệu mua bán. Khi giá và EMA nhanh cắt lên dải trên của Bollinger Bands phát sinh tín hiệu mua; khi giá và EMA nhanh cắt xuống dải dưới của Bollinger Bands phát sinh tín hiệu bán.

- Chỉ báo dừng lỗ ATR được sử dụng để đặt điểm dừng lỗ. Khoảng cách dừng lỗ bằng 1,5 lần giá trị ATR.

- Sau khi vào lệnh, sử dụng tỷ lệ lợi nhuận/rủi ro để đặt điểm dừng lỗ, chốt lời và di chuyển dừng lỗ về giá vào lệnh.

Phân tích ưu điểm

- Sử dụng chỉ báo Bollinger Bands để xác định thời điểm thích hợp mua hoặc bán, có thể tăng xác suất có lợi nhuận.

- Chỉ báo UT Bot Alerts có thể tạo ra tín hiệu khá chính xác.

- Áp dụng tỷ lệ lợi nhuận/rủi ro để dừng lỗ và chốt lời, có thể kiểm soát rủi ro hiệu quả.

Phân tích rủi ro

- Bollinger Bands dễ phát sinh tín hiệu sai trong thị trường đi ngang.

- ATR có độ trễ, trong giai đoạn đầu của xu hướng khoảng cách dừng lỗ có thể quá lớn.

- Việc thiết lập tỷ lệ lợi nhuận/rủi ro không phù hợp có thể dẫn đến quá mạo hiểm hoặc quá bảo thủ.

Hướng tối ưu hóa

- Có thể thử sử dụng chỉ báo khác thay thế chỉ báo UT Bot Alerts.

- Có thể tối ưu hóa chu kỳ và bội số của ATR để khoảng cách dừng lỗ phù hợp hơn.

- Có thể thử nghiệm các tỷ lệ lợi nhuận/rủi ro khác nhau để tìm ra tham số tối ưu.

Tổng kết

Chiến lược này tích hợp ưu điểm của nhiều chỉ báo, có tính thực tiễn cao. Thông qua tối ưu hóa tham số, có thể trở thành một hệ thống phá vỡ ổn định và đáng tin cậy. Tuy nhiên, cũng cần chú ý phòng ngừa rủi ro do chỉ báo mất hiệu lực và tham số không phù hợp.

Source

Pine

/*backtest

start: 2023-11-07 00:00:00

end: 2023-12-07 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=5

//Developed by StrategiesForEveryone

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1