Chiến lược cắt lỗ theo dõi siêu xu hướng

Tổng quan

Chiến lược này dựa trên chỉ báo siêu xu hướng và cắt lỗ theo dõi để mở và đóng vị thế. Nó sử dụng 4 cảnh báo để mở và đóng vị thế, đồng thời áp dụng chiến lược siêu xu hướng. Chiến lược được thiết kế đặc biệt cho robot, với chức năng cắt lỗ theo dõi.

Nguyên lý chiến lược

Chiến lược sử dụng chỉ báo ATR để tính toán dải trên và dải dưới. Khi giá đóng cửa phá vỡ dải trên, tín hiệu mua được tạo ra; khi phá vỡ dải dưới, tín hiệu bán xuất hiện. Chiến lược cũng sử dụng đường siêu xu hướng để xác định hướng xu hướng. Khi đường siêu xu hướng cắt lên, thị trường tăng bắt đầu; khi cắt xuống, thị trường giảm bắt đầu. Chiến lược mở vị thế khi có tín hiệu, đồng thời đặt giá cắt lỗ ban đầu. Sau đó, giá cắt lỗ sẽ được điều chỉnh theo biến động giá để khóa lợi nhuận, đạt được hiệu quả cắt lỗ theo dõi.

Phân tích ưu điểm

Chiến lược này kết hợp ưu điểm của chỉ báo siêu xu hướng trong việc xác định xu hướng và chỉ báo ATR trong việc đặt cắt lỗ, giúp lọc hiệu quả các phá vỡ giả. Cắt lỗ theo dõi giúp khóa lợi nhuận tốt, giảm sụt giảm. Ngoài ra, chiến lược được thiết kế đặc biệt cho robot, có thể giao dịch tự động.

Phân tích rủi ro

Chỉ báo siêu xu hướng dễ tạo ra nhiều tín hiệu sai. Khi biên độ điều chỉnh giá cắt lỗ lớn, xác suất cắt lỗ bị xuyên thủng sẽ tăng lên. Hơn nữa, giao dịch robot cũng phải đối mặt với các rủi ro kỹ thuật như máy chủ ngừng hoạt động, mất kết nối mạng.

Để giảm xác suất tín hiệu sai, có thể điều chỉnh tham số ATR phù hợp hoặc thêm các chỉ báo khác để lọc. Khi điều chỉnh biên độ theo dõi cắt lỗ, cần cân bằng giữa lợi nhuận và rủi ro. Đồng thời chuẩn bị máy chủ dự phòng và mạng để phòng ngừa rủi ro sự cố kỹ thuật.

Hướng tối ưu hóa

Chiến lược có thể được tối ưu hóa theo các hướng sau:

-

Thêm các chỉ báo hoặc điều kiện để lọc tín hiệu vào lệnh, tránh tín hiệu sai. Ví dụ: có thể thêm chỉ báo MACD.

-

Có thể kiểm tra các tổ hợp tham số ATR khác nhau để tìm ra tham số tối ưu.

-

Có thể tối ưu hóa biên độ theo dõi cắt lỗ để tìm điểm cân bằng tốt nhất.

-

Có thể thêm nhiều mức giá cắt lỗ hơn để thực hiện cắt lỗ phân tán.

-

Có thể xây dựng kiến trúc máy chủ dự phòng chính/phụ, chuyển đổi nhanh khi máy chủ chính gặp sự cố.

Tổng kết

Chiến lược này tích hợp ưu điểm của chỉ báo siêu xu hướng và cắt lỗ theo dõi, có thể tự động mở vị thế và cắt lỗ. Kết hợp với các biện pháp cải tiến theo hướng tối ưu hóa khi giao dịch thực tế, nó có thể trở thành một chiến lược giao dịch định lượng rất thiết thực.

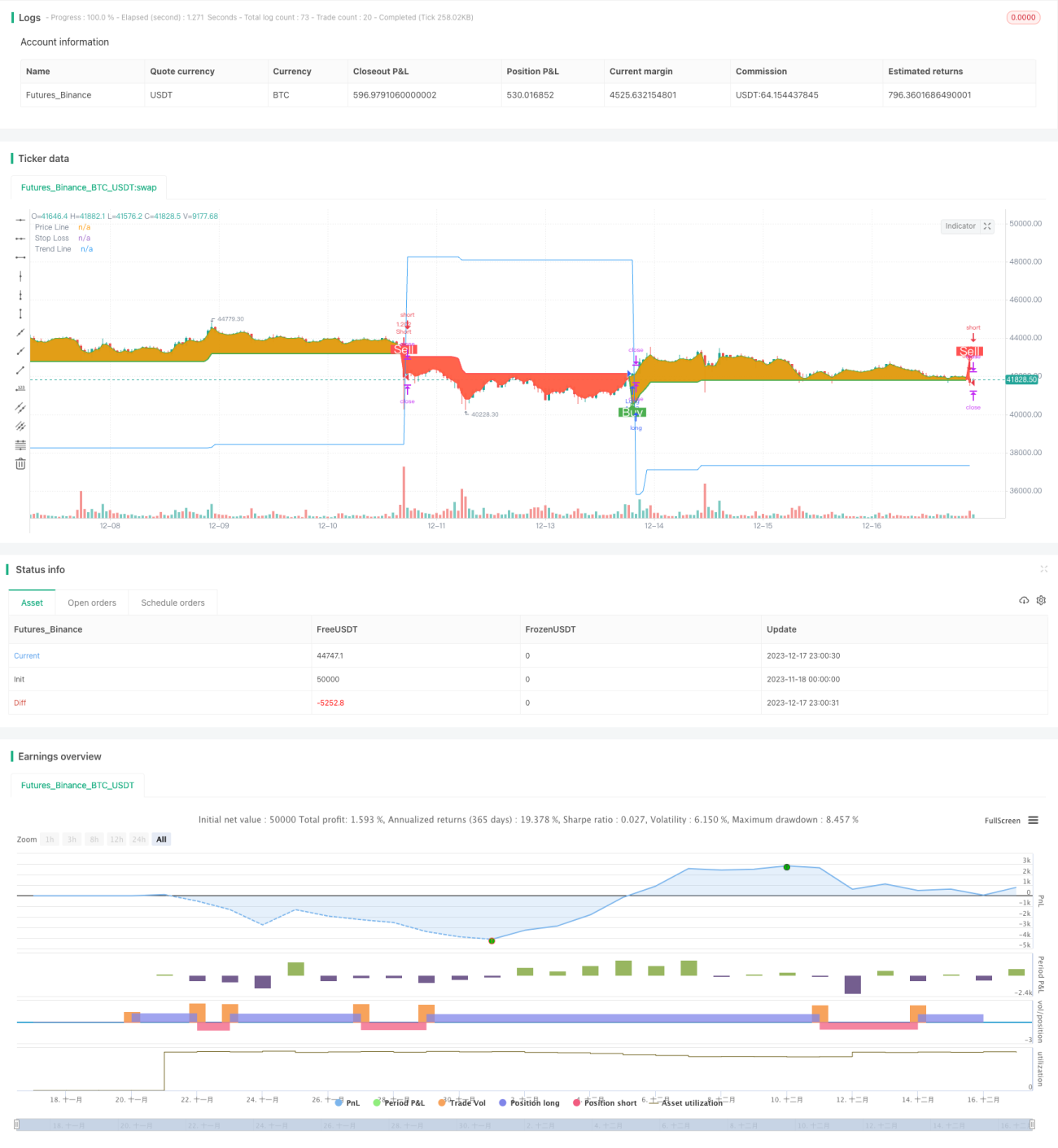

/*backtest

start: 2023-11-18 00:00:00

end: 2023-12-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © arminomid1375

//@version=5

strategy('Mizar_BOT_super trend', overlay=true, default_qty_value=100, currency=currency.USD, default_qty_type=strategy.percent_of_equity, initial_capital=100, max_bars_back=4000)- 1