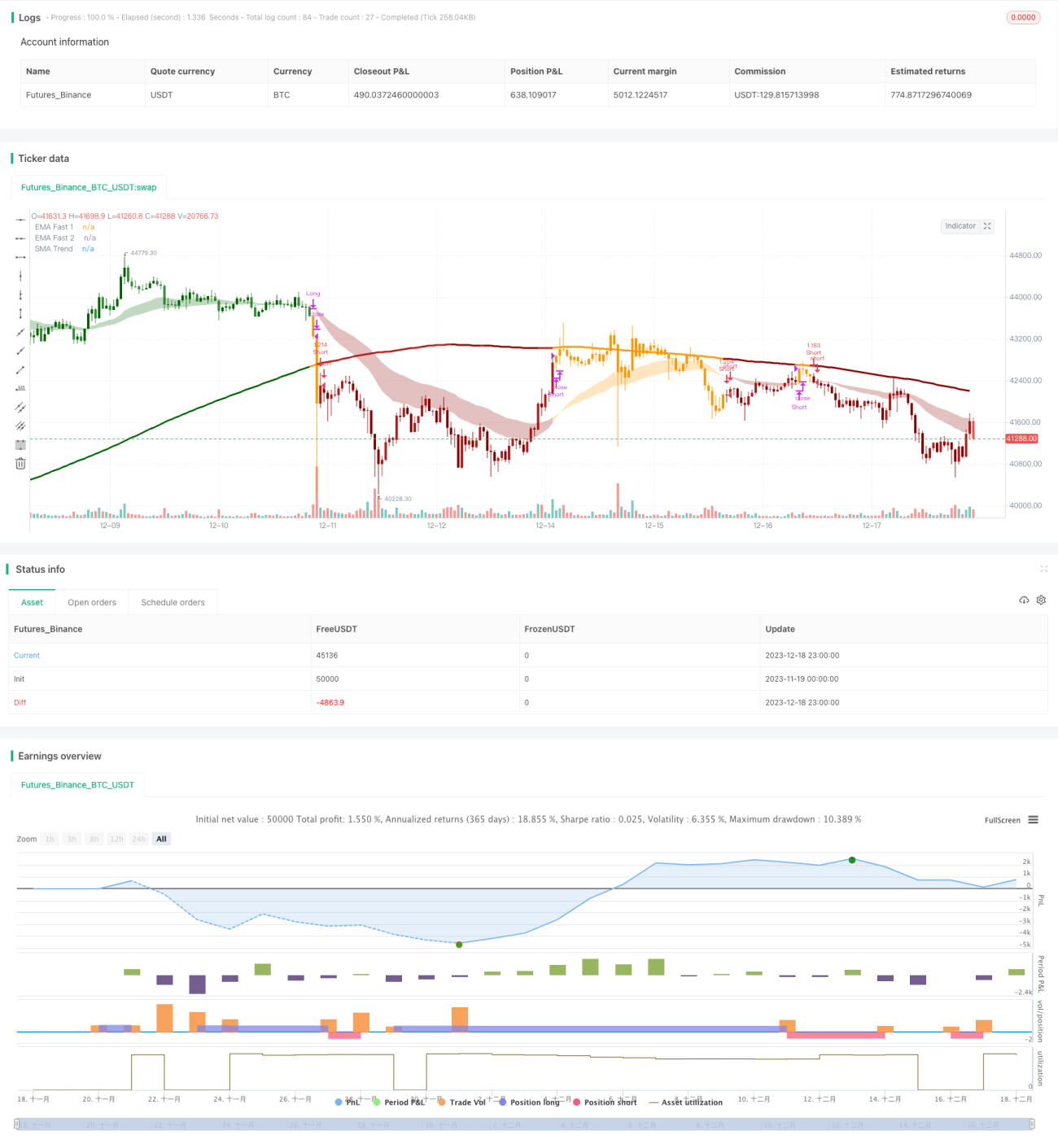

Chiến lược giao dịch định lượng kết hợp hai chỉ báo

Tổng quan

Chiến lược này kết hợp hai loại chỉ báo để xác định hướng xu hướng và thực hiện giao dịch. Đầu tiên, nó sử dụng sự giao cắt của hai đường trung bình động (đường nhanh và đường trung bình) để đánh giá xu hướng ngắn hạn; thứ hai, nó sử dụng phạm vi kênh và đường trung bình động dài hạn để xác định hướng xu hướng chính. Tín hiệu giao dịch chỉ được tạo ra khi cả hai kết quả đánh giá nhất quán. Việc kết hợp nhiều chỉ báo như vậy có thể lọc hiệu quả các tín hiệu giả, tăng tính ổn định.

Nguyên lý chiến lược

Chiến lược này sử dụng ba nhóm chỉ báo để đánh giá. Đầu tiên, giao cắt vàng/tử của đường EMA nhanh (chu kỳ 26) và đường EMA trung bình (chu kỳ 50) để đánh giá xu hướng ngắn hạn; thứ hai, tính toán phạm vi kênh, xem xét liệu giá có phá vỡ phạm vi đó hay không để đánh giá xu hướng trung hạn (tăng hay giảm); cuối cùng, tính toán đường trung bình động dài hạn SMA (chu kỳ 200), so sánh với giá để xác định hướng xu hướng chính. Tín hiệu giao dịch chỉ được phát ra khi cả ba kết quả đánh giá đều nhất quán.

Cụ thể, logic đánh giá như sau:

-

Giao cắt giữa đường nhanh và đường trung bình (giao cắt vàng = tăng, giao cắt tử = giảm) xác định hướng xu hướng ngắn hạn.

-

Giá có phá vỡ phạm vi kênh hay không xác định hướng xu hướng trung hạn. Phạm vi kênh dựa trên đường trung bình động dài hạn cộng/trừ ATR nhân với một hệ số. Nếu giá phá vỡ trên biên trên, là tín hiệu tăng; nếu phá vỡ dưới biên dưới, là tín hiệu giảm.

-

So sánh mối quan hệ giữa giá và đường trung bình động dài hạn để xác định hướng xu hướng chính.

Cuối cùng, tín hiệu giao dịch chỉ được phát ra khi cả ba đánh giá ngắn, trung, dài đều nhất quán. Phương pháp đánh giá kết hợp này có thể lọc hiệu quả các tín hiệu giả, tăng tính ổn định.

Ưu điểm của chiến lược

Chiến lược kết hợp hai chỉ báo này có một số ưu điểm:

-

Có thể lọc hiệu quả các tín hiệu giả, tăng tính ổn định. Vì tín hiệu giao dịch cần được xác nhận bởi nhiều chỉ báo ngắn, trung, dài, từ đó tránh được các tín hiệu sai do một chỉ báo đơn lẻ gây ra.

-

Tính linh hoạt cao, có thể điều chỉnh tham số chỉ báo theo thị trường. Các tham số của đường trung bình nhanh/chậm và phạm vi kênh đều có thể điều chỉnh, phù hợp với các môi trường thị trường khác nhau.

-

Kết hợp giao dịch theo xu hướng và giao dịch trong khoảng. Các chỉ báo ngắn và trung hạn bắt xu hướng, chỉ báo dài hạn xác định khoảng, nhìn chung kết hợp ưu điểm của cả chiến lược xu hướng và đảo chiều.

-

Hiệu quả sử dụng vốn cao. Chỉ đặt lệnh khi nhiều chỉ báo cùng xác nhận, có thể sử dụng vốn hiệu quả, tránh các giao dịch không cần thiết.

Rủi ro của chiến lược

Chiến lược này cũng có một số rủi ro:

-

Rủi ro cài đặt tham số. Các chu kỳ đường trung bình động và tham số phạm vi kênh cần được thiết lập hợp lý; nếu không phù hợp, có thể không phát hiện xu hướng hiệu quả hoặc tạo ra quá nhiều tín hiệu sai.

-

Hai chỉ báo làm tăng chi phí cơ hội giao dịch. So với chiến lược một chỉ báo, có thể bỏ lỡ một số cơ hội giao dịch, không thể vào và ra lệnh ở điểm tối ưu.

-

Cần thận trọng với chiến lược cắt lỗ. Cơ chế cắt lỗ khi phá vỡ trong chiến lược này có thể gây ra thua lỗ không cần thiết, cần cẩn thận đặt tỷ lệ cắt lỗ.

-

Hiệu quả có thể kém trong thị trường biến động mạnh. Chiến lược này phù hợp hơn với môi trường thị trường có xu hướng rõ rệt.

Hướng tối ưu hóa chiến lược

Chiến lược này có thể được tối ưu hóa theo các hướng sau:

-

Kiểm tra các tổ hợp tham số khác nhau để tìm tham số tối ưu. Có thể thử nghiệm trên nhiều dữ liệu lịch sử hơn để tìm ra cài đặt tham số tốt nhất.

-

Thêm cơ chế cắt lỗ thích ứng. Có thể kết hợp Chỉ báo Biến động (Volatility Indicator) để điều chỉnh biên độ cắt lỗ một cách linh hoạt.

-

Thêm chỉ báo khối lượng để hỗ trợ đánh giá. Hỗ trợ xác định quy mô vị thế tại các điểm quan trọng, tăng hiệu quả sử dụng vốn.

-

Tối ưu hóa logic vào lệnh. Cân nhắc nhiều hơn chiến lược chi phí trung bình (Cost Average) với vào lệnh theo từng phần, giảm rủi ro khi vào lệnh một lần.

-

Kết hợp mô hình học máy để đánh giá. Đưa vào các mô hình như mạng nơ-ron để đánh giá độ mạnh mẽ và độ phù hợp của mô hình.

Tổng kết

Chiến lược này thông qua ba chỉ báo (nhanh, trung, dài) và cơ chế xác nhận kép, có thể ức chế hiệu quả tín hiệu giả, tăng tính ổn định. Đồng thời, nó kết hợp ưu điểm của giao dịch theo xu hướng và giao dịch trong khoảng, hiệu quả sử dụng vốn cao. Có thể cải thiện thông qua tối ưu hóa tham số, tối ưu hóa cắt lỗ, kết hợp chỉ báo khối lượng, v.v., là một chiến lược định lượng hỗn hợp đáng được khuyến nghị.

- 1