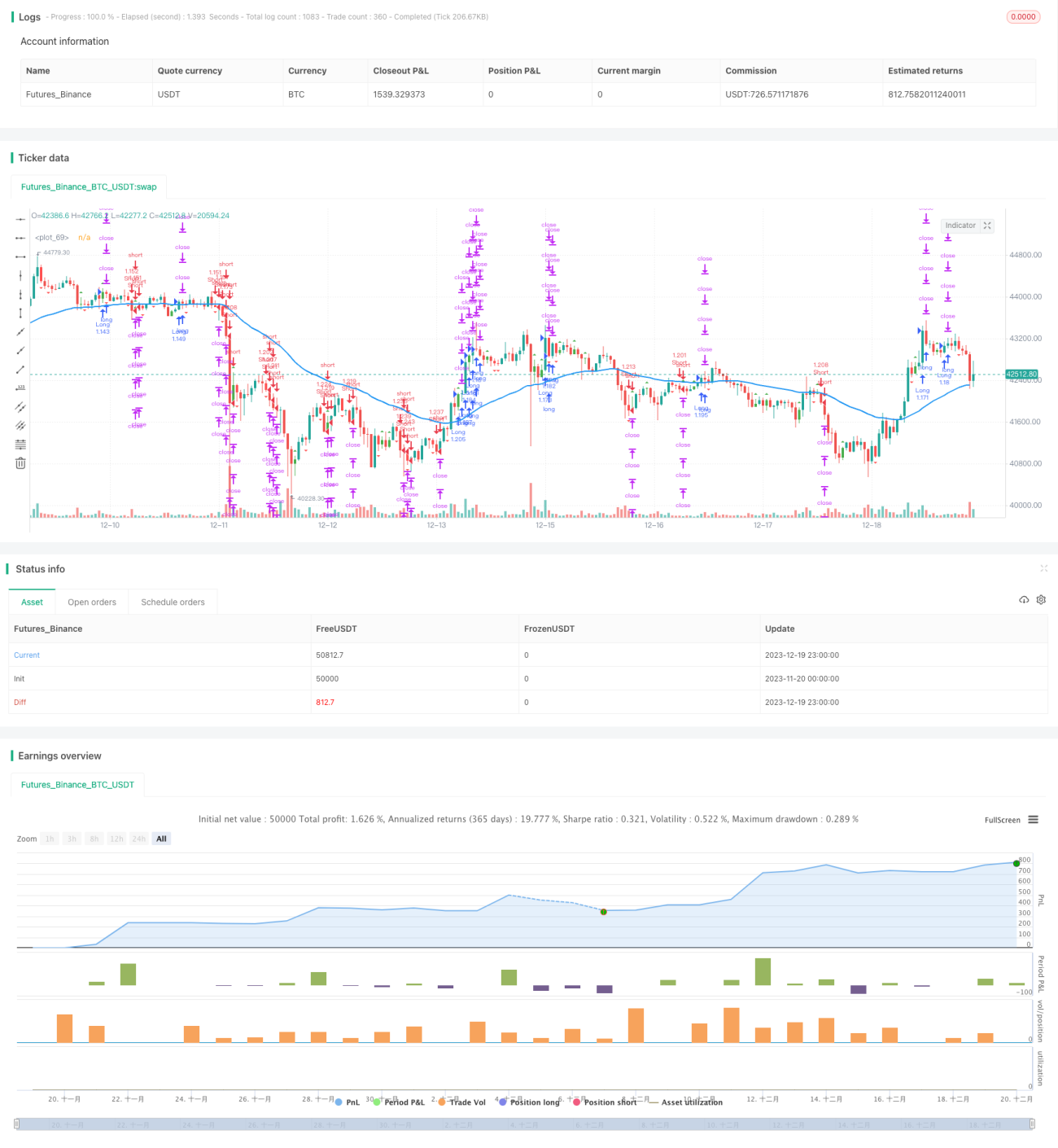

Chiến lược giao dịch định lượng tự động dựa trên đường nến nội bộ và đường trung bình động

Tổng quan

Ý tưởng cốt lõi của chiến lược này là kết hợp mô hình nến bên trong và chỉ báo đường trung bình động để thực hiện giao dịch tự động. Khi xuất hiện mô hình nến bên trong, điều này cho thấy xu hướng hiện tại có thể đảo chiều. Lúc đó, chúng ta sử dụng vị trí của đường trung bình động để xác định hướng giao dịch cuối cùng.

Nguyên lý chiến lược

-

Tìm kiếm mô hình nến bên trong. Mô hình nến bên trong là khi giá cao nhất và giá thấp nhất của một cây nến nằm trong khoảng thân nến của cây nến trước đó. Dựa vào màu sắc thân nến, chúng ta có thể xác định nến bên trong là nến bên trong tăng hay nến bên trong giảm.

-

Xác định vị trí đường trung bình động. Khi tìm thấy mô hình nến bên trong, nếu giá cao hơn đường trung bình động thì đó là tín hiệu tăng, nếu giá thấp hơn đường trung bình động thì đó là tín hiệu giảm.

-

Kết hợp mô hình nến bên trong và tín hiệu tăng/giảm từ đường trung bình động để có hướng giao dịch cuối cùng. Cụ thể: nến bên trong giảm phá vỡ xuống dưới đường trung bình thì bán khống, nến bên trong tăng phá vỡ lên trên đường trung bình thì mua lên.

Ưu điểm của chiến lược

-

Kết hợp chỉ báo kỹ thuật và mô hình giá, nâng cao độ chính xác của quyết định giao dịch.

-

Bản thân mô hình nến bên trong đã chứa tín hiệu đảo chiều giá mạnh, giúp xác định sớm điểm đảo chiều xu hướng.

-

Đường trung bình động lọc bỏ một phần nhiễu, tránh bị mắc kẹt trong vùng dao động.

-

Thực hiện giao dịch hoàn toàn tự động, giảm đáng kể thời gian và công sức giao dịch thủ công.

Rủi ro của chiến lược và cách khắc phục

-

Khi giá dao động gần đường trung bình, sẽ xuất hiện nhiều tín hiệu sai, dẫn đến giao dịch quá mức. Có thể tối ưu hóa tham số đường trung bình động hoặc thêm điều kiện lọc để giảm tín hiệu sai.

-

Chiến lược này phù hợp hơn với thị trường có xu hướng rõ ràng, hiệu quả có thể giảm trong thị trường dao động. Có thể kết hợp chỉ báo xác định xu hướng như ADX để kiểm soát việc kích hoạt thuật toán.

-

Có độ trễ thời gian nhất định. Có thể rút ngắn tham số hoặc tối ưu hóa cách tính đường trung bình động để giảm độ trễ.

-

Rủi ro drawdown lớn. Có thể đặt stop loss để kiểm soát rủi ro thua lỗ, đồng thời điều chỉnh quản lý vị thế hợp lý cũng giúp giảm drawdown.

Hướng tối ưu hóa chiến lược

-

Tối ưu hóa tham số chu kỳ xác định nến bên trong để tìm ra tổ hợp tham số tốt nhất.

-

Thử nghiệm các loại đường trung bình động khác nhau như EMA, SMA để xác định chỉ báo đường trung bình động phù hợp nhất.

-

Bổ sung các chỉ báo phụ trợ như MACD, KDJ để làm phong phú cơ sở xác định tăng/giảm, nâng cao độ chính xác của tín hiệu.

-

Thêm các chỉ báo lọc như ADX, ATR để kiểm soát môi trường kích hoạt thuật toán, tránh chạy ở thị trường không phù hợp.

-

Tối ưu hóa chiến lược quản lý vị thế như kiểm soát rủi ro vị thế, bù đắp vị thế khi mất lợi nhuận, nhằm kiểm soát rủi ro và theo đuổi lợi nhuận cao hơn.

Tổng kết

Chiến lược này bằng cách theo dõi động tín hiệu nến bên trong và chỉ báo đường trung bình động, đã xây dựng một giải pháp giao dịch định lượng hoàn toàn tự động. Tín hiệu chiến lược được tạo ra đơn giản và rõ ràng, dễ hiểu và dễ theo dõi. Hoạt động khá tốt trong thị trường có xu hướng rõ ràng. Bằng cách tối ưu hóa thêm tham số và quy tắc, có thể tăng cường độ ổn định và khả năng sinh lời của chiến lược.

- 1