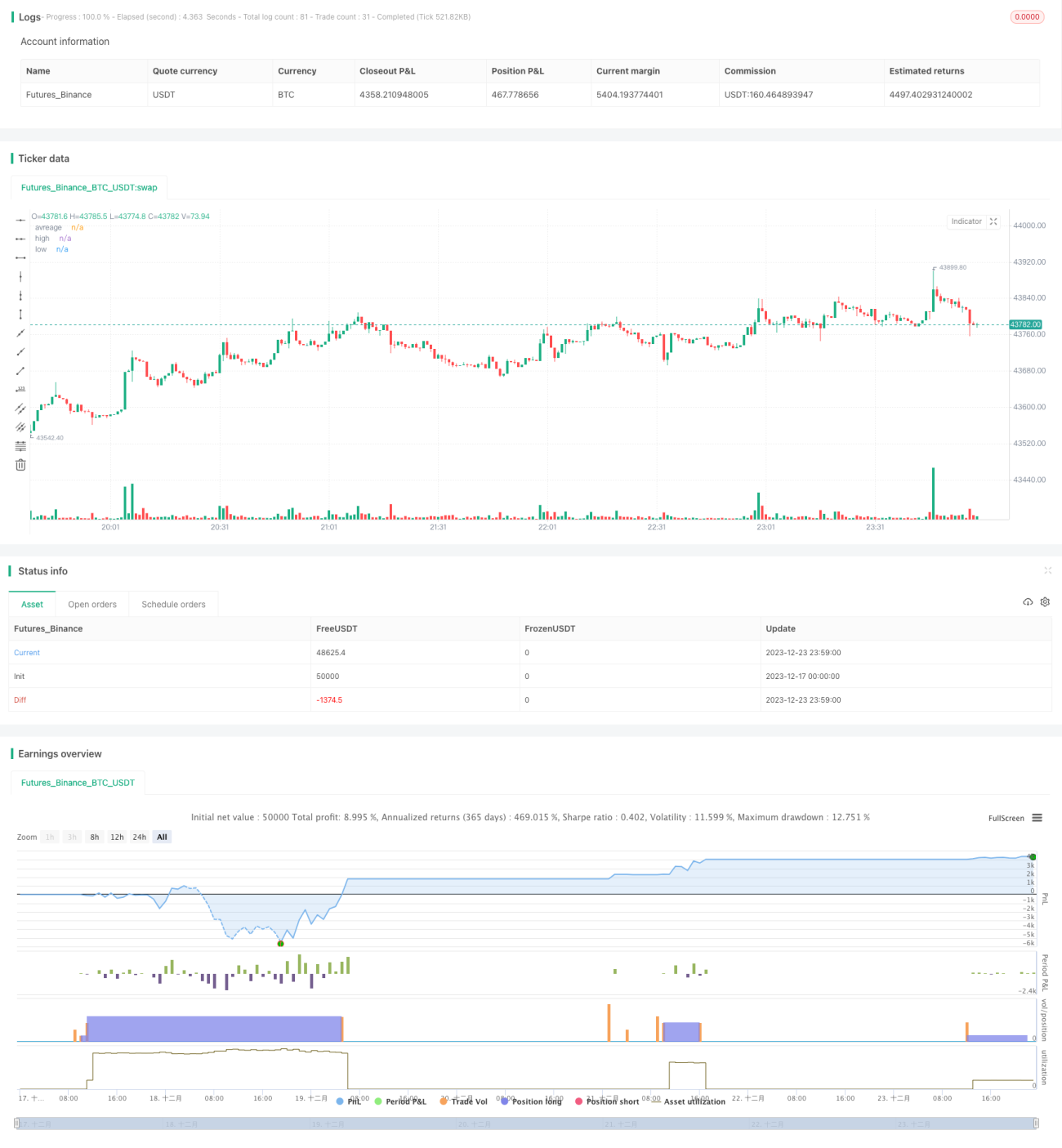

Chiến lược theo xu hướng tăng dựa trên chỉ báo RSI

Tổng quan

Chiến lược này được thiết kế dựa trên chỉ báo Relative Strength Index (RSI), là chiến lược giao dịch theo xu hướng tăng (long) mua vào khi RSI ở điểm thấp, dừng lỗ/chốt lời ở điểm cao. Tín hiệu mua được tạo ra khi chỉ báo RSI nằm dưới đường quá mua, tín hiệu bán được tạo ra khi chỉ báo RSI nằm trên đường quá bán. Chiến lược tối ưu hóa hiệu suất bám theo xu hướng, có thể kiểm soát rủi ro giao dịch một cách hiệu quả.

Nguyên lý chiến lược

Chiến lược sử dụng chỉ báo RSI để đánh giá giá cổ phiếu có bị đánh giá quá cao hay quá thấp. Chỉ báo RSI kết hợp với các đường quá mua và quá bán để hình thành tín hiệu mua và bán. Cụ thể, nếu chỉ báo RSI cắt lên trên đường quá bán 20, tạo tín hiệu mua; nếu chỉ báo RSI cắt xuống dưới đường quá mua 80, tạo tín hiệu bán.

Sau khi vào lệnh mua (long), chiến lược thiết lập một đường dừng lỗ ban đầu để kiểm soát rủi ro giảm giá. Đồng thời thiết lập hai đường chốt lời với tỷ lệ khác nhau, chốt lời từng phần để khóa lợi nhuận. Cụ thể, trước tiên chốt lời 50% vị thế với giá chốt lời bằng 3% giá mua; sau đó chốt lời 50% vị thế còn lại với giá chốt lời bằng 5% giá mua.

Chiến lược sử dụng chỉ báo RSI một cách đơn giản và hiệu quả để xác định thời điểm vào thị trường. Các cài đặt chốt lời và dừng lỗ hợp lý, có thể kiểm soát rủi ro hiệu quả.

Ưu điểm chiến lược

- Sử dụng chỉ báo RSI để xác định xu hướng tăng/giảm, tránh mua lung tung

- Tham số chỉ báo RSI được tối ưu hóa, hiệu quả chỉ báo tốt hơn

- Thiết kế hai mức chốt lời hợp lý, có thể chốt lời từng phần, khóa được nhiều lợi nhuận hơn

- Dừng lỗ ban đầu và dừng lỗ liên tiếp ngăn chặn thua lỗ lớn

Phân tích rủi ro

- Chiến lược long, hiệu quả kém trong thị trường tăng không liên tục

- Tồn tại xác suất chỉ báo RSI phát tín hiệu sai, đánh giá tín hiệu không đúng có thể làm tăng tổn thất

- Điểm dừng lỗ quá sâu gây rủi ro không thể dừng lỗ

- Thiếu giới hạn về số lần và tỷ lệ thêm vị thế, có thể dẫn đến khuếch đại thua lỗ

Hướng tối ưu hóa

- Kết hợp với các chỉ báo khác để lọc tín hiệu RSI, nâng cao độ chính xác của tín hiệu

- Thêm giới hạn về số lần và tỷ lệ thêm vị thế

- Kiểm tra hiệu quả của các tham số RSI khác nhau

- Tối ưu hóa điểm dừng lỗ và chốt lời, giảm rủi ro

Tổng kết

Chiến lược sử dụng chỉ báo RSI để đánh giá thị trường, cài đặt chốt lời và dừng lỗ hợp lý. Có thể đánh giá xu hướng thị trường hiệu quả, kiểm soát rủi ro giao dịch, phù hợp để sử dụng làm chiến lược bám đuổi xu hướng tăng. Thông qua lọc tín hiệu, kiểm tra tham số, tối ưu hóa dừng lỗ,... có thể nâng cao hơn nữa độ ổn định của chiến lược.

- 1