Chiến lược đột phá biến động khối lượng mua bán động

1

Follow

1802

Followers

Tổng quan

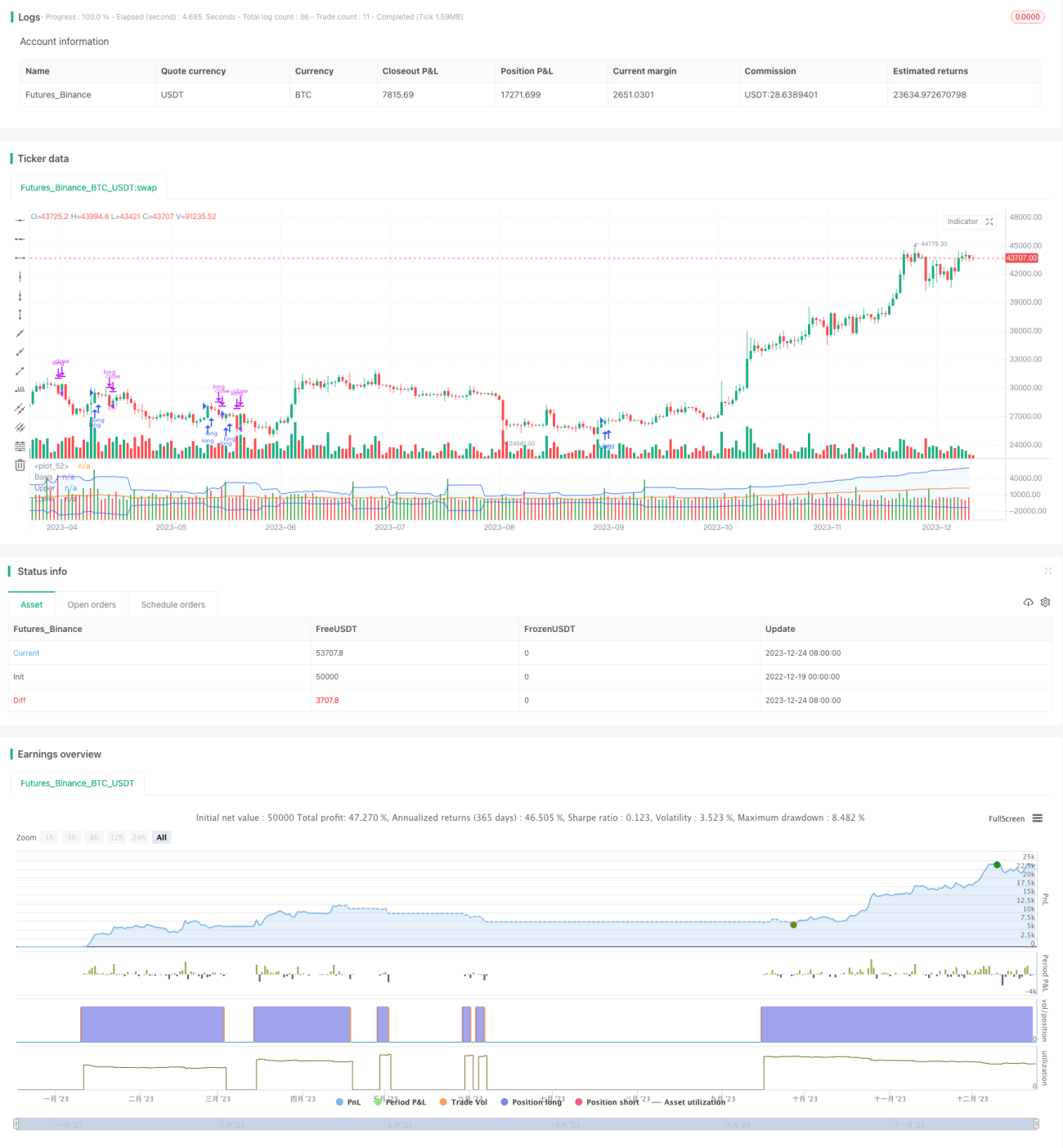

Chiến lược này sử dụng khối lượng mua bán trong khung thời gian tùy chỉnh để xác định xu hướng tăng giảm, kết hợp với VWAP tuần và Bollinger Bands để lọc, nhằm theo dõi xu hướng với xác suất cao. Đồng thời, cơ chế chốt lời cắt lỗ động được áp dụng, giúp kiểm soát hiệu quả rủi ro một chiều.

Nguyên lý chiến lược

- Tính toán chỉ số khối lượng mua bán trong khung thời gian tùy chỉnh

- BV: Khối lượng mua – khối lượng phát sinh từ việc mua tại đáy

- SV: Khối lượng bán – khối lượng phát sinh từ việc bán tại đỉnh

- Xử lý khối lượng mua bán

- Làm mượt bằng EMA 20 chu kỳ

- Tách riêng phần dương và âm của khối lượng mua bán đã xử lý

- Xác định hướng chỉ báo

- Chỉ báo lớn hơn 0 là tín hiệu tăng, nhỏ hơn 0 là tín hiệu giảm

- Kết hợp VWAP tuần và Bollinger Bands để xác định phân kỳ

- Giá nằm trên VWAP và chỉ báo tăng → tín hiệu mua

- Giá nằm dưới VWAP và chỉ báo giảm → tín hiệu bán

- Chốt lời cắt lỗ động

- Đặt tỷ lệ chốt lời cắt lỗ theo ATR ngày

Ưu điểm chiến lược

- Khối lượng mua bán phản ánh động lực thực tế của thị trường, nắm bắt năng lượng tiềm ẩn của xu hướng

- VWAP tuần xác định hướng xu hướng lớn, Bollinger Bands xác định tín hiệu bứt phá

- ATR động giúp chốt lời cắt lỗ tối đa hóa lợi nhuận, tránh overshoot

Rủi ro chiến lược

- Dữ liệu khối lượng mua bán có sai số nhất định, có thể dẫn đến phán đoán sai

- Kết hợp chỉ một chỉ báo dễ tạo ra tín hiệu nhiễu

- Cài đặt tham số Bollinger Bands không phù hợp có thể thu hẹp các đợt bứt phá hiệu quả

Hướng tối ưu chiến lược

- Tối ưu chỉ số khối lượng mua bán trên nhiều khung thời gian

- Bổ sung các chỉ báo phụ trợ như khối lượng giao dịch để lọc tín hiệu

- Điều chỉnh tham số Bollinger Bands động, nâng cao hiệu quả bứt phá

Tổng kết

Chiến lược này tận dụng khả năng dự báo của khối lượng mua bán, kết hợp VWAP và Bollinger Bands để tạo ra tín hiệu xác suất cao, kiểm soát rủi ro hiệu quả thông qua chốt lời cắt lỗ động. Đây là một chiến lược giao dịch định lượng hiệu quả và ổn định. Với việc liên tục tối ưu tham số và quy tắc, hiệu quả dự kiến sẽ càng rõ rệt hơn.

Source

Pine

/*backtest

start: 2022-12-19 00:00:00

end: 2023-12-25 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © original author ceyhun

//@ exlux99 update

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1