Chiến lược giao dịch theo xu hướng dựa trên Average True Range

Tổng quan

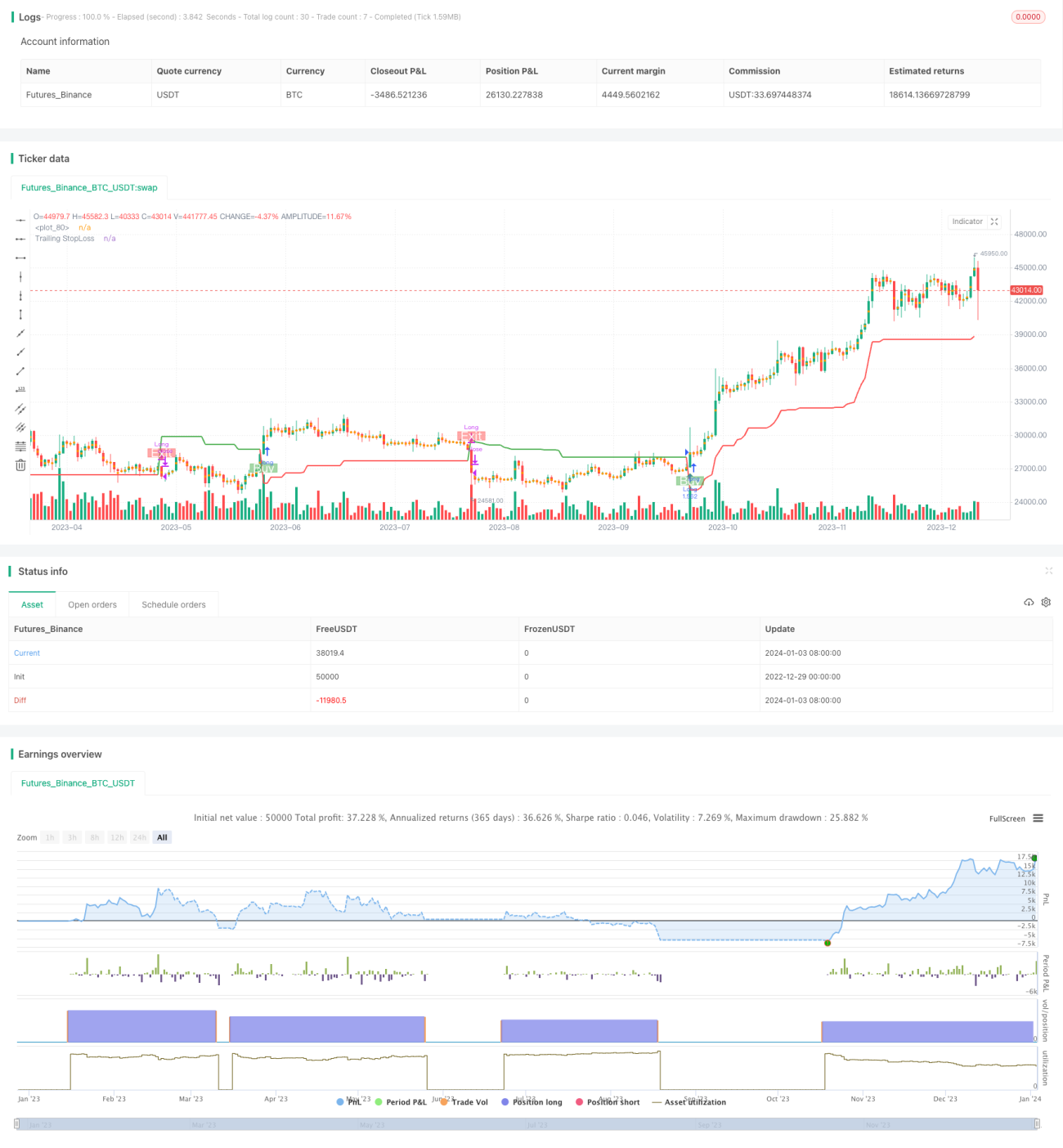

Chiến lược này là một chiến lược giao dịch theo xu hướng dựa trên Chỉ báo Biến động Trung bình Thực (ATR). Nó sử dụng ATR để tính toán các giá trị chỉ báo, từ đó xác định hướng của xu hướng giá. Chiến lược cũng cung cấp cơ chế cắt lỗ để kiểm soát rủi ro.

Nguyên lý chiến lược

Chiến lược này sử dụng ba tham số chính: Chu kỳ (Period), Hệ số nhân (Multiplier) và Điểm vào/ra (Entry/Exit Point). Tham số mặc định là chu kỳ ATR 14 và hệ số nhân 4.

Đầu tiên, chiến lược tính giá trung bình vị thế mua (buyavg) và giá trung bình vị thế bán (sellavg), sau đó so sánh giá với hai mức giá trung bình này để xác định hướng xu hướng hiện tại. Nếu giá cao hơn giá trung bình vị thế bán, thì đó là xu hướng tăng; nếu giá thấp hơn giá trung bình vị thế mua, thì đó là xu hướng giảm.

Ngoài ra, chiến lược này kết hợp ATR để thiết lập lệnh dừng lỗ động (Trailing Stop Loss). Cụ thể: sử dụng đường trung bình động gia quyền 14 chu kỳ của ATR nhân với một hệ số nhân (mặc định là 4) làm khoảng cách dừng lỗ. Bằng cách này, khoảng cách dừng lỗ có thể được điều chỉnh linh hoạt theo mức độ biến động của thị trường.

Khi lệnh dừng lỗ bị kích hoạt, chiến lược sẽ đóng vị thế để chốt lợi nhuận.

Ưu điểm của chiến lược

- Dựa trên phán đoán xu hướng, có thể đi theo xu hướng để kiếm lợi nhuận liên tục.

- Sử dụng ATR để điều chỉnh khoảng cách dừng lỗ động, kiểm soát rủi ro hiệu quả.

- Cách tính điểm mua/bán đơn giản, trực tiếp, dễ hiểu và dễ thực hiện.

Rủi ro và biện pháp đối phó

- Khi xu hướng đảo chiều, có thể xảy ra thua lỗ lớn.

- Điều chỉnh chu kỳ ATR và hệ số nhân một cách thích hợp để tối ưu hóa khoảng cách dừng lỗ.

- Trong thị trường đi ngang, sẽ phát sinh nhiều khoản lỗ nhỏ.

- Thêm các bộ lọc để tránh giao dịch trong thị trường đi ngang.

- Tham số cài đặt không phù hợp có thể khiến chiến lược kém hiệu quả.

- Thực hiện tối ưu hóa đa tổ hợp tham số để tìm ra tham số tốt nhất.

Hướng tối ưu hóa chiến lược

- Thêm các chỉ báo khác để lọc tín hiệu, tránh vào lệnh trong thị trường đi ngang.

- Tối ưu hóa tham số chu kỳ ATR và hệ số nhân để khoảng cách dừng lỗ hợp lý hơn.

- Thêm kiểm soát khối lượng vị thế khi mở lệnh, điều chỉnh kích thước vị thế theo tình hình thị trường.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược giao dịch theo xu hướng đơn giản và thực tế. Nó chỉ cần một vài tham số để thực hiện, sử dụng ATR để điều chỉnh dừng lỗ động nhằm kiểm soát rủi ro hiệu quả. Nếu kết hợp với các chỉ báo hỗ trợ khác, nó có thể được tối ưu hóa thêm để lọc bớt các tín hiệu nhiễu. Nhìn chung, chiến lược này phù hợp với những người muốn học giao dịch theo xu hướng, đồng thời cũng có thể được sử dụng như một thành phần cơ bản cho các chiến lược nâng cao hơn.

/*backtest

start: 2022-12-29 00:00:00

end: 2024-01-04 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('Trend Strategy by zdmre', shorttitle='Trend Strategy', overlay=true, pyramiding=0, currency=currency.USD, default_qty_type=strategy.percent_of_equity, initial_capital=10000, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.005)

show_STOPLOSSprice = input(true, title='Show TrailingSTOP Prices')

src = input(close, title='Source')- 1