Chiến lược theo xu hướng đường trung bình động dựa trên SSL

Tổng quan

Chiến lược này là một chiến lược sử dụng chỉ báo SSL Channel để xác định xu hướng thị trường và dựa trên đường trung bình động để bám theo xu hướng. Nó phù hợp với khung thời gian 4 giờ và ngày cho giao dịch trung và dài hạn.

Nguyên lý chiến lược

-

Kênh SSL được tạo thành từ đường trung bình động Jurik và biên độ thực. Nó có thể xác định hướng xu hướng thị trường. Khi giá phá vỡ dải trên là tín hiệu tăng, phá vỡ dải dưới là tín hiệu giảm.

-

Chiến lược sử dụng các chỉ báo đường trung bình động như EMA để tính toán một đường trung bình động cơ sở. Đường trung bình này có thể lọc bớt một số tín hiệu phá vỡ giả.

-

Chiến lược sẽ mua (Long) khi giá phá vỡ dải trên của SSL, và bán (Short) khi giá phá vỡ dải dưới của SSL. Trong xu hướng tăng, nó mua đuổi tăng; trong xu hướng giảm, nó bắt đáy rơi dao.

-

Các phương thức cắt lỗ bao gồm: cắt lỗ theo phần trăm, cắt lỗ theo ATR và cắt lỗ theo mức giá thấp nhất/cao nhất trong quá khứ. Chốt lời là N lần mức cắt lỗ. Các tham số cụ thể do người dùng xác định.

Phân tích ưu điểm

-

Kênh SSL xác định hướng xu hướng chính xác, giảm tín hiệu giả. Kết hợp với đường trung bình động làm cơ sở vào lệnh, tránh mua đỉnh bán đáy.

-

Có thể linh hoạt lựa chọn các loại đường trung bình động khác nhau, thích ứng với nhiều điều kiện thị trường.

-

Phương thức cắt lỗ linh hoạt và đa dạng, kiểm soát được rủi ro. Hệ số chốt lời cũng có thể được thiết lập linh hoạt, đáp ứng các sở thích khác nhau.

-

Có thể đồng thời mua và bán, khai thác triệt để các cơ hội hai chiều của thị trường.

Phân tích rủi ro

-

Các chỉ báo đường trung bình động đều có độ trễ, có thể dẫn đến tích lũy thua lỗ.

-

Trong thị trường dao động (sideway), vừa phá vỡ dải trên/dưới sẽ có sự đảo chiều, dễ bị kẹt lệnh.

-

Cắt lỗ theo ATR và theo mức giá quá khứ có thể quá rộng trong các đột phá bất thường, làm gia tăng thua lỗ.

Biện pháp đối phó rủi ro:

- Điều chỉnh tham số đường trung bình động phù hợp, hoặc chọn loại đường trung bình động khác.

- Mở rộng biên độ cắt lỗ, cắt lỗ kịp thời.

- Thêm hệ số nhân vào ATR, hoặc điều chỉnh chu kỳ nhìn lại.

Hướng tối ưu hóa

- Kiểm tra nhiều loại chỉ báo đường trung bình động hơn, tìm tham số tốt nhất.

- Tối ưu tham số chu kỳ ATR cho cắt lỗ.

- Kiểm tra các tham số hệ số nhân cắt lỗ khác nhau.

- Kiểm tra các hệ số rủi ro chốt lời khác nhau.

Kết luận

Chiến lược này kết hợp sử dụng SSL để xác định xu hướng và chỉ báo đường trung bình động để xác nhận vào lệnh, có thể bám theo xu hướng hiệu quả. Nó cung cấp các phương thức cắt lỗ và chốt lời linh hoạt, vừa kiểm soát rủi ro vừa thu được lợi nhuận cao hơn. Thông qua việc liên tục kiểm tra và tối ưu hóa các tham số, có thể đạt được hiệu suất giao dịch tốt hơn. Đây là một chiến lược hiệu quả đáng để theo dõi và sử dụng lâu dài.

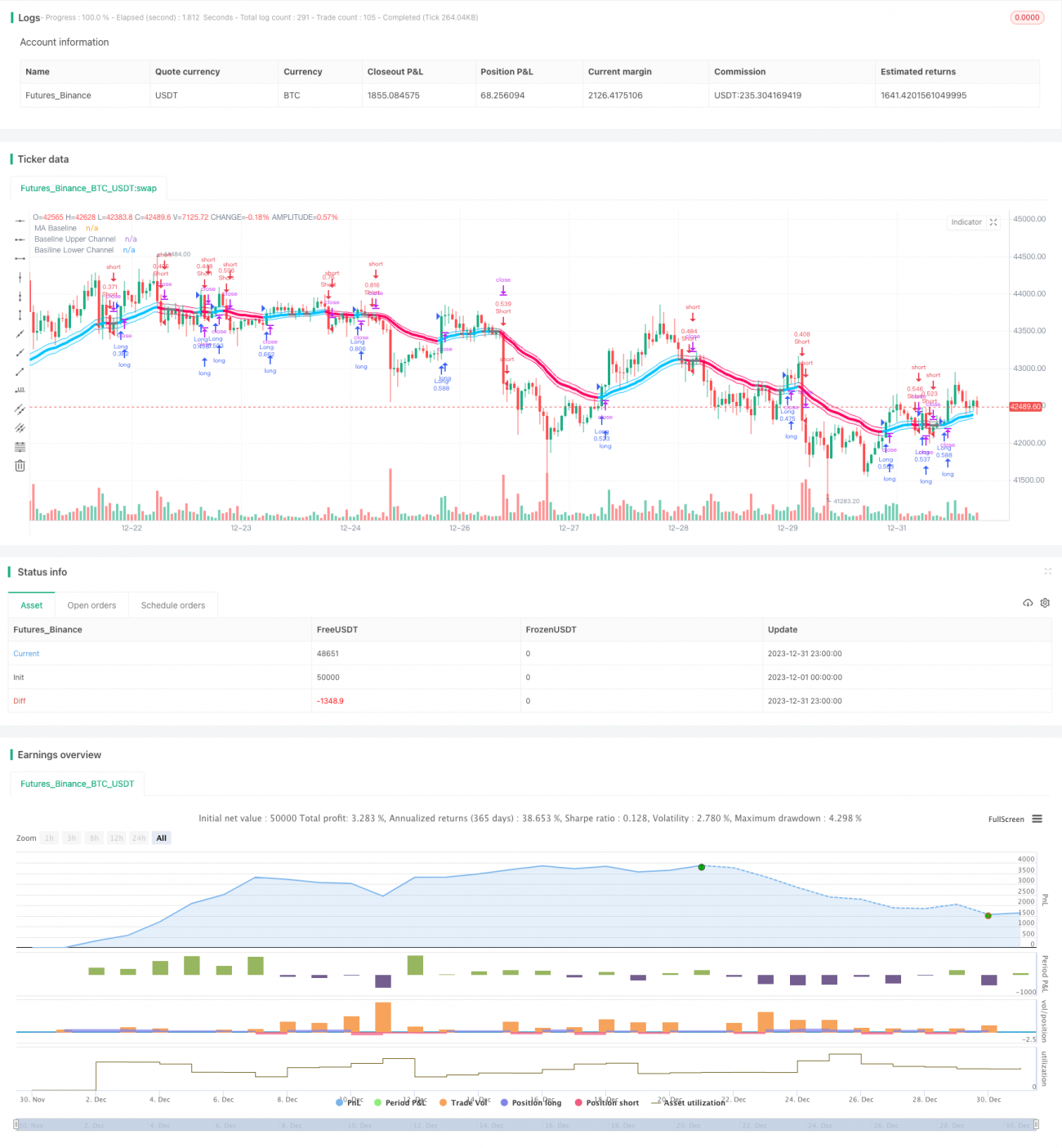

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// Thanks to @kevinmck100 for opensource strategy template and @Mihkel00 for SSL Hybrid

// @fpemehd

// @version=5- 1