Chiến lược chênh lệch giá hai chiều dựa trên chỉ báo TSI và HMACCI

Tổng quan

Chiến lược này kết hợp tín hiệu giao dịch hai chiều của chỉ báo TSI và chỉ báo CCI cải tiến, sử dụng phương pháp arbitrage để thường xuyên mở và đóng vị thế, nhằm theo đuổi lợi nhuận ổn định và liên tục hơn. Logic chính là dựa trên giao cắt vàng và tử thần giữa đường trung bình nhanh và chậm của chỉ báo TSI, kết hợp với đường tín hiệu đa chiều của chỉ báo HMACCI để xác định hướng mua bán trên thị trường. Rủi ro được kiểm soát bằng cách giới hạn điều kiện mở vị thế, đồng thời thiết lập logic cắt lỗ và chốt lời.

Nguyên lý chiến lược

Chiến lược này chủ yếu dựa trên sự kết hợp của hai chỉ báo TSI và HMACCI.

Chỉ báo TSI bao gồm một đường trung bình nhanh và một đường trung bình chậm, dùng để xác định tín hiệu mua bán. Khi đường nhanh vượt lên trên đường chậm từ dưới lên, đó là tín hiệu mua; ngược lại là tín hiệu bán. Điều này cho phép nắm bắt nhạy bén các xu hướng thay đổi của thị trường.

Chỉ báo HMACCI sử dụng đường trung bình Hull thay thế cho giá trong chỉ báo CCI truyền thống, giúp lọc bỏ phần nào nhiễu và xác định vùng quá mua/quá bán. Vùng quá mua/quá bán có thể xác nhận lại hướng tín hiệu của chỉ báo TSI.

Logic chính của chiến lược là kết hợp kết quả từ hai chỉ báo này, đồng thời thiết lập một số điều kiện bổ sung để lọc tín hiệu sai, chẳng hạn như xem xét giá đóng cửa của nến trước đó và giá cao nhất/thấp nhất cách đây nhiều chu kỳ, nhằm kiểm soát chất lượng tín hiệu đảo chiều.

Về mở vị thế, nếu điều kiện thỏa mãn, tại thời điểm đóng cửa mỗi nến, sẽ mở vị thế theo giá thị trường, đồng thời mua và bán cùng lúc. Điều này mang lại lợi nhuận ổn định hơn nhưng phải chấp nhận rủi ro arbitrage.

Về chốt lời và cắt lỗ, thiết lập cắt lỗ thả nổi và đóng toàn bộ vị thế khi có lợi nhuận. Điều này giúp kiểm soát tốt rủi ro giao dịch một chiều.

Lợi thế của chiến lược

Đây là một chiến lược arbitrage tần suất cao tương đối ổn định và đáng tin cậy. Các lợi thế chính:

- Kết hợp hai chỉ báo giúp tránh được tín hiệu sai hiệu quả.

- Mở vị thế mỗi nến, thao tác arbitrage thường xuyên, biến động lợi nhuận ổn định hơn.

- Logic mở vị thế và điều kiện cắt lỗ chặt chẽ, có thể kiểm soát rủi ro.

- Kết hợp nhận định xu hướng và đảo chiều, khả năng chịu lỗi cao.

- Không thiên vị hướng, phù hợp với nhiều loại thị trường.

- Tham số có thể điều chỉnh linh hoạt, có thể tối ưu hóa cho từng sản phẩm khác nhau.

Phân tích rủi ro

Các rủi ro chính cần lưu ý:

- Chi phí hoa hồng cao hơn do giao dịch tần suất cao.

- Không thể tránh hoàn toàn khả năng bị kẹt trong arbitrage.

- Thiết lập tham số không phù hợp có thể dẫn đến vào lệnh quá hung hăng.

- Khó chịu đựng được khoản lỗ lớn một chiều trong ngắn hạn.

Có thể giảm rủi ro bằng các cách sau:

- Điều chỉnh tần suất mở vị thế phù hợp, giảm tác động của phí giao dịch.

- Tối ưu hóa tham số chỉ báo để đảm bảo chất lượng tín hiệu.

- Tăng biên độ cắt lỗ, nhưng sẽ chịu nhiều tổn thất arbitrage hơn.

- Kiểm tra thiết lập tham số trên các sản phẩm khác nhau.

Hướng tối ưu hóa

Chiến lược này vẫn còn nhiều dư địa để tối ưu hóa, các hướng chính:

- Tối ưu hóa và thử nghiệm các tham số như chu kỳ, độ dài, v.v.

- Thử nghiệm các tổ hợp chỉ báo khác như MACD, BOLL, v.v.

- Sửa đổi logic mở vị thế, thiết lập điều kiện lọc chặt chẽ hơn.

- Tối ưu hóa chiến lược chốt lời/cắt lỗ, thực hiện cắt lỗ động và đột phá.

- Thử nghiệm phương pháp học máy để tìm ra phạm vi tham số ổn định hơn.

- Thử nghiệm trên các sản phẩm và khung thời gian giao dịch khác nhau.

- Kết hợp các chỉ báo nhận định xu hướng để tránh vào ra quá mức trong thị trường đi ngang.

Tổng kết

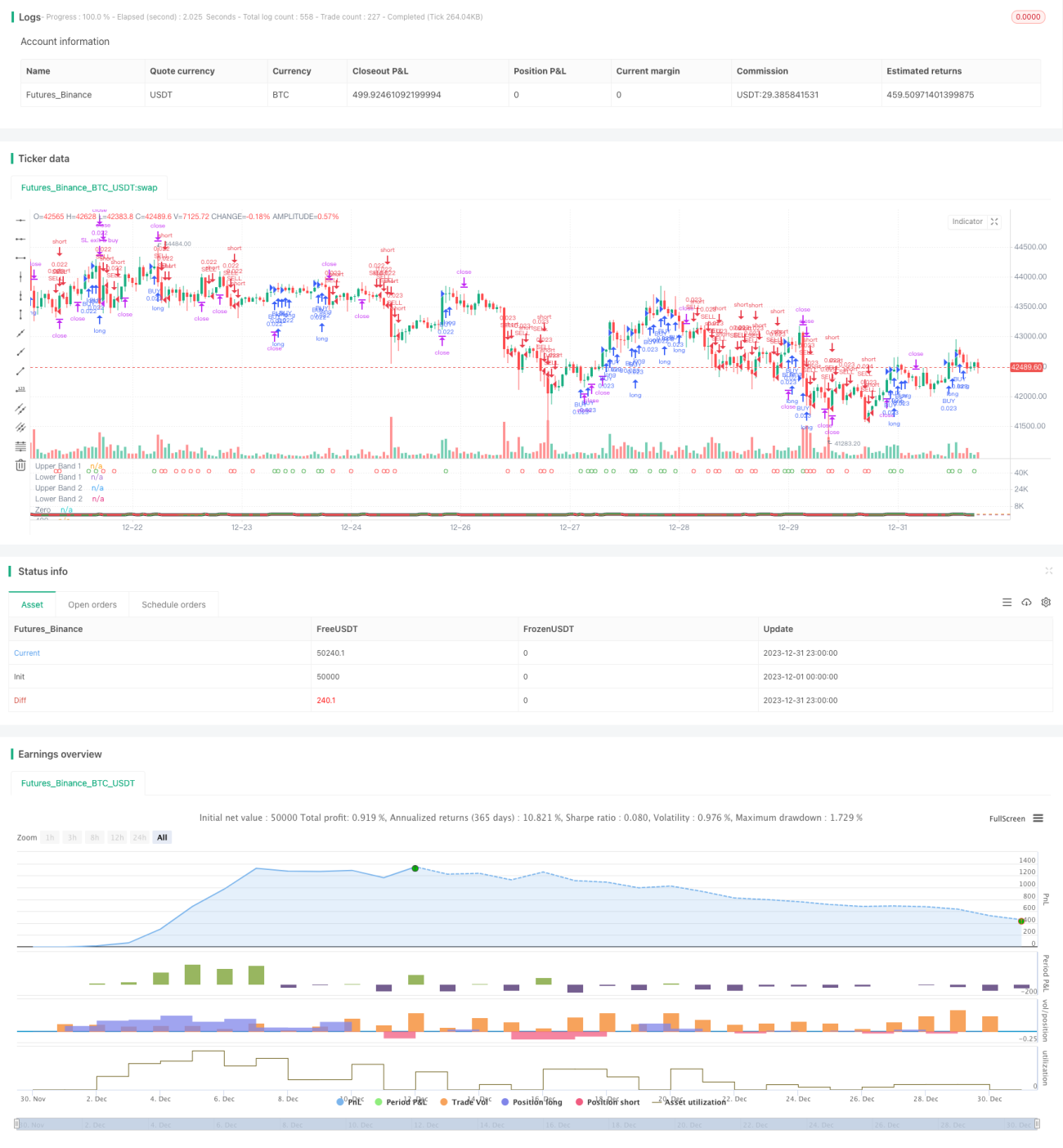

Nhìn chung, chiến lược này là một chiến lược arbitrage hai chiều ổn định, đáng tin cậy, có khả năng chịu lỗi cao. Nó kết hợp nhận định xu hướng và chỉ báo đảo chiều, thu được lợi nhuận ổn định thông qua việc mở vị thế hai chiều thường xuyên. Đồng thời, bản thân chiến lược có không gian và tiềm năng tối ưu hóa mạnh mẽ, là một ý tưởng giao dịch tần suất cao đáng để nghiên cứu sâu.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the suns bipolarity

//©SeaSide420

//@version=4

strategy(title="TSI HMA CCI", default_qty_type=strategy.cash,default_qty_value=1000,commission_type=strategy.commission.percent,commission_value=0.001)- 1