Chiến lược chỉ báo MoFei xuyên thời gian

Tổng quan

Đây là một chiến lược định lượng đơn giản sử dụng chỉ báo Moffi để nhận diện "cá mập lớn" trên thị trường. Chiến lược này áp dụng cho khung thời gian 5 phút, chủ yếu dùng cho giao dịch tiền điện tử.

Nguyên lý chiến lược

Chiến lược sử dụng chỉ báo Moffi có độ dài 3, đặt đường quá mua ở mức 100 và đường quá bán ở mức 0. Chiến lược chờ chỉ báo Moffi đạt đến mức quá mua, cho thấy sự hiện diện của "cá mập lớn" trên thị trường. Nếu trong ngày, hai điểm quá mua đầu tiên của chỉ báo Moffi mà giá vẫn giữ được xu hướng tăng, thì đó là tín hiệu vào lệnh mua.

Khi chỉ báo Moffi = 100 và nến tiếp theo là nến tăng lớn, vào lệnh mua. Đặt stop loss tại mức thấp nhất của ngày giao dịch đó, chốt lời trong vòng 60 phút sau khi vào lệnh.

Đối với bán khống, có thể sử dụng logic đối xứng. Tức là khi chỉ báo Moffi đạt mức quá bán và nến tiếp theo là nến giảm lớn, vào lệnh bán.

Ưu điểm chiến lược

-

Sử dụng chỉ báo Moffi có thể nhận diện hiệu quả hành vi tích lũy cổ phiếu tiềm năng của "cá mập lớn", những cổ phiếu này có khả năng tiếp tục tăng.

-

Tận dụng thân nến thực để nhận diện các điểm phá vỡ có lực mạnh, giúp lọc bỏ nhiều tín hiệu phá vỡ giả.

-

Kết hợp bộ lọc SMA, tránh mua cổ phiếu đang trong xu hướng giảm, giảm thiểu rủi ro giao dịch.

-

Sử dụng phương pháp giao dịch siêu ngắn trong ngày, chốt lời sau 60 phút giúp nhanh chóng khóa lợi nhuận, giảm xác suất sụt giảm.

Rủi ro chiến lược

-

Chỉ báo Moffi có thể tạo ra tín hiệu giả, dẫn đến thua lỗ không cần thiết. Có thể điều chỉnh tham số phù hợp hoặc thêm các chỉ báo khác để lọc.

-

Phương pháp giao dịch siêu ngắn 60 phút có thể quá mạnh, không phù hợp với các cổ phiếu có độ biến động cao. Có thể điều chỉnh thời gian chốt lời hoặc sử dụng stop loss động để tối ưu.

-

Chưa tính đến rủi ro tác động thị trường khi xảy ra các sự kiện kinh tế vĩ mô quan trọng. Khi đó nên tạm dừng chiến lược, chờ thị trường ổn định trở lại mới tiếp tục giao dịch.

Hướng tối ưu hóa chiến lược

-

Có thể thử nghiệm các tổ hợp tham số khác nhau, như điều chỉnh độ dài của chỉ báo Moffi, tối ưu chu kỳ SMA, v.v.

-

Thử thêm các chỉ báo khác kết hợp, như dải Bollinger, chỉ báo KD, xem có cải thiện độ chính xác tín hiệu không.

-

Thử nghiệm nới lỏng biên độ stop loss để xem liệu có thể thu được lợi nhuận đơn lẻ lớn hơn không.

-

Thử phát triển các phiên bản cho khung thời gian khác dựa trên khung chiến lược này, như phiên bản 15 phút hoặc 30 phút.

Kết luận

Nhìn chung, chiến lược này rất đơn giản và dễ hiểu, ý tưởng cơ bản tương tự chiến lược theo dõi "cá mập lớn" kinh điển. Bằng cách nhận diện các điểm quá mua/quá bán của chỉ báo Moffi kết hợp với sàng lọc thân nến thực, có thể lọc được nhiều nhiễu. Việc thêm bộ lọc SMA cũng giúp tăng tính ổn định của chiến lược.

Phương pháp giao dịch siêu ngắn 60 phút có thể thu lợi nhanh, nhưng cũng mang lại rủi ro giao dịch cao hơn. Nhìn chung, đây là một mẫu chiến lược định lượng có giá trị thực tiễn cao, đáng để nghiên cứu và tối ưu hóa chuyên sâu, đồng thời cung cấp cho chúng ta những ý tưởng phát triển chiến lược quý giá.

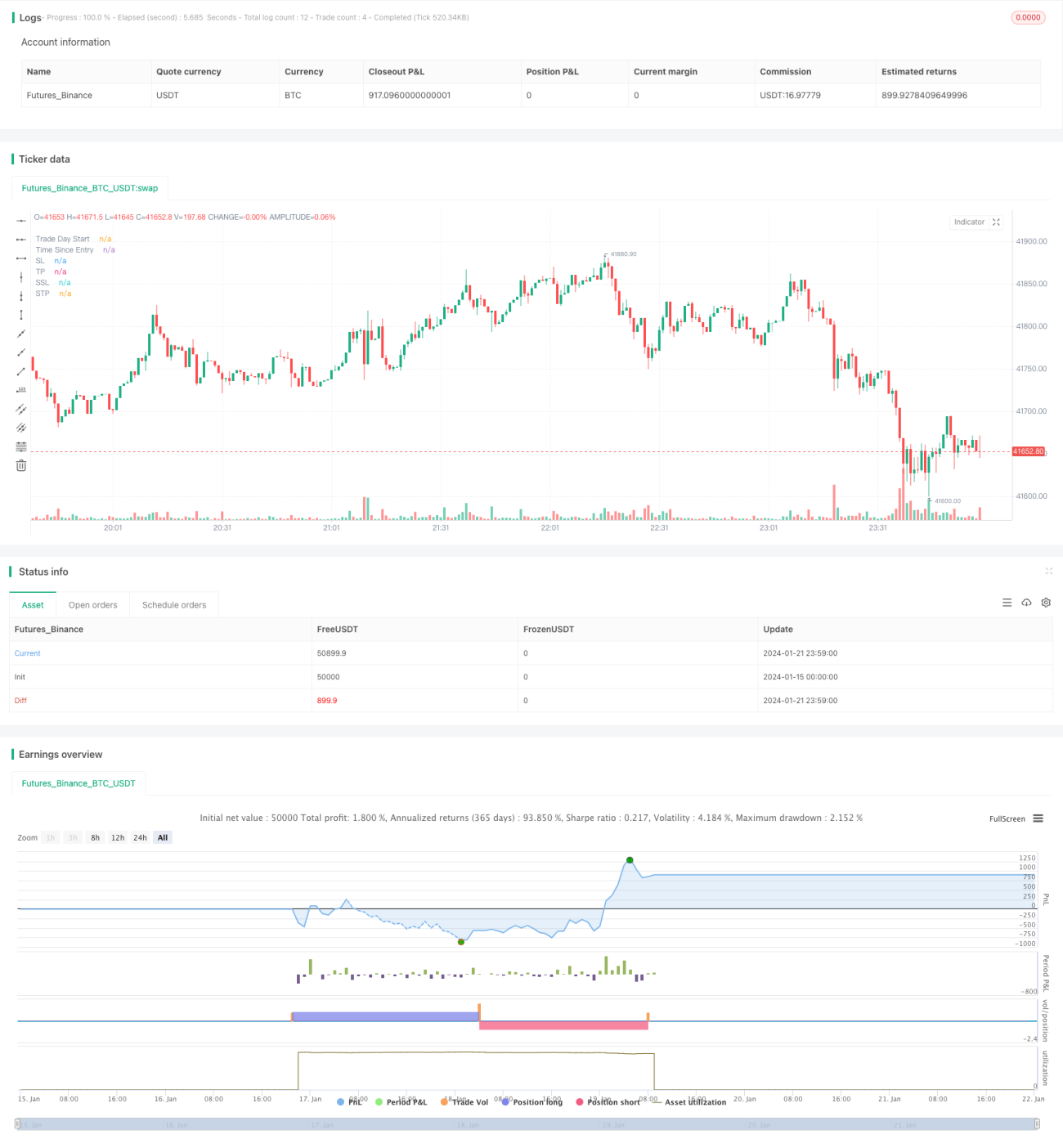

/*backtest

start: 2024-01-15 00:00:00

end: 2024-01-22 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// From "Crypto Day Trading Strategy" PDF file.

- 1