Chiến lược theo dõi xu hướng kênh giá đường trung bình động kép

Tổng quan

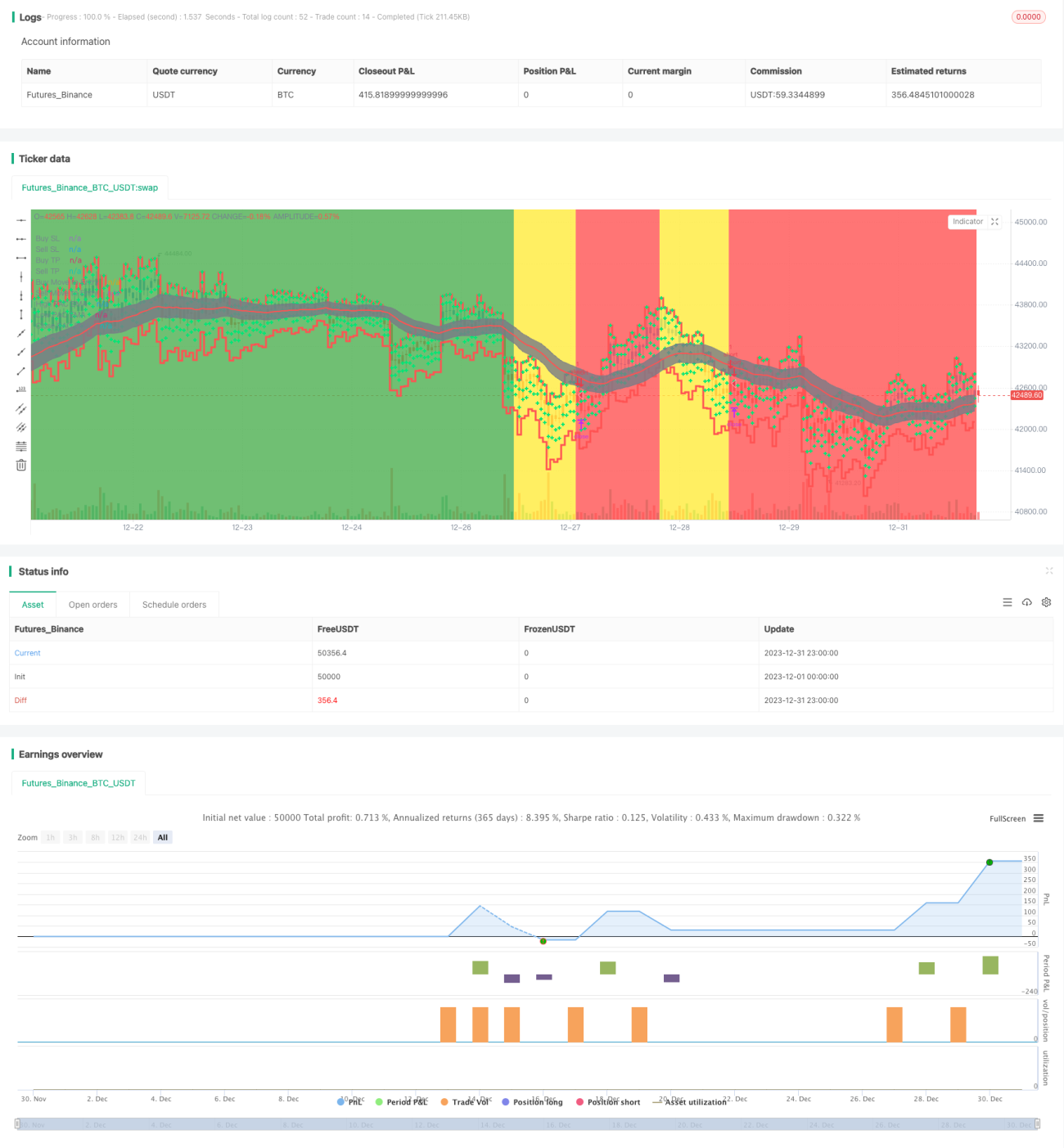

Chiến lược này được xây dựng dựa trên kênh giá từ hai đường trung bình động (MA), sử dụng phạm vi kênh để xác định hướng đi của xu hướng giá và thiết lập trailing stop để chốt lợi nhuận. Đây là chiến lược giao dịch theo xu hướng.

Nguyên lý chiến lược

Chiến lược kênh giá hai đường trung bình động sử dụng EMA nhanh và EMA chậm để xây dựng kênh giá. Tham số EMA nhanh là 89 chu kỳ, EMA chậm là 200 chu kỳ. Đồng thời, sử dụng ba đường trung bình động dựa trên giá cao nhất, giá thấp nhất và giá đóng cửa để xây dựng phạm vi kênh giá. Đường trên và dưới của kênh lần lượt là EMA 34 chu kỳ của giá cao nhất và giá thấp nhất.

Khi EMA nhanh nằm trên EMA chậm và giá thấp hơn đường dưới, xu hướng được xác định là tăng; khi EMA nhanh nằm dưới EMA chậm và giá cao hơn đường trên, xu hướng được xác định là giảm.

Trong xu hướng tăng, chiến lược sẽ bán khống khi xác nhận xu hướng đảo chiều; trong xu hướng giảm, chiến lược sẽ mua khi xác nhận xu hướng đảo chiều.

Ngoài ra, chiến lược còn có chức năng trailing stop. Sau khi vào lệnh, giá trailing stop được cập nhật liên tục để chốt lợi nhuận.

Phân tích ưu điểm

Ưu điểm lớn nhất của chiến lược này là sử dụng hai đường trung bình động để xây dựng kênh giá nhằm xác định xu hướng, kết hợp giao dịch khi đảo chiều, tránh mua đuổi bán đáy. Đồng thời, có chức năng trailing stop giúp chốt lợi nhuận và giảm rủi ro thua lỗ.

Các ưu điểm khác bao gồm: không gian tối ưu tham số lớn, có thể điều chỉnh cho từng sản phẩm và chu kỳ khác nhau; giá stop được cập nhật theo thời gian thực, rủi ro giao dịch thấp.

Phân tích rủi ro

Rủi ro chính của chiến lược là hiệu quả xác định tín hiệu đảo chiều không tốt, có thể dẫn đến nhầm lẫn. Khi đó cần tối ưu tham số để đảm bảo xác định chính xác xu hướng đảo chiều.

Ngoài ra, việc đặt điểm stop cũng rất quan trọng. Nếu stop quá rộng có thể dẫn đến không cắt lỗ kịp thời; nếu stop quá hẹp có thể dẫn đến cắt lỗ quá mức. Cần điều chỉnh dựa trên từng sản phẩm cụ thể.

Cuối cùng, vấn đề dữ liệu cũng có thể khiến chiến lược mất hiệu quả. Cần đảm bảo sử dụng dữ liệu lịch sử đáng tin cậy, liên tục và đầy đủ để backtest và xác thực chiến lược trên thực tế.

Hướng tối ưu hóa

Chiến lược này có thể tối ưu ở một số khía cạnh sau:

-

Chu kỳ của EMA nhanh và EMA chậm có thể tối ưu, thử các tổ hợp tham số khác nhau để đánh giá hiệu quả.

-

Tham số đường trên và dưới của kênh giá cũng có thể điều chỉnh để tìm chu kỳ phù hợp hơn.

-

Việc đặt điểm stop rất quan trọng, có thể thử nghiệm các tham số khác nhau để tối ưu chiến lược stop.

-

Có thể thử thêm các chỉ báo khác để xác định đảo chiều xu hướng, nâng cao hiệu quả giao dịch.

Tổng kết

Chiến lược này có quy trình vận hành tổng thể hợp lý và mượt mà, sử dụng kênh hai đường trung bình động để xác định hướng xu hướng và giao dịch, kết hợp trailing stop để chốt lợi nhuận. Đây là một chiến lược theo xu hướng tương đối ổn định. Thông qua tối ưu tham số và cải thiện cài đặt quản lý rủi ro, chiến lược này có thể trở thành một trong những chiến lược giao dịch định lượng hiệu quả.

- 1