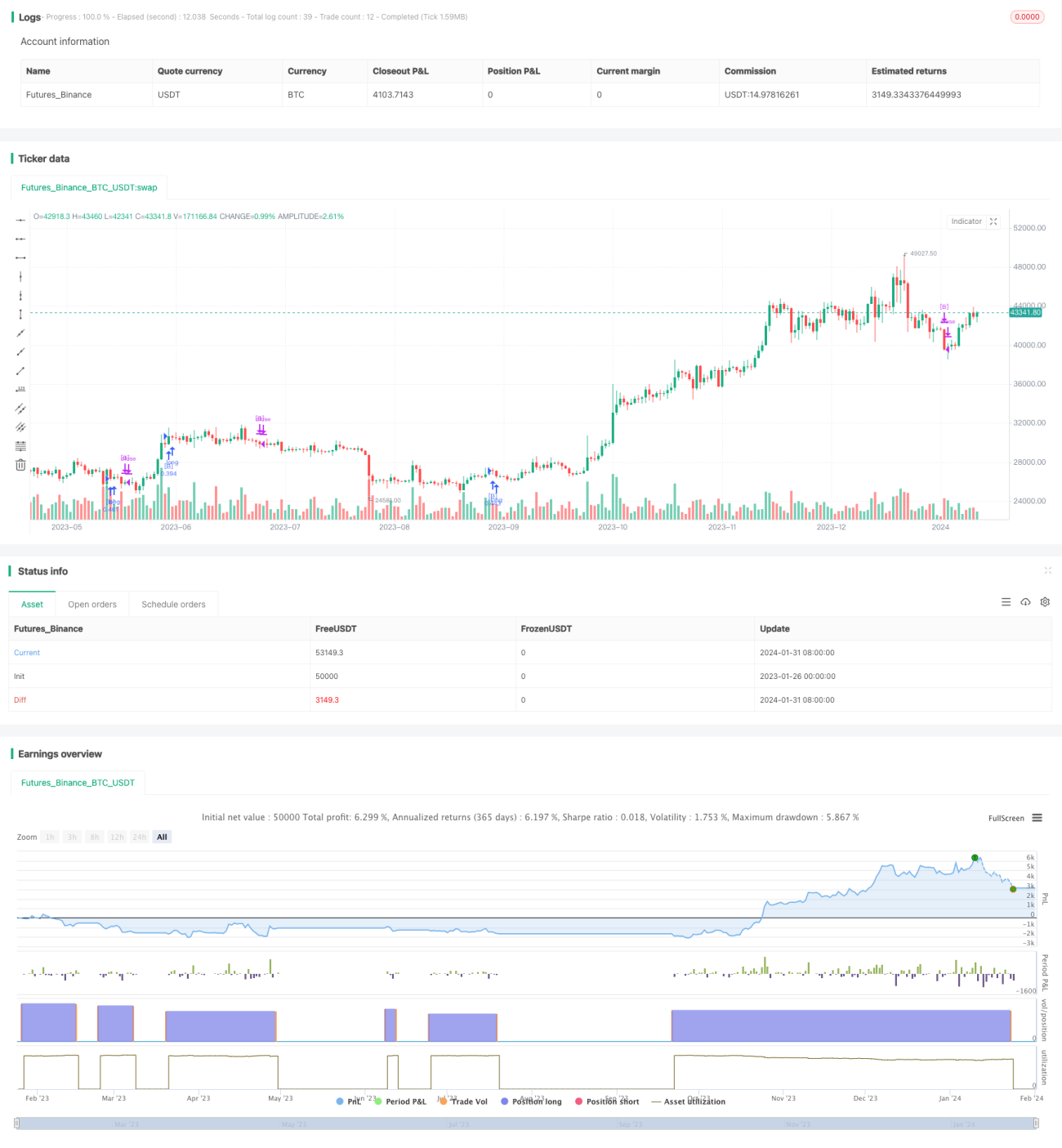

Chiến lược đảo chiều dài hạn dựa trên hai đường trung bình động

Tổng quan

Chiến lược này chủ yếu sử dụng giao cắt vàng và giao cắt chết của đường trung bình động đơn giản 14 và 28 ngày để thực hiện các giao dịch đảo chiều. Khi đường trung bình nhanh vượt lên trên đường trung bình chậm từ dưới lên, điều đó cho thấy xu hướng thị trường bắt đầu đảo chiều, có thể mở vị thế mua; khi đường trung bình nhanh cắt xuống dưới đường trung bình chậm từ trên xuống, điều đó cho thấy xu hướng thị trường bắt đầu đảo chiều, có thể mở vị thế bán.

Do sử dụng đường trung bình động đơn giản để xác định sự thay đổi xu hướng thị trường, tôi đặt tên cho chiến lược này là "Chiến lược đảo chiều dài hạn dựa trên hai đường trung bình động".

Nguyên lý chiến lược

Logic cốt lõi của chiến lược này là sử dụng hai đường trung bình động đơn giản với kỳ hạn khác nhau là 14 ngày và 28 ngày để xác định xu hướng thị trường, các quy tắc cụ thể như sau:

-

Định nghĩa đường nhanh là đường trung bình động đơn giản 14 ngày, đường chậm là đường trung bình động đơn giản 28 ngày.

-

Khi đường nhanh vượt lên trên đường chậm từ dưới lên, đó là tín hiệu mua, vào lệnh mua.

-

Khi đường nhanh cắt xuống dưới đường chậm từ trên xuống, đó là tín hiệu bán, vào lệnh bán.

-

Sau khi mua/bán, nếu đường nhanh lại cắt xuống dưới đường chậm, đó là tín hiệu đóng vị thế.

Chiến lược này đồng thời kết hợp quản lý rủi ro với cắt lỗ, chốt lời và chốt lời theo dõi. Đối với các trường hợp mua và bán, lần lượt xác định giá cắt lỗ cho vị thế mua, giá chốt lời cho vị thế mua, giá chốt lời cho vị thế bán, giá chốt lời theo dõi cho vị thế mua. Các tham số này đều được thiết lập dưới dạng phần trăm, giúp chiến lược linh hoạt hơn.

Phân tích ưu điểm

- Chiến lược sử dụng hai đường trung bình động để xác định xu hướng chính của thị trường, nguyên lý đơn giản rõ ràng, dễ hiểu và dễ kiểm chứng.

- Chu kỳ của đường trung bình nhanh và chậm được đặt ở 14 và 28 ngày, đại diện cho sự chuyển đổi xu hướng ngắn hạn và trung hạn, có thể phát hiện tốt các cơ hội đảo chiều.

- Kết hợp chốt lời, cắt lỗ và chốt lời theo dõi để kiểm soát rủi ro, giúp khóa lợi nhuận và tránh thua lỗ mở rộng.

- Có thể đồng thời mua và bán, đáp ứng nhu cầu của các môi trường thị trường khác nhau.

Rủi ro và cải tiến

- Giao cắt hai đường trung bình động có độ trễ nhất định, có thể bỏ lỡ thời điểm vào lệnh tối ưu.

- Giao cắt giữa đường trung bình dài và ngắn dễ xảy ra tín hiệu sai, nên tránh đặt chu kỳ đường trung bình quá ngắn.

- Khoảng cách cắt lỗ đặt quá nhỏ có thể làm tăng xác suất bị chạm lỗ. Nên thiết lập khoảng cách cắt lỗ hợp lý dựa trên từng loại sản phẩm.

- Có thể đưa thêm nhiều chỉ báo hơn để kết hợp, nâng cao độ vững chắc của chiến lược. Ví dụ thêm Bollinger Bands để xác định xu hướng, hoặc đưa MACD vào để kiểm tra thời điểm vào lệnh.

Hướng tối ưu

- Kiểm tra các tổ hợp tham số đường trung bình khác nhau, tìm chu kỳ đường trung bình phù hợp hơn với đặc tính của sản phẩm.

- Kiểm tra các thiết lập khoảng cách cắt lỗ khác nhau, tìm vị trí cắt lỗ tối ưu.

- Kiểm tra việc thêm các chỉ báo khác để tối ưu, tìm tổ hợp tham số tối ưu nhằm giảm tín hiệu sai.

- Tối ưu quy tắc quản lý vị thế, giúp lợi nhuận trở nên dồi dào hơn.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược rất kinh điển dựa trên hai đường trung bình động để xác định sự đảo chiều xu hướng. Nó có ưu điểm là nguyên lý thao tác đơn giản, dễ nắm bắt; đồng thời cũng có một số hướng có thể tiếp tục tối ưu sau này. Nhìn chung, chiến lược này khá hoàn thiện về nguyên lý và thao tác, là một chiến lược khởi đầu tốt cho giao dịch định lượng.

- 1