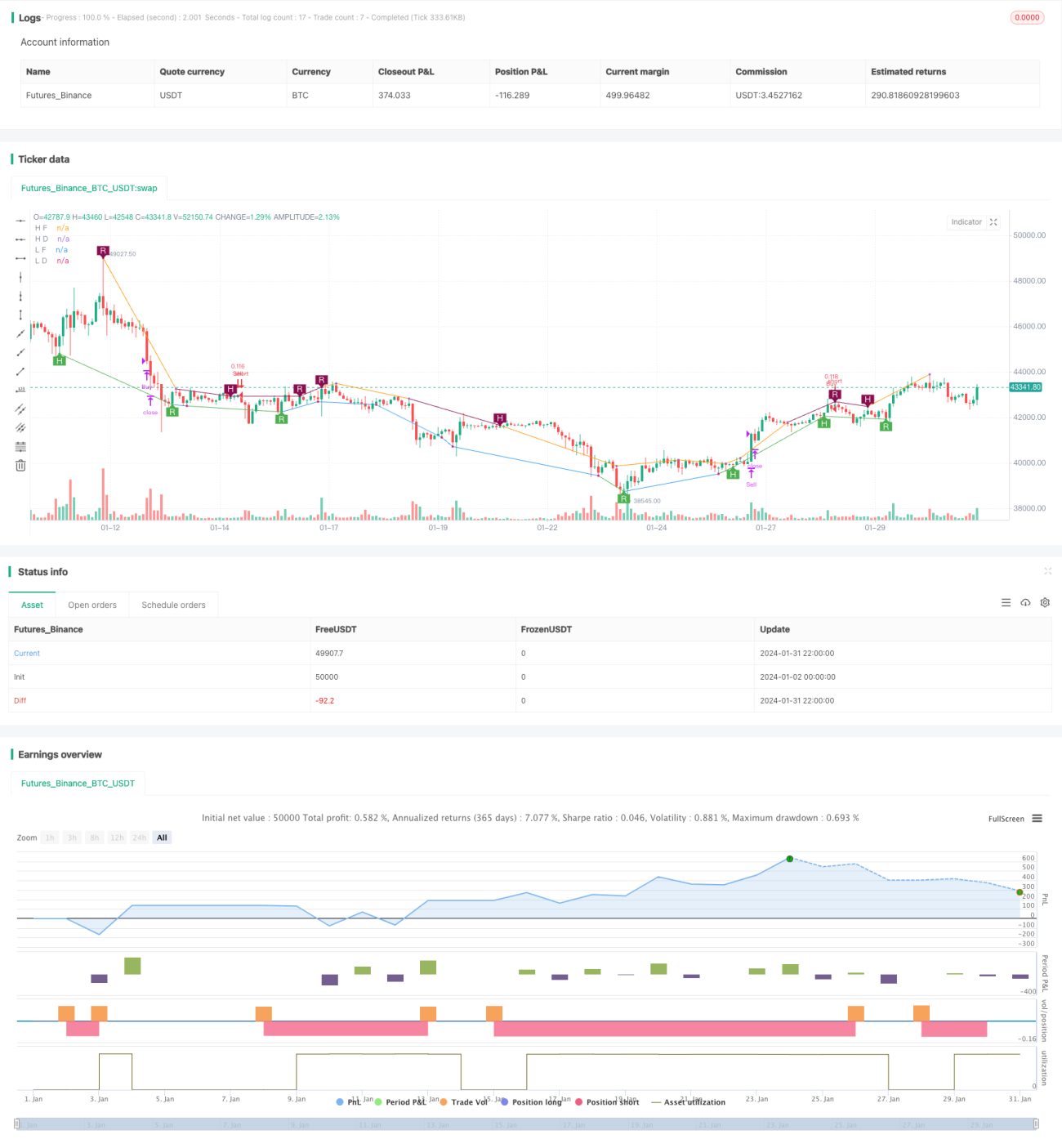

Chiến lược giao dịch theo xu hướng dựa trên sự phân kỳ giá

Tổng quan

Chiến lược này là một chiến lược giao dịch theo xu hướng dựa trên tín hiệu phân kỳ giá. Nó sử dụng nhiều chỉ báo để phát hiện tín hiệu phân kỳ giá, chẳng hạn như RSI, MACD, Stochastics, v.v., và được xác nhận bởi bộ dao động Murrey Math. Khi tín hiệu phân kỳ giá xuất hiện, nếu bộ dao động cũng xác nhận hướng xu hướng hiện tại, thì sẽ thực hiện vào lệnh.

Nguyên lý chiến lược

Cốt lõi của chiến lược là lý thuyết phân kỳ giá. Khi giá tạo đỉnh cao hơn nhưng chỉ báo không tạo đỉnh cao hơn, được gọi là phân kỳ giá giảm (bearish divergence); khi giá tạo đáy thấp hơn nhưng chỉ báo không tạo đáy thấp hơn, được gọi là phân kỳ giá tăng (bullish divergence). Điều này cho thấy xu hướng có thể đảo chiều. Chiến lược kết hợp phân kỳ đỉnh/đáy với bộ dao động để xác nhận tín hiệu giao dịch.

Cụ thể, điều kiện vào lệnh của chiến lược là:

- Phát hiện tín hiệu phân kỳ giá, bao gồm phân kỳ thông thường và phân kỳ ẩn.

- Bộ dao động Murrey Math nằm trong vùng xu hướng tương ứng.

Điều kiện thoát lệnh là khi bộ dao động quay lại cắt đường trung bình.

Phân tích ưu điểm

Chiến lược này kết hợp lý thuyết phân kỳ giá và xác nhận xu hướng, có những ưu điểm sau:

- Sử dụng tín hiệu phân kỳ giá để phát hiện các điểm đảo chiều xu hướng tiềm năng.

- Áp dụng bộ dao động để xác nhận xu hướng hiện tại, tránh phá vỡ giả.

- Kết hợp nhiều chỉ báo và tham số, có thể điều chỉnh linh hoạt.

- Cân bằng giữa theo dõi xu hướng và phòng ngừa thua lỗ.

- Logic quy tắc rõ ràng, dư địa tối ưu hóa mã lớn.

Phân tích rủi ro

Rủi ro chính đến từ các khía cạnh sau:

- Tín hiệu phân kỳ giá có thể là tín hiệu giả, không thể hoàn toàn xác nhận sự đảo chiều xu hướng.

- Cài đặt tham số bộ dao động không phù hợp có thể dẫn đến bỏ lỡ cơ hội giao dịch.

- Sự nghiêng lệch quá mức về vị thế mua hoặc bán có thể gây rủi ro thua lỗ lớn.

- Trong giai đoạn biến động mạnh, có thể làm tăng số lượng giao dịch và chi phí trượt giá.

Khuyến nghị đặt stop loss, điều chỉnh vị thế và tối ưu hóa tổ hợp tham số để giảm rủi ro.

Hướng tối ưu hóa

Chiến lược này còn có dư địa tối ưu hóa thêm:

- Thêm thuật toán học máy để tối ưu hóa tổ hợp tham số theo thời gian thực.

- Thêm kỹ thuật stop loss thích ứng, chẳng hạn như trailing stop, average stop, v.v.

- Kết hợp thêm nhiều chỉ báo và bộ lọc để cải thiện tỷ lệ tín hiệu/nhiễu.

- Điều chỉnh linh hoạt tham số bộ dao động để tối ưu hóa nhận định xu hướng.

- Tối ưu hóa quản lý rủi ro, đặt các giới hạn như drawdown tối đa.

Tổng kết

Chiến lược này tích hợp lý thuyết phân kỳ giá và các chỉ báo phân tích xu hướng, có thể phát hiện hiệu quả các điểm chuyển đổi xu hướng tiềm năng. Kết hợp các biện pháp quản lý rủi ro được tối ưu hóa, có thể đạt được tỷ suất lợi nhuận chiến lược tốt. Trong tương lai, có thể tối ưu hóa thông qua các phương pháp tiên tiến như học máy để đạt được lợi nhuận vượt trội ổn định hơn.

- 1