Mean-Reversion-Momentum-Strategie

Überblick

Die Mean-Reversion-Momentum-Strategie ist eine Trendhandelsstrategie, die kurzfristige Preis-Durchschnitte verfolgt. Sie kombiniert Mean-Reversion-Indikatoren mit Momentum-Indikatoren, um die mittelfristige Markttendenz zu bestimmen.

Strategieprinzip

Die Strategie berechnet zunächst die Mean-Reversion-Linie des Preises sowie die Standardabweichung. Anschließend wird anhand der vorgegebenen Schwellenwerte (Upper Threshold und Lower Threshold) überprüft, ob der Preis um mehr als eine Standardabweichung von der Mean-Reversion-Linie abweicht. Bei Überschreitung wird ein Handelssignal generiert.

Für ein Long-Signal muss der Preis mindestens eine Standardabweichung unter der Mean-Reversion-Linie liegen, der Schlusskurs unter dem SMA der LENGTH-Periode und über dem TREND-SMA liegen. Bei Erfüllung dieser drei Bedingungen wird eine Long-Position eröffnet. Die Schließung erfolgt, sobald der Preis den SMA der LENGTH-Periode von unten nach oben durchbricht.

Für ein Short-Signal muss der Preis mindestens eine Standardabweichung über der Mean-Reversion-Linie liegen, der Schlusskurs über dem SMA der LENGTH-Periode und unter dem TREND-SMA liegen. Bei Erfüllung dieser drei Bedingungen wird eine Short-Position eröffnet. Die Schließung erfolgt, sobald der Preis den SMA der LENGTH-Periode von oben nach unten durchbricht.

Die Strategie verwendet zudem einen prozentualen Gewinn- und Verlustziel (Percent Profit Target und Percent Stop Loss) zur Realisierung von Gewinnmitnahmen und Verlustbegrenzung.

Als Exit-Methode kann entweder der Durchbruch eines gleitenden Durchschnitts oder die lineare Regressionsdurchbrechung gewählt werden.

Durch die Kombination von Long- und Short-Trades, Trendfilterung sowie Gewinnmitnahme- und Stop-Loss-Management wird der mittelfristige Markttrend erkannt und verfolgt.

Strategievorteile

-

Der Mean-Reversion-Indikator kann effektiv beurteilen, ob der Preis vom inneren Wert abweicht.

-

Der Momentum-Indikator SMA filtert kurzfristiges Marktrauschen heraus.

-

Long- und Short-Trades ermöglichen eine umfassende Erfassung von Trendchancen.

-

Gewinnmitnahme- und Stop-Loss-Mechanismen kontrollieren das Risiko effektiv.

-

Wahlbare Exit-Methoden ermöglichen eine flexible Anpassung an die Marktbedingungen.

-

Die vollständige Trendhandelsstrategie erfasst mittelfristige Trends gut.

Strategierisiken

-

Der Mean-Reversion-Indikator ist empfindlich gegenüber Parametereinstellungen; falsch gewählte Schwellenwerte können zu Fehlsignalen führen.

-

Bei stark schwankenden Märkten können zu häufige Stop-Loss-Auslösungen auftreten.

-

In Seitwärtsmärkten kann die Handelsfrequenz zu hoch sein, was zu höheren Transaktionskosten und Slippage-Risiken führt.

-

Bei illiquiden Handelsinstrumenten kann die Slippage-Kontrolle unbefriedigend sein.

-

Das Long-Short-Handelsmodell birgt ein höheres Risiko und erfordert eine sorgfältige Kapitalverwaltung.

Diese Risiken können durch Parameteroptimierung, Anpassung der Stop-Loss-Methoden und Kapitalmanagement kontrolliert werden.

Optimierungsmöglichkeiten

-

Optimierung der Parameter für Mean-Reversion und Momentum-Indikatoren, um sie besser an verschiedene Instrumente anzupassen.

-

Hinzufügen von Trendbestimmungsindikatoren zur Verbesserung der Trendidentifikation.

-

Optimierung der Stop-Loss-Strategie, um sie besser an starke Marktschwankungen anzupassen.

-

Einführung eines Positionsgrößenmanagement-Moduls zur Anpassung der Positionsgröße an die Marktbedingungen.

-

Hinzufügen weiterer Risikomanagementmodule, z. B. Kontrolle des maximalen Drawdowns oder der Eigenkapitalkurve.

-

Integration von maschinellen Lernmethoden zur automatischen Parameteroptimierung der Strategie.

Zusammenfassung

Zusammenfassend lässt sich sagen, dass die Mean-Reversion-Momentum-Strategie durch einfache und effektive Indikatoren die Wertrückkehrtendenzen auf mittlere Sicht erfasst. Die Strategie weist eine hohe Anpassungsfähigkeit und Universalität auf, birgt jedoch auch gewisse Risiken. Durch kontinuierliche Optimierung und Kombination mit anderen Strategien können bessere Ergebnisse erzielt werden. Insgesamt ist die Strategie recht vollständig und stellt einen erwägenswerten Trendhandelsansatz dar.

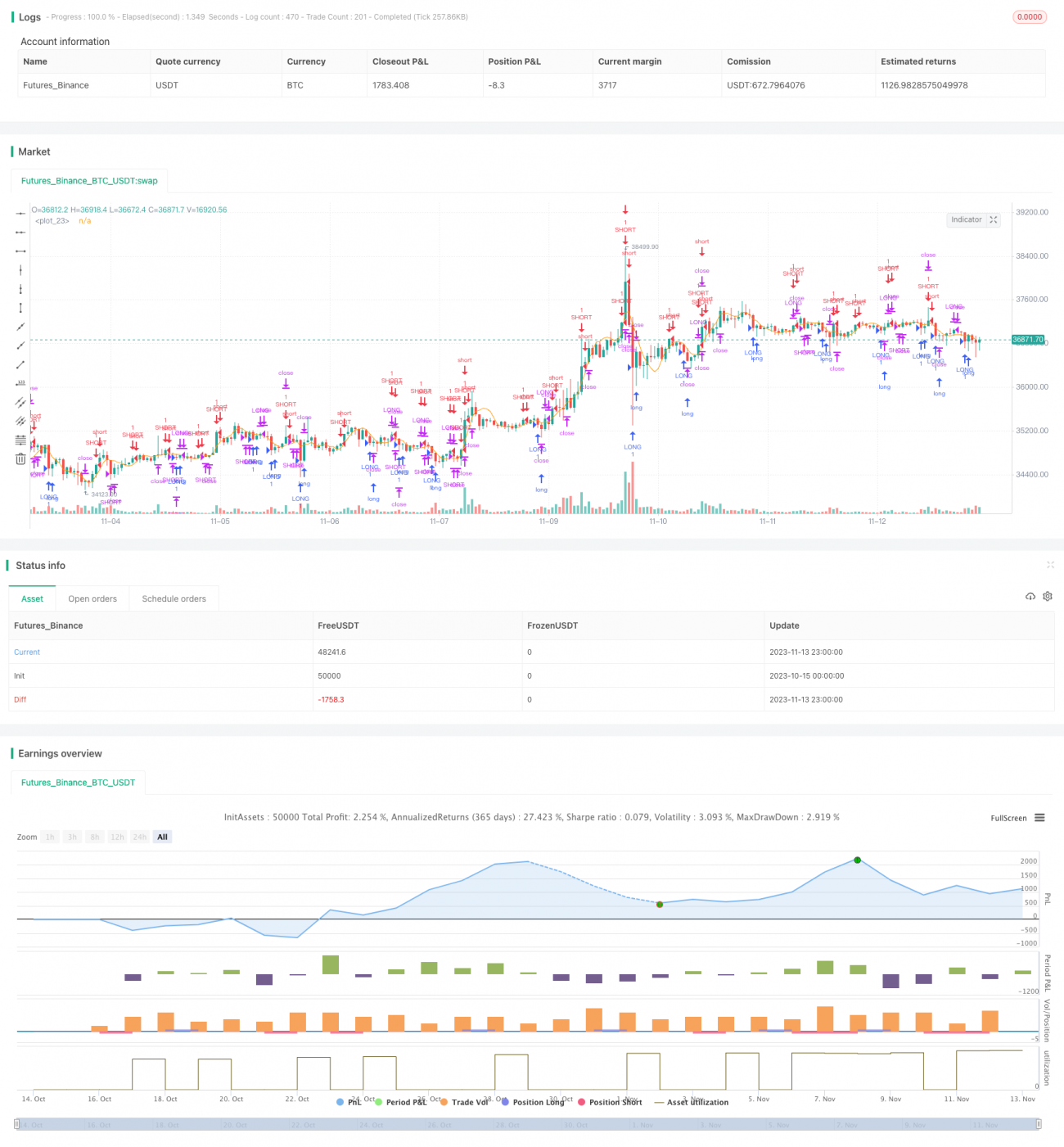

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1