Auf Multi-Indikatoren basierende quantitative Handelsstrategie

Übersicht

Diese Strategie realisiert automatische Long-/Short-Positioneröffnungen und -Schließungen durch die Integration von drei Hauptindikatoren: gleitende Durchschnitte, Relative-Stärke-Index (RSI) und Moving Average Convergence Divergence (MACD). Der Name der Strategie enthält „Multiple Indikatoren“, um die Vielzahl der verwendeten Indikatoren hervorzuheben.

Strategieprinzip

Die Strategie bestimmt vor allem die Trendrichtung durch den Vergleich der Größenverhältnisse zweier gleitender Durchschnitte und kombiniert den RSI-Indikator, um Reversal-Chancen nicht zu verpassen. Konkret verwendet die Strategie EMA oder SMA zur Berechnung einer schnellen und einer langsamen Linie. Ein Kreuzen der schnellen Linie über die langsame Linie ist ein Kaufsignal, ein Kreuzen der schnellen Linie unter die langsame Linie ein Verkaufssignal. Um Fehlausbrüche zu filtern, wird zusätzlich eine Long-/Short-Logik für den RSI-Indikator implementiert: Nur wenn der RSI ebenfalls die Bedingung erfüllt, wird ein Handelssignal generiert.

Darüber hinaus wird der MACD-Indikator für Handelsentscheidungen integriert. Wenn die Differenzlinie des MACD die Nulllinie von unten nach oben kreuzt, ist dies ein Kaufsignal; kreuzt sie von oben nach unten, ein Verkaufssignal. So kann mithilfe des MACDs beurteilt werden, ob der Trend eine Wende vollzieht, um fehlerhafte Signale an Trendwendepunkten zu vermeiden.

Vorteile

Der größte Vorteil dieser Strategie liegt in der Integration mehrerer Indikatoren zur Signalfilterung, wodurch Fehlsignale effektiv reduziert und die Signalqualität verbessert werden kann. Im Einzelnen:

-

Die Kombination aus schneller/langsamer Linie und RSI vermeidet Fehlausbrüche, die bei alleiniger Verwendung gleitender Durchschnitte auftreten können.

-

Die Integration des MACD ermöglicht eine frühzeitige Erkennung von Trendumkehrungen und vermeidet Fehlsignale an Wendepunkten.

-

Die Wahl zwischen EMA und SMA erlaubt eine an die unterschiedlichen Markteigenschaften angepasste Indikatorparametrierung.

-

Die Option zur Auswahl eines Money-Management-Plans ermöglicht die Kontrolle des Einzelordervolumens und eine effektive Risikosteuerung.

-

Unterstützung von Stop-Loss und Take-Profit sichert Gewinne und verhindert eine Ausweitung von Verlusten.

Risikoanalyse

Die Strategie ist hauptsächlich folgenden Risiken ausgesetzt:

-

Eine ungeeignete Parameteroptimierung kann zu schlechter Strategieleistung führen. Es ist notwendig, verschiedene Parameterkombinationen zu testen.

-

Die Wahrscheinlichkeit von Fehlsignalen der Indikatoren besteht weiterhin. Wenn alle drei Indikatoren gleichzeitig ein Fehlsignal geben, kann dies zu größeren Verlusten führen.

-

Die Performance ist bei einem einzelnen Instrument nicht stabil und muss auf weitere Instrumente ausgeweitet werden.

-

Datenicht zureichen, Strategie effekt wird in der Zukunft abnehmen.

Optimierungsmöglichkeiten

Die Strategie kann hauptsächlich in folgenden Bereichen optimiert werden:

-

Test verschiedener Indikatorparameterkombinationen zur Ermittlung optimaler Parameter.

-

Hinzufügen eines nachlaufenden Stops (Trailing Stop) innerhalb der Stop-Loss-Mechanismen. Sobald der Kurs eine bestimmte Strecke zurückgelegt hat, kann ein Trailing Stop Gewinne sichern.

-

Hinzufügen von Indikatoren zur Beurteilung des übergeordneten Trends, um countertrend Trades zu vermeiden, z. B. Integration des ADX-Indikators.

-

Fügen Sie Moneymanagement Module hinzu für besseres Risikomanagement.

-

Fügen Sie Filter für fundamentale Faktoren wie Nachrichten hinzu.

Zusammenfassung

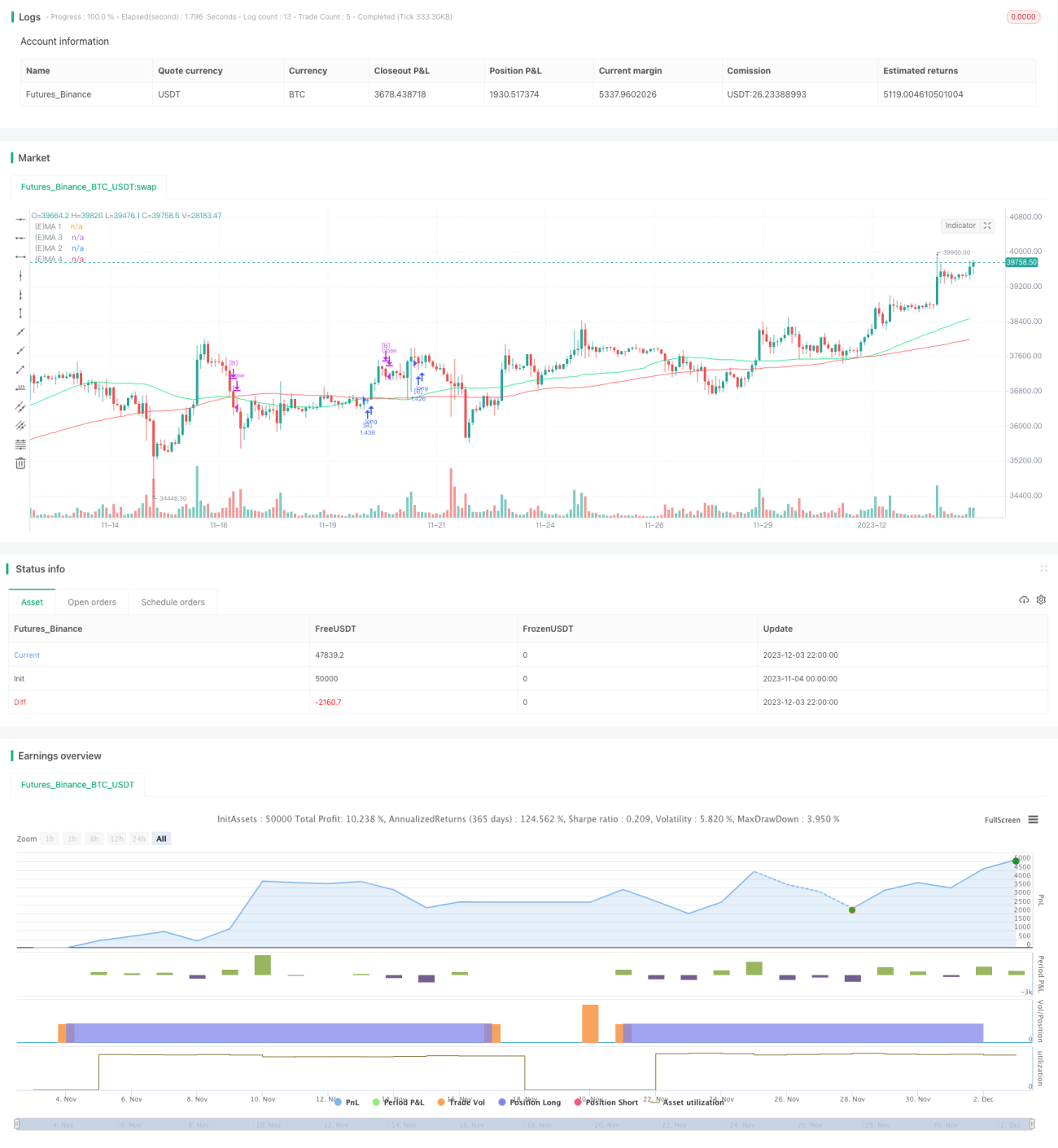

Diese Strategie realisiert die Identifikation und Filterung von Long- und Short-Signalen durch die Integration mehrerer technischer Indikatoren wie gleitende Durchschnitte, RSI und MACD. Ihr Vorteil liegt in der effektiven Filterung von Fehlsignalen und der Verbesserung der Signalqualität. Hauptnachteile sind die Parameterwahl und die weiterhin bestehende Wahrscheinlichkeit von Fehlsignalen der Indikatoren. Zukünftige Optimierungsrichtungen umfassen Parameteroptimierung, Stop-Loss-Optimierung, Trendfilterung usw. Insgesamt ist die Strategie als Multi-Indikator-Rahmenwerk wirksam und bedarf weiterer Optimierung und Validierung.

/*backtest

start: 2023-11-04 00:00:00

end: 2023-12-04 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fikira

//@version=4

strategy("Strategy Tester EMA-SMA-RSI-MACD", shorttitle="Strat-test", overlay=true, max_bars_back=5000, - 1